Idaho Airbnb Insurance: Peace Of Mind For Short-Term Hosts

Your standard homeowners policy won’t protect your Airbnb rental. Insurance companies exclude short-term rentals because guest turnover creates higher risks for property damage and liability claims.

At Matt Anderson Insurance, we help Idaho hosts understand their coverage options. The right Idaho Airbnb insurance policy protects your investment and gives you genuine peace of mind.

Why Your Standard Homeowners Policy Falls Short

Your homeowners insurance policy was designed for one scenario: you living in your home year-round. The moment you list your property on Airbnb or VRBO, that coverage evaporates. Insurance companies explicitly exclude short-term rentals because the risk profile changes dramatically. Constant exposure to strangers creates higher property damage claims and liability exposure that standard policies simply don’t address. According to data from Airbtics, Boise alone has 1,395 Airbnb listings that generate around $31,000 in revenue per listing annually. That income matters, but your standard homeowners policy won’t protect it if a guest causes damage or injury. Most hosts don’t realize their claim will be denied until it’s too late. We’ve seen this happen repeatedly with Idaho hosts who thought their existing coverage would apply to rental activity. It won’t.

The Real Cost of Underinsurance

Guest damage happens more frequently than most hosts expect. A broken window, damaged furniture, or stained flooring might seem minor, but repair costs add up fast. More serious incidents-a guest injury on your property or theft of valuables-create liability exposure that reaches far beyond the damage itself. Idaho law requires short-term rental properties to carry at least $1,000,000 in liability insurance coverage. Your homeowners policy typically provides $100,000 to $300,000 in liability coverage, leaving a massive gap. If a guest is injured and sues, you become personally responsible for anything above your policy limit. Additionally, standard policies don’t cover loss of rental income. If your property becomes uninhabitable due to a covered loss, you lose bookings and revenue with no compensation. A dedicated short-term rental policy covers actual loss sustained-meaning you receive compensation for the income you would have earned during the vacancy period.

What Dedicated Rental Insurance Actually Covers

Specialized short-term rental policies address the specific risks you face as a host. They include comprehensive building coverage with replacement cost for both structure and contents, general liability protection for guest-related injuries or property damage, and property entrustment coverage that protects against theft and guest-caused damage. Business revenue protection covers lost bookings and canceled reservations after a covered claim. Some policies even include bed bug and flea protection, squatter protection if a guest refuses to leave, and liquor liability coverage if alcohol is served on the property.

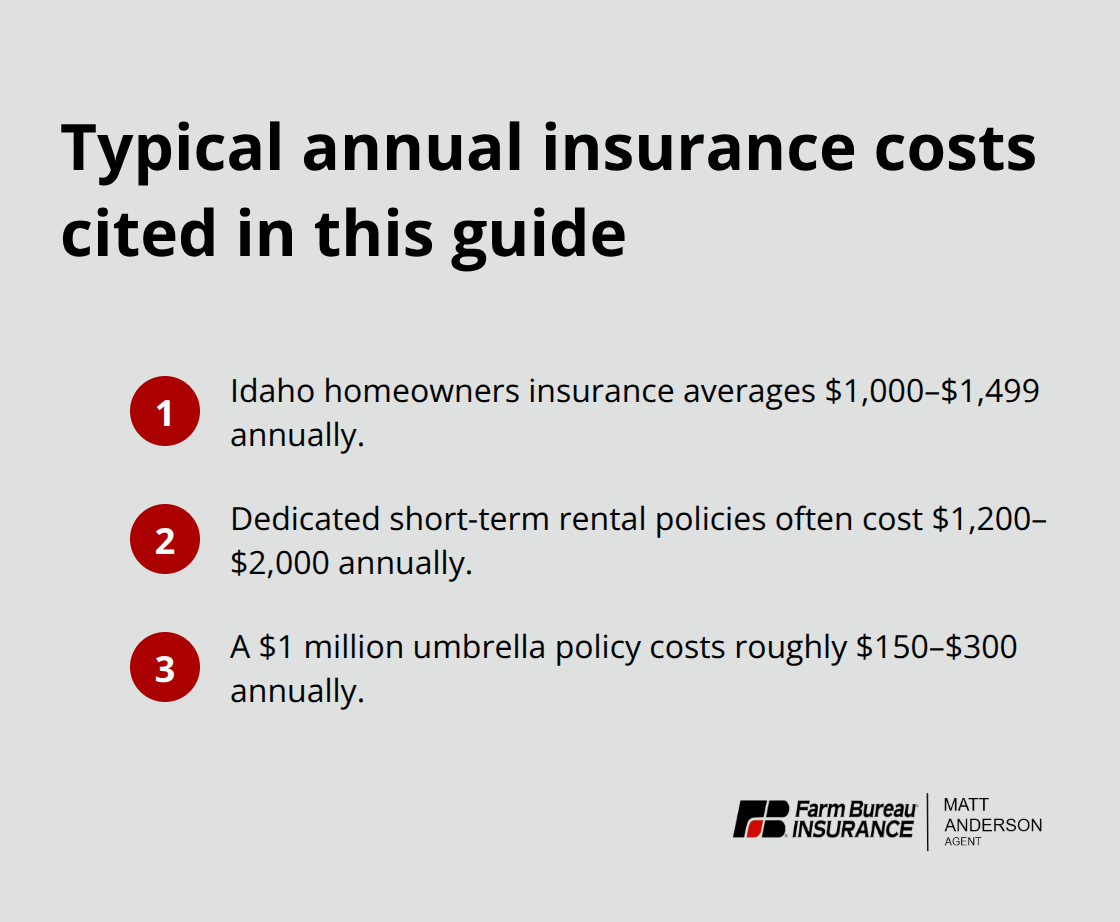

These coverages don’t exist in homeowners policies. The cost difference matters too. Idaho homeowners insurance averages $1,000 to $1,499 annually according to U.S. Census Bureau data, but dedicated short-term rental policies are competitively priced and often bundle multiple protections that would cost far more to obtain separately. Working with an agent experienced in Idaho rental properties ensures you’re not overpaying for coverage you don’t need while closing gaps in areas where you do.

Finding the Right Coverage for Your Situation

The gap between what you think you’re covered for and what you actually are covered for can cost you thousands. Your next step is to explore the specific coverage options available to Idaho hosts-from platform protections to standalone policies that give you complete control over your coverage limits.

Coverage Options for Idaho Short-Term Rental Hosts

Airbnb’s Host Protection Has Serious Limits

Airbnb’s host protection program sounds appealing until you read the fine print. The platform offers up to $1 million in liability coverage, but this coverage only activates when Airbnb’s own insurance is triggered-typically after your personal policy denies a claim. That means you rely on a backup safety net rather than primary protection. More critically, Airbnb’s coverage excludes loss of income from canceled bookings, theft by guests, and damage caused by guests during their stay. You also navigate Airbnb’s claims process, which can take months to resolve. Idaho hosts cannot rely on platform protection alone.

Dedicated Short-Term Rental Policies Provide Primary Coverage

A dedicated short-term rental policy covers your property as the primary insurer from day one. These policies include comprehensive building coverage with replacement cost for both your structure and contents, general liability protection starting at $1 million (meeting Idaho’s legal requirement), and business revenue protection that compensates you for actual income lost during vacancy. Specialized insurers offer bed bug and flea protection, squatter protection if a guest refuses to leave, and amenities liability coverage for bikes, kayaks, pools, and hot tubs. This specialized approach means you own complete protection tailored to your rental operation rather than gambling on a platform’s secondary coverage. The cost remains competitive with standard homeowners policies, often between $1,200 and $2,000 annually depending on your property type and coverage limits-reasonable given the scope of protection.

Umbrella Coverage Protects Your Personal Assets

Umbrella coverage acts as your final safety layer, and it’s not optional if you’re serious about asset protection. A $1 million umbrella policy costs roughly $150 to $300 annually and covers liability claims that exceed your primary policy limits. If a guest suffers a serious injury on your property and wins a $2 million lawsuit, your dedicated rental policy covers the first $1 million and your umbrella covers the remaining $1 million, protecting your personal assets.

Idaho hosts who own their properties outright should absolutely carry umbrella coverage; those with mortgages face lender requirements for liability protection anyway.

Structuring Your Complete Protection Strategy

Work with a local agent who understands Idaho rental risks and can bind coverage quickly. The right combination of dedicated short-term rental coverage and umbrella protection means you’re genuinely protected when claims happen. Your agent helps you evaluate property type, guest volume, and local regulations to select appropriate coverage limits. Once you understand what protection looks like, the next step involves comparing specific policies and deductibles to find the right fit for your situation.

How to Choose the Right Insurance for Your Idaho Rental

Match Coverage to Your Property and Guest Patterns

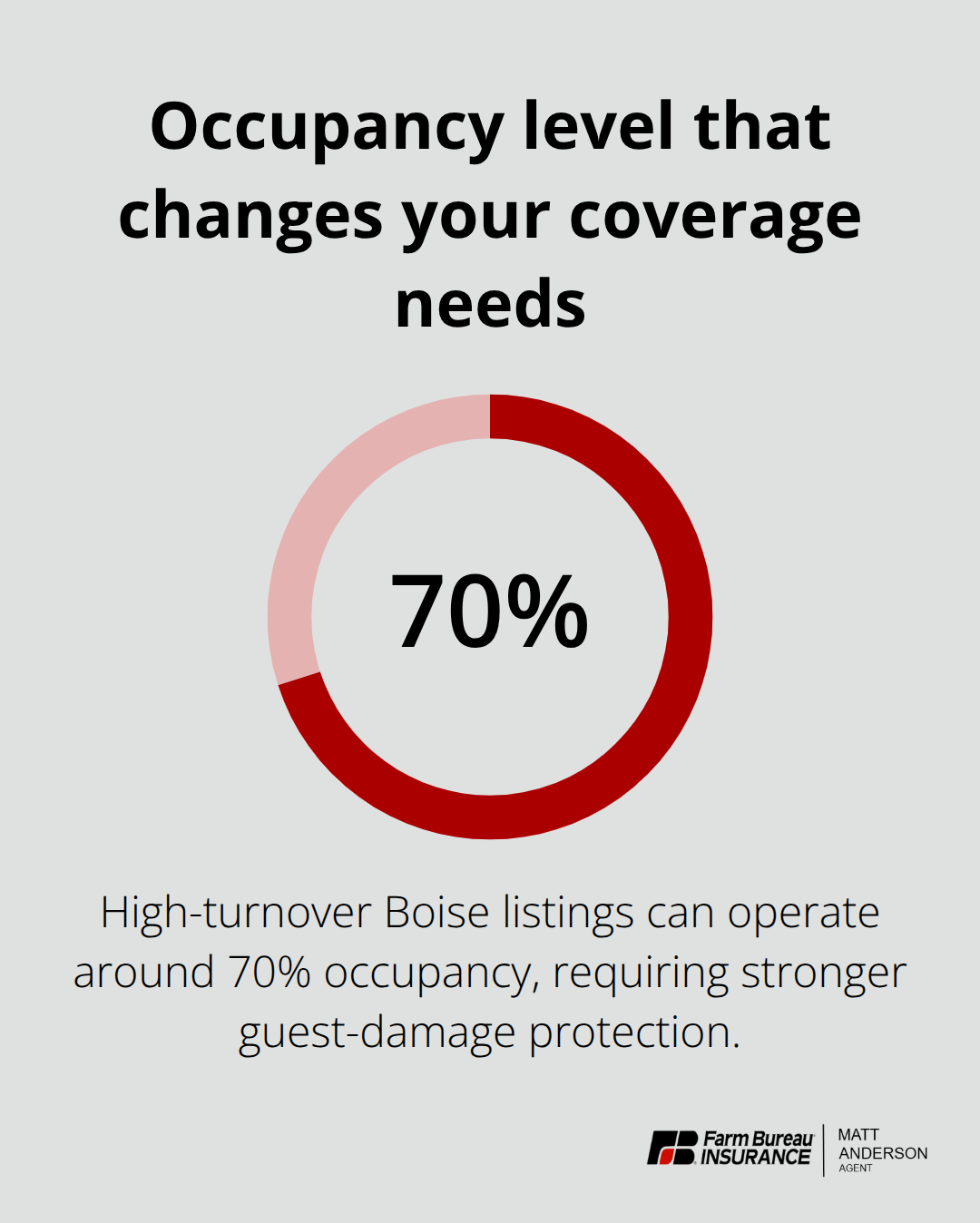

Start with the specifics of your property, not general insurance talk. A cabin in McCall that hosts families during ski season faces different risks than a downtown Boise apartment renting to business travelers year-round. Your property type, occupancy patterns, and guest demographics directly determine the coverage limits you actually need. A 2-bedroom apartment generating around $31,000 annually according to Airbtics data requires different protection than a luxury vacation home. High-turnover properties with 70% occupancy like many Boise listings need robust guest damage coverage and frequent replacement cost assessments. Properties with lower occupancy can sometimes reduce coverage limits without sacrificing protection.

Your guest volume matters because frequent turnover increases the statistical likelihood of property damage, theft, and liability claims. Ask yourself: Do you host families or solo travelers? Are guests primarily local or international? Do you allow pets? Do you serve alcohol? These answers shape which coverage options actually protect you. A property that allows pets needs animal liability coverage with no breed restrictions-a standard homeowners policy won’t touch this. A property where guests consume alcohol needs liquor liability protection, another exclusion in traditional policies.

Calculate your annual revenue realistically using data from your listings or platforms like Airbtics, then ensure your business revenue coverage matches that income. If you generate $30,000 annually, your loss-of-income coverage should reflect that threshold. Idaho hosts commonly underestimate this number and end up with coverage limits that don’t match actual revenue.

Select Deductibles and Liability Limits Based on Your Financial Reality

Coverage limits and deductibles require honest assessment of your financial position, not wishful thinking. Idaho law mandates $1,000,000 in liability coverage for short-term rentals, so that’s your floor, not your ceiling. If a guest suffers a serious injury and sues for $2 million, a $1 million policy leaves you personally liable for the difference. Dedicated short-term rental policies typically offer $1 million to $2 million in liability; choosing the higher limit costs roughly $200 to $400 more annually but protects your assets substantially.

Your deductible directly impacts your out-of-pocket costs when claims happen. A $500 deductible means you pay $500 for each claim; a $2,500 deductible reduces your premium but increases your financial exposure. High-volume hosts with frequent minor claims benefit from lower deductibles; hosts with minimal claims history can absorb higher deductibles and lower premiums. Building and contents coverage should reflect replacement cost, not actual cash value. If your furnishings cost $15,000 to replace and a guest damages them, replacement cost coverage pays the full amount; actual cash value accounts for depreciation and leaves you short.

Work with Local Idaho Agents Who Understand Rental Risks

Work with a local Idaho agent who handles short-term rental properties regularly. These agents understand Idaho’s specific risks-wildfire exposure in forested areas, seasonal rental patterns in resort communities, and local regulatory requirements that changed significantly after House Bill 583 took effect July 1, 2026. A local agent binds coverage quickly, answers claims questions directly, and helps you select the right insurance policy as your rental operation grows.

Compare quotes from multiple insurers; prices and coverage terms vary substantially. Some insurers specialize in short-term rentals while others treat them as afterthoughts. An agent experienced with properties like yours identifies gaps that generalist insurers miss and explains trade-offs between coverage options in plain language.

Final Thoughts

Your Idaho Airbnb insurance protects your income, your assets, and your ability to operate without constant financial anxiety. Standard homeowners policies leave you exposed to thousands in potential losses, while dedicated short-term rental coverage closes those gaps with comprehensive protection designed specifically for hosts. Airbnb’s host protection provides a secondary safety net, but a primary policy gives you control from day one, and adding umbrella protection creates a complete defense against liability claims that exceed your primary limits.

Idaho’s regulatory environment supports responsible hosts, and House Bill 583 eliminated many local restrictions on short-term rentals while keeping the $1 million liability requirement firm. Wildfire risk in Idaho’s forested regions continues to rise, making comprehensive property coverage essential for hosts in affected areas. The cost of proper coverage remains competitive with standard homeowners insurance, typically between $1,200 and $2,000 annually depending on your property and coverage selections.

Contact a local Idaho agent who understands short-term rental risks and can match your specific situation to the right coverage. At Matt Anderson Insurance, our licensed agents specialize in protecting Idaho hosts with comprehensive short-term rental coverage and umbrella policies that reduce your overall insurance costs. Get a quote today and stop gambling with inadequate coverage.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.