Idaho Car Insurance Quotes: How To Get Fast, Accurate Estimates

Getting Idaho car insurance quotes shouldn’t feel like a guessing game. The difference between a quote that matches your actual costs and one that leaves you surprised at renewal can come down to the information you provide and the insurers you compare.

We at Matt Anderson Insurance help Idaho drivers cut through the confusion and find quotes that reflect their real needs. This guide walks you through exactly what insurers look for, common mistakes that drive up costs, and how to get accurate estimates fast.

How Insurers Calculate Your Idaho Car Insurance Quote

The Information That Shapes Your Quote

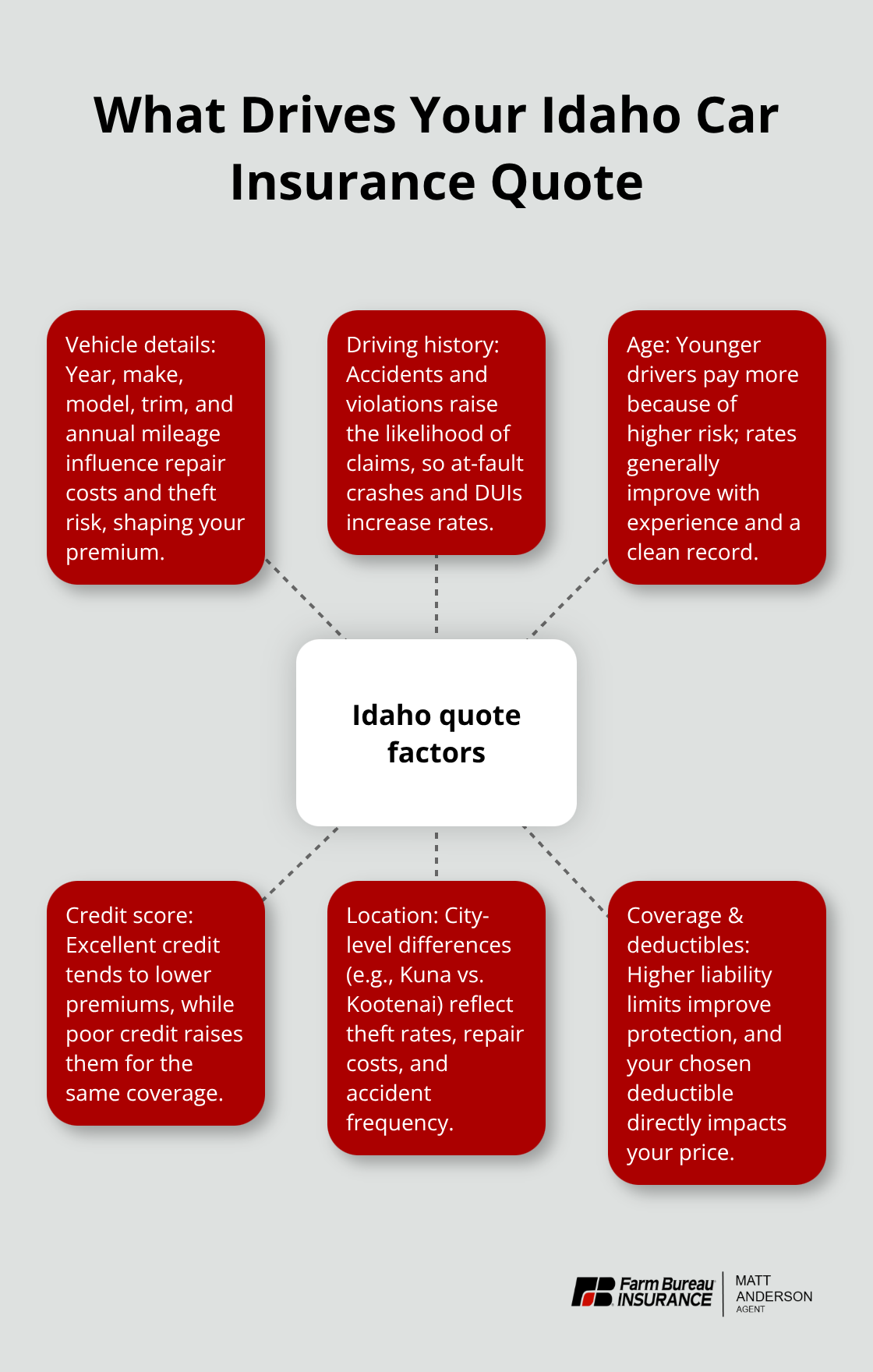

Insurers don’t pull numbers from thin air when they generate a quote. They assemble a detailed financial profile of your risk, and the accuracy of your quote depends entirely on the accuracy of the information you provide. When you request an Idaho car insurance quote, insurers ask for your vehicle details-year, make, model, trim, and annual mileage-because these directly affect repair costs and theft risk. A 2024 Honda Accord LX costs about $1,887 per year for full coverage in Idaho, while a Honda CR-V averages about $1,560 per year, according to Insure.com data from 2026. That $327 difference reflects actual repair expenses and market values.

You’ll also provide your driving history, including any accidents or violations, because insurance companies use this to assess how likely you are to file a claim. A single at-fault accident raises your full-coverage premium to around $2,023 per year, while a DUI pushes costs to approximately $2,423 per year. Your age matters significantly too. An 18-year-old pays about $4,580 per year for full coverage, a 20-year-old around $3,278 per year, and a 25-year-old approximately $1,951 per year.

How Credit Score and Location Affect Your Costs

Credit score is another major factor-drivers with excellent credit pay roughly $1,318 per year for full coverage, while those with poor credit face about $2,194 per year. Location within Idaho affects your quote as well. Kuna residents pay among the lowest rates at about $1,636 per year, while Kootenai drivers pay around $2,105 per year for the same coverage. The difference comes from local theft rates, repair shop costs, and accident frequency in each area.

Deductibles and Coverage Limits Control Your Premium

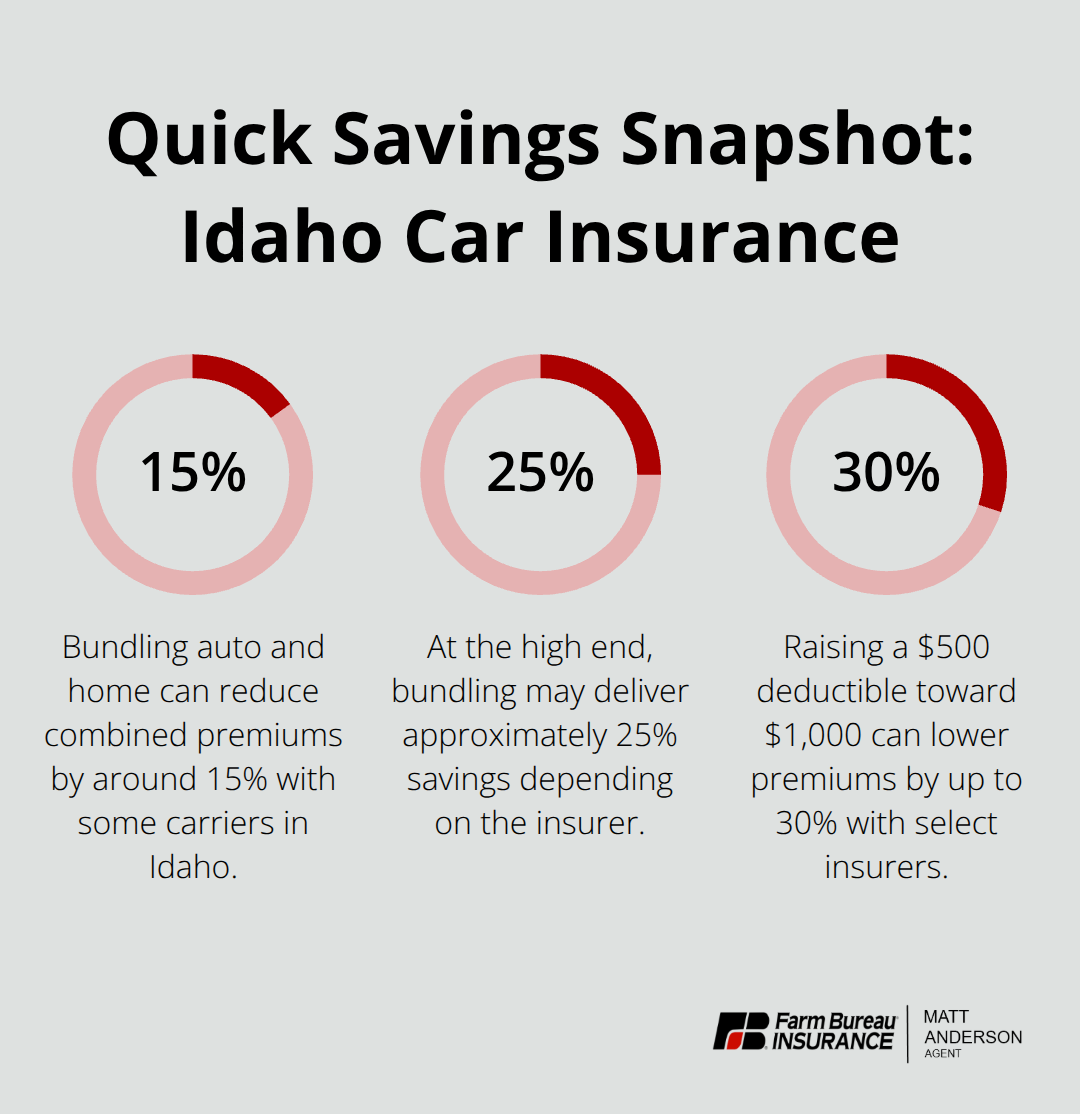

Your deductible is the amount you pay out-of-pocket when you file a claim, and it’s one of the few factors you control directly. Raising your deductible from $500 to $1,000 lowers your monthly premium, but only select a deductible you can actually afford to pay if an accident happens. Idaho’s average full-coverage cost is about $1,901 per year, or roughly $158 per month, but this assumes a standard $500 deductible. Increase that deductible, and your premium drops-sometimes by 20 to 30 percent depending on the insurer.

The coverage limits you select also determine your quote’s accuracy. Idaho requires minimums of 25/50/15, meaning $25,000 bodily injury per person, $50,000 per accident, and $15,000 property damage. These minimums are genuinely insufficient for serious crashes. Carrying 100/300/100 limits instead of the state minimum typically adds only $50 to $100 per year to your premium but provides substantially better protection.

Uninsured Motorist Coverage and Your Quote

Uninsured and underinsured motorist coverage also affects your quote. Idaho requires you to be offered these protections, and they typically cost between $10 and $30 per month depending on your limits. If another driver causes an accident and lacks sufficient insurance, this coverage protects you and your passengers-and it’s worth the modest premium increase. When you request quotes, the insurer plugs in your chosen limits, and the quote reflects that exact coverage. The next section shows you how to compare these quotes across multiple insurers and identify which one actually fits your budget and protection needs.

Getting the Best Quote Requires Shopping Around

Requesting a single quote from one insurer leaves money on the table. Idaho drivers who compare quotes from multiple carriers save substantially more than those who accept the first estimate they receive. Switching to coverage can yield savings when you compare quotes from competitors like GEICO, Progressive, State Farm, and Allstate, though actual savings depend on your specific profile and coverage needs. The only way to know if you’re getting a competitive rate is to gather quotes from at least three different insurers and compare them side-by-side using identical coverage limits and deductibles. When you pull quotes, ensure each one reflects Idaho’s required minimums of 25/50/15 bodily injury and property damage limits, plus your chosen uninsured and underinsured motorist levels. A quote from one carrier might show $1,500 annually for 100/300/100 limits with a $500 deductible, while another insurer quotes $1,650 for the exact same coverage. That $150 difference compounds over years, making comparison shopping a practical necessity rather than an optional step.

Bundling Policies Delivers Real Savings

Most Idaho drivers carry multiple insurance policies-auto, home, renters, or umbrella coverage-yet fail to bundle them with a single insurer. Carriers offer bundle discounts that meaningfully reduce your total premium across all policies. Bundling auto and home insurance typically saves 15 to 25 percent on your combined costs, though the exact discount varies by insurer and your specific situation. When you request a quote, ask whether the insurer offers bundling discounts and what coverage types qualify.

Farm Bureau and national carriers offer varying bundling discounts, so comparing them side by side reveals which combination saves you the most. If you own a home in Idaho, bundling becomes especially valuable because homeowners insurance premiums are substantial enough that a 15 percent reduction translates to real money. Conversely, if you rent and carry only auto insurance, bundling may not apply unless you add renters coverage.

Safe-Driving Programs and Usage-Based Discounts

Some insurers offer discounts through safe-driving programs. These programs track your actual driving habits and reward safe behavior with lower premiums. You’ll need to install a mobile app or device in your vehicle, but the potential savings justify the minor inconvenience for many drivers.

Maximize Discounts When You Request Quotes

Request quotes that include all available discounts for your situation: good grades if you have teen drivers, online purchase discounts, paying in full rather than monthly, and safety features on your vehicle like airbags or anti-lock brakes. The difference between a quote that excludes discounts and one that includes every applicable discount can exceed $300 per year on a standard policy. Each discount you qualify for stacks on top of the others, so the cumulative effect matters significantly.

Once you’ve gathered competitive quotes with all applicable discounts, the next step involves understanding what happens after you select a policy and how to maintain those rates over time.

What Mistakes Cost You Most on Car Insurance

Underestimating Your Coverage Needs

Selecting a coverage level that sounds reasonable at quote time often proves inadequate when you actually need it. Idaho’s state minimum coverage limits of $15,000 in Property Damage Liability leaves you dangerously exposed-a serious accident with medical bills exceeding $25,000 per person means you personally cover the remainder, and property damage liability of just $15,000 won’t touch a $40,000 vehicle collision. According to the Insurance Information Institute, state minimums frequently fail to cover actual crash costs, yet drivers choose them anyway to save $50 to $100 monthly. That math inverts instantly when a claim arrives.

Carrying 100/300/100 limits costs roughly $50 to $100 more per year than minimums but protects your assets and income from lawsuits. The mistake isn’t choosing low coverage-it’s failing to calculate what happens if you cause serious injury. A single at-fault accident pushes your premium from $1,476 per year to approximately $2,023 per year according to Bankrate data, so the savings from low limits evaporate the moment you file a claim.

Rejecting Uninsured and Underinsured Motorist Protection

Your uninsured and underinsured motorist coverage deserves equal attention. Idaho requires insurers to offer these protections, yet many drivers reject them to trim $10 to $30 monthly from their premium. If an uninsured driver hits you, this coverage protects your medical bills and lost wages-rejecting it transfers that risk entirely to you.

Skipping Annual Policy Reviews

Annual policy reviews separate drivers who pay accurately from those who overpay year after year. Life changes-moving within Idaho, adding a vehicle, or changing jobs-directly affect your quote, yet most drivers never contact their insurer to update their information. Comparing quotes on a single website shows only carriers that pay to advertise there, masking better rates elsewhere; the same principle applies to your existing policy. Moving from Kootenai at $2,105 per year to Kuna at $1,636 per year saves $469 annually without changing your vehicle or coverage, but only if you report the address change and request a new quote.

Similarly, reducing your annual mileage from 12,000 to 5,000 miles qualifies you for low-mileage discounts that insurers won’t apply unless you ask. Failing to report life changes creates a second problem: your insurer may deny claims if material information changed without notification. Divorce, job changes that alter your commute distance, or adding a teen driver to your policy all shift your premium-ignoring these updates means you’re either overpaying or underinsured.

Taking Action When Life Changes

Contact your agent whenever significant life events occur. The cost of that conversation takes minutes and frequently reveals $200 to $400 in annual savings through discounts you’ve become eligible for but never applied. Moving to a new Idaho city, changing employers, or adjusting your driving patterns all warrant a policy review and updated quote.

Final Thoughts

Accurate Idaho car insurance quotes require you to provide honest information about your vehicle and driving history, compare multiple quotes side-by-side, and review your coverage annually as your life changes. The difference between overpaying and finding a competitive rate often exceeds $300 per year, which means the time you invest in gathering quotes pays for itself within months. A local Idaho agent eliminates the confusion from quote shopping by gathering your information once and pulling quotes from multiple carriers simultaneously, ensuring each quote reflects identical coverage levels and your specific situation.

At Matt Anderson Insurance, our agents understand Idaho’s unique driving conditions and local rate variations across cities like Kuna and Kootenai. We identify discounts you might miss on your own, explain the practical differences between coverage options, and support your claims if an accident occurs. Your next step is straightforward: contact a licensed agent, provide your vehicle and driving information, and request Idaho car insurance quotes that include all available discounts for your situation.

Within days, you’ll have competitive quotes that let you make an informed decision rather than guessing. If you own a home or rent, mention it so we can show you bundling savings. If you’ve experienced life changes recently, share those details so your quote reflects your current situation accurately.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.