Idaho Rental Property Coverage: Landlord Protection You Can Rely On

Owning rental property in Idaho comes with real financial exposure. Tenant damage, liability claims, and income loss can happen faster than you’d expect.

We at Matt Anderson Insurance know that Idaho rental property coverage isn’t optional-it’s the foundation of smart property ownership. This guide walks you through what protection you actually need and how to get it right.

What Your Idaho Landlord Policy Actually Protects

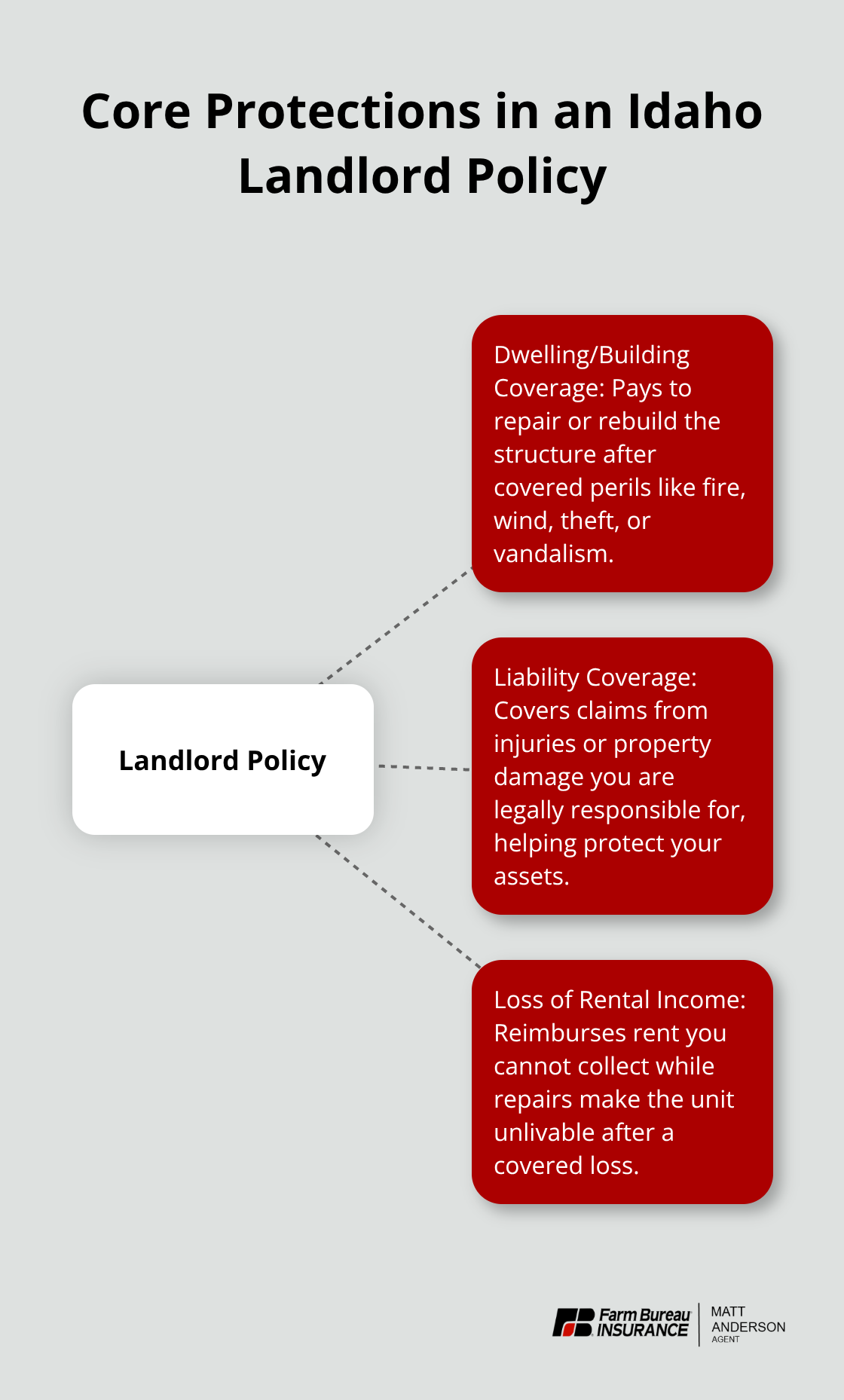

A standard landlord policy in Idaho covers the building itself, your liability exposure, and lost rental income when a covered event makes the property unlivable. The dwelling coverage pays to repair or replace the structure after fire, wind, theft, or vandalism. What matters most is that your dwelling limit reflects your actual rebuild cost. If construction costs have climbed in your area and your limit hasn’t kept pace, you’ll face a gap when you file a claim.

Coverage for Structures and Equipment on Your Property

Other structures coverage on your policy protects detached garages, sheds, or storage buildings. Landlord’s personal property coverage includes maintenance equipment like lawnmowers and tools you keep on-site to service the rental, but it explicitly does not cover tenants’ belongings-that’s their responsibility through renters insurance. This distinction matters because many landlords mistakenly assume their policy protects tenant property, only to discover otherwise after a loss.

Why Loss of Rent Coverage Matters More Than You Think

Loss of rental income protection reimburses you for rent you cannot collect while the property is being repaired after a covered peril. If a kitchen fire makes the unit uninhabitable for three months, this coverage pays your lost rent during that repair period. Most agents recommend setting your loss of rent limit to cover six to twelve months of expected income, depending on how quickly repairs typically happen in your area. This protection stabilizes your cash flow when a covered event disrupts your rental income stream.

Liability and Medical Payments Protection

Liability coverage on a landlord policy runs higher than homeowners insurance precisely because tenant activity and guest injuries create different exposure. A guest slipping on ice in your stairwell or a tenant’s injury from a maintenance failure can trigger a significant claim. Your policy also covers medical payments for minor injuries on the property, protecting you from small claims that might otherwise require legal defense.

What Your Policy Does Not Cover

Standard landlord policies do not cover intentional damage by tenants or damage from flood-flood requires a separate National Flood Insurance Program policy or private flood carrier. Wrongful eviction claims and wrongful entry liability are increasingly important endorsements in Idaho, especially as tenant rights laws evolve, and many landlords add personal umbrella liability insurance for additional protection to cover assets beyond the standard policy limits. Understanding these gaps helps you identify which additional protections your rental operation actually needs.

What Actually Threatens Your Idaho Rental Property

Tenant damage ranks as the costliest exposure most Idaho landlords face, and it extends far beyond what standard landlord insurance covers. Intentional damage-a tenant punches a wall, deliberately floods a unit, or destroys appliances-falls outside your policy entirely, leaving you to pursue legal action and collect from the tenant directly, a process that often yields nothing. Even unintentional damage from negligence can create disputes about whether the tenant or your policy bears responsibility. Security deposits rarely cover the full cost of repairs, and eviction proceedings in Idaho consume time and legal fees that eat into your rental income long before a new tenant moves in.

Tenant Screening Stops Problems Before They Start

The National Association of Residential Property Managers reports that the average eviction costs landlords between $3,500 and $5,000 when accounting for lost rent, legal fees, and property damage. This reality makes tenant screening your first line of defense. Run background checks on every applicant, verify income at two to three times the monthly rent, check at least two prior landlord references, and conduct in-person property tours-this process filters out problem tenants before they sign a lease. Documented maintenance records also matter; if a tenant claims you failed to maintain the property, your records prove otherwise and protect you in liability disputes.

Weather and Natural Disasters Hit Hard in Idaho

Weather and natural disasters hit Idaho rental properties with unpredictable force, and your standard landlord policy has clear limits. Hail damage to roofs, wind damage during spring storms, and winter freeze-thaw cycles that burst pipes occur regularly across Idaho, but flood damage remains completely excluded from standard coverage-you must purchase separate National Flood Insurance Program protection or a private flood policy if your property sits in or near a flood zone.

Liability Claims From Injuries on Your Property

Liability claims from injuries on your property represent a major risk, and they often surprise landlords with their severity. A tenant’s guest slips on ice in winter, a child suffers injury from a loose deck railing, or someone gets hurt by a maintenance hazard you failed to address-any of these can trigger significant claims, which is why your liability limit should reflect realistic exposure for your property type and location. Idaho’s premises liability laws hold property owners responsible for maintaining safe conditions to prevent injuries, so you must maintain clear walkways, functional lighting in common areas, working handrails, and documented safety inspections.

Safety Upgrades Lower Your Risk and Your Premiums

Installing monitored alarms, smoke and carbon monoxide detectors, water leak sensors, and automatic shut-off devices not only reduces your risk but also qualifies you for premium discounts with most Idaho insurers-some carriers credit 5 to 15 percent off your premium for documented safety upgrades. Winter preparedness deserves particular attention; establish a snow removal protocol, salt icy walkways promptly, document your safety measures with photos, and communicate expectations clearly to tenants about their responsibilities for maintaining entry areas. These proactive steps protect your tenants, reduce your exposure, and position your property as a lower-risk investment when you work with your insurance agent to review coverage options tailored to your specific rental operation.

How to Choose the Right Landlord Insurance Policy

Calculate Your Property’s True Rebuild Cost

Start by calculating your property’s true rebuild cost, not its market value. Market value includes land, which insurance does not replace after a loss, while rebuild cost reflects what it actually costs to reconstruct the building from the ground up. Idaho construction costs vary significantly by region and property type. Most communities see building costs ranging from $200 to $400 per square foot, depending on local labor rates, material costs, and your home’s quality grade. Contact local contractors for quotes on a full rebuild, then add 10 to 15 percent as a buffer for cost inflation between now and when you file a claim.

Your dwelling limit must match this figure closely. Underinsuring by just 20 percent can trigger coinsurance penalties that reduce your claim payout substantially, leaving you to cover the gap yourself. The Insurance Information Institute reports that the average U.S. landlord pays around $1,083 annually for landlord insurance, though Idaho premiums typically range from $950 to $1,400 depending on property specifics. Your rebuild cost drives the largest portion of that premium, so get the number right before you compare quotes.

Set Loss of Rent Limits Based on Realistic Repair Timelines

Loss of rent limits deserve the same precision as your dwelling coverage. Calculate your monthly rental income, then multiply by the number of months repairs typically take in your area. Idaho winter storms can disable a property for two to three months, while major structural damage might require six months or longer. Try to set your loss of rent limit to cover this realistic timeframe rather than guessing at a number that may leave you short when you need it most.

Choose a Deductible You Can Actually Afford

Deductibles create a direct trade-off with your premium. A $1,000 deductible costs less than a $500 deductible, but you absorb that $1,000 out of pocket after every claim. Consider your cash reserves when selecting this number. If a tenant-caused fire damages the rental, you pay the deductible before insurance kicks in, so select a deductible you can actually afford without creating financial stress.

Address Short-Term Rental Coverage Gaps

Short-term rentals demand additional scrutiny because standard landlord policies often restrict coverage for properties rented fewer than 30 or 90 days per year. Vacation rental platforms like Airbnb require specialized coverage that differs substantially from traditional long-term rental policies. Your liability exposure increases significantly with short-term rentals because you host frequent guests with no lease agreement or tenant screening process.

Ask a local agent explicitly whether your policy covers short-term rental activity, and if not, what endorsements or alternative policies address this gap. Many carriers exclude short-term rentals entirely from standard coverage, forcing you to shop for specialized short-term rental policies that carry higher premiums but provide the protection your operation actually needs.

Final Thoughts

Protecting your Idaho rental property requires more than hoping nothing goes wrong. You need landlord coverage that matches your actual rebuild costs, covers your lost income during repairs, and provides liability protection against the real risks tenants and guests create on your property. The gaps in standard coverage-intentional tenant damage, flood losses, and wrongful eviction claims-demand your attention before you face a loss and discover what your policy won’t pay.

Your property’s value and your financial stability depend on getting Idaho rental property coverage right from the start. Underinsuring by even 20 percent triggers coinsurance penalties that slash your claim payout, while skipping loss of rent coverage leaves you absorbing months of lost income out of pocket. Short-term rental activity requires specialized endorsements that standard policies often exclude entirely, and these details separate landlords who recover quickly from losses and those who face financial hardship.

Contact Matt Anderson Insurance for a quote tailored to your Idaho rental property. Bring your property details, current rent amount, and any recent improvements you’ve made so our agents can walk you through coverage options and help you build protection that lets you operate your rental with confidence.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.