Idaho Contractor Insurance Coverage: What It Includes For Builders

Running a construction business in Idaho means managing real risks every day. One accident or lawsuit can drain your finances fast, which is why Idaho contractor insurance coverage matters so much.

At Matt Anderson Insurance, we’ve seen builders lose everything because they skipped the wrong coverage type. This guide shows you exactly what protection you need and where most contractors leave themselves exposed.

What Your Contractor Insurance Actually Protects

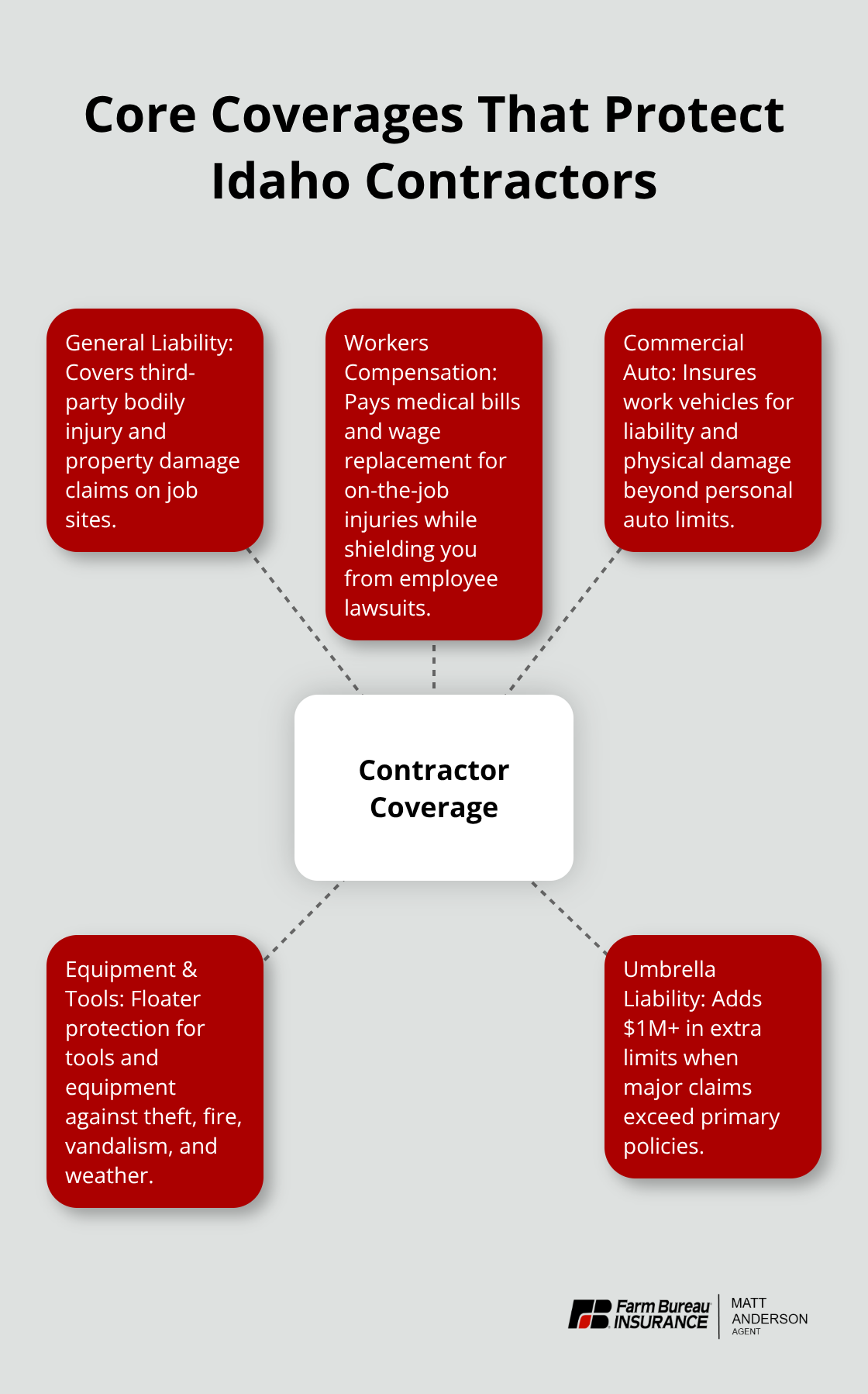

General Liability Coverage on the Jobsite

General liability insurance covers the accidents that happen on your jobsite. When a homeowner slips on wet concrete and breaks their arm, or you accidentally damage their water line while digging, general liability pays their medical bills and repair costs. The Hartford, identified by MoneyGeek as a top Idaho general liability insurer, offers coverage starting around $77 per month, but here’s what matters: Idaho law requires only a $300,000 minimum, yet the practical standard in Idaho construction is now $1 million per occurrence and $2 million aggregate. This gap exists because real accidents exceed minimums. A single serious on-site injury can easily cost $100,000 or more in medical bills, legal fees, and settlements.

Property damage coverage within your policy responds when you damage a client’s roof, their interior finishings, or their landscaping. Legal defense costs are included in most policies and get paid regardless of whether you’re found liable-this protects your cash flow during disputes. When you shop quotes, ask whether defense costs are paid inside your limits or separately, because this changes how much coverage remains for actual settlements.

Workers’ Compensation and Equipment Protection

Workers’ compensation insurance is mandatory in Idaho if you have employees. It covers medical expenses, rehabilitation, and lost wages when someone gets hurt on the job. You’ll need proof of workers’ compensation or an exemption statement to register with the Idaho Contractors Board for projects over $2,000. Tools and equipment protection keeps your gear safe from theft, fire, and vandalism-critical because replacing stolen power tools or a damaged compressor can halt projects and kill your cash flow.

Matching Coverage Limits to Your Projects

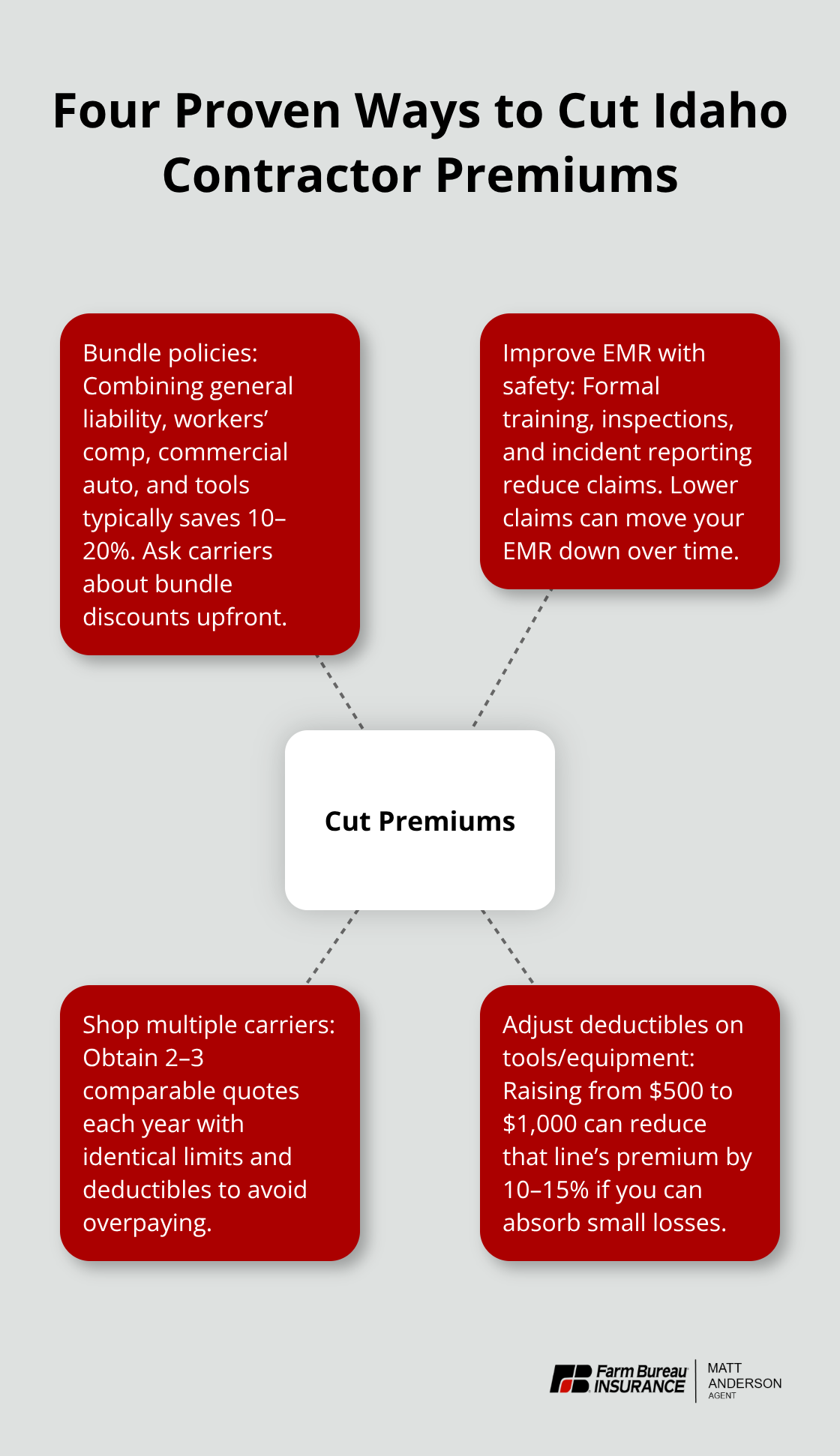

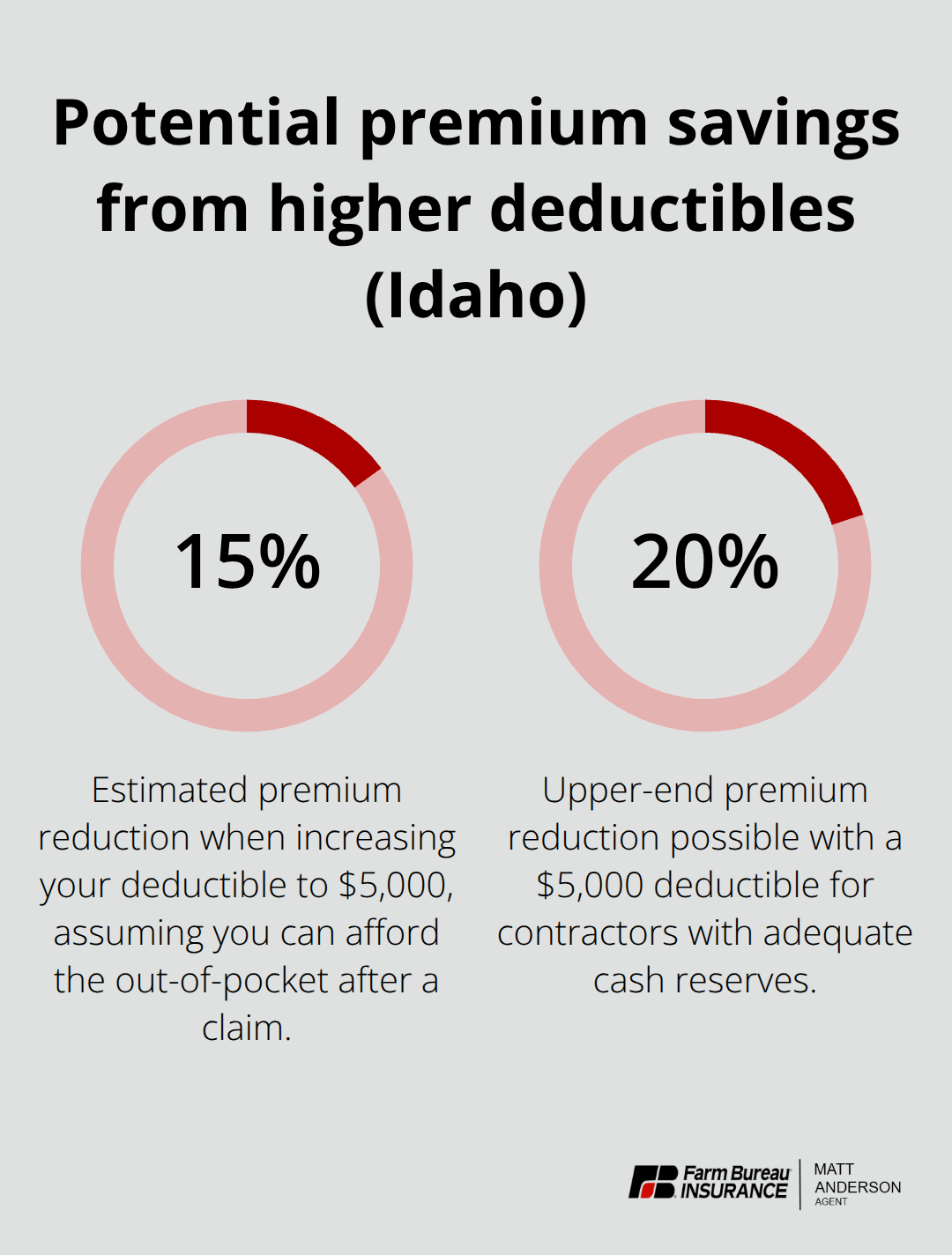

Match your coverage limits to your actual project value: for jobs under $50,000, a $500,000 limit can work; for projects over $500,000 or on commercial properties, $1 million per occurrence is prudent. Deductibles matter too. Common Idaho deductibles are $1,000 or $2,500, but raising it to $5,000 can cut your premiums by 15 to 20 percent if you can absorb that out-of-pocket cost after a claim. Shop quotes from at least three Idaho-licensed insurers and provide them with your annual revenue, number of employees, typical project types, and project values so they can tailor limits and endorsements to your actual risk profile.

These details help insurers identify the specific protections your construction business actually needs, which sets the stage for understanding where most builders leave themselves exposed.

Why Idaho Builders Must Carry Contractor Insurance

Registration Requirements Protect You Legally, Not Financially

The Idaho Contractors Board mandates registration for any project exceeding $2,000 in materials and labor. Registration requires proof of general liability insurance with at least a $300,000 single limit before you can even apply, yet this minimum falls far short of real-world protection. In fiscal year 2025, Idaho’s Department of Professional and Licensing recorded 485 contractor complaints-the highest among all boards and commissions-which shows that registration alone does not shield contractors or their clients from financial disaster. Operating without current coverage carries severe penalties: up to $1,000 in fines, six months in jail, loss of building permits, and forfeiture of lien rights on projects. These consequences mean you cannot legally collect payment for work if you lack proper insurance, making compliance both a legal obligation and a business necessity.

Lawsuits Cost Far More Than You Expect

Lawsuits happen whether you anticipate them or not, and they cost far more than most builders expect. A homeowner suing over water damage to their home, a worker injured on your jobsite, or property damage claims can easily exceed $100,000 when medical bills, legal defense costs, and settlements combine. Without adequate coverage, these costs come directly from your personal savings and business accounts. Contractors with only the state minimum of $300,000 face serious exposure on larger projects because a single accident can consume that entire limit and leave you personally liable for anything beyond it.

On-Site Accidents Create Immediate Financial Exposure

On-site accidents involving employees or third parties generate medical expenses, lost wages, rehabilitation costs, and often legal fees that drain cash flow fast. Workers’ compensation insurance covers your employees’ medical care and lost wages when they get hurt, which is mandatory if you have staff, while general liability covers injuries to clients, property owners, and bystanders on your jobsite. Without these protections in place, one serious injury could force you to close your business. Contractors who carry adequate coverage-the market standard of $1 million per occurrence and $2 million aggregate-handle real-world accidents without personal financial ruin and build credibility with property owners and general contractors who increasingly require proof of coverage before awarding contracts. This standard coverage level positions you to win bids and protect your business, which leads directly to understanding the specific gaps that most builders overlook.

Common Coverage Gaps Idaho Builders Miss

Completed Operations Coverage Protects Work After Project Completion

Your general liability and workers’ compensation policies handle the obvious risks, but they leave critical gaps that cost builders thousands when accidents happen. Completed operations coverage protects you after a project finishes-this is where most contractors get blindsided. Standard general liability policies cut off coverage the moment you leave the jobsite, but problems surface later. A roof you installed leaks six months after completion, or flooring you laid buckles from moisture damage. The homeowner files a claim, and your insurance denies it because the work is complete.

Contractors who carry completed operations coverage stay protected for years after project handoff, which is why this endorsement matters more than most realize. Ask your insurer whether your current policy includes products-completed operations coverage, and if not, add it immediately. The cost runs minimal-often $200 to $500 annually depending on your revenue-compared to paying out-of-pocket for repairs that could total $10,000 or more.

Pollution Liability Covers Environmental Damage Claims

Environmental damage claims arise when you accidentally contaminate soil or groundwater during excavation, or when fuel spills from equipment damage your client’s property. Standard general liability policies exclude pollution, leaving you personally liable for cleanup costs that state and federal regulations can force onto property owners. These gaps exist in most contractor policies because insurers assume you’ll address them separately-but most builders never do.

When you request quotes from Idaho insurers, specifically ask about pollution liability endorsements. This addition costs $300 to $800 annually but prevents catastrophic exposures that could exceed $50,000 or more on a single claim.

Hired and Non-Owned Vehicle Coverage Fills Transportation Gaps

Hired and non-owned vehicle coverage fills the gap when you rent equipment or use a subcontractor’s vehicle for jobsite transport. If that rented excavator causes property damage, or a subcontractor’s truck injures someone while hauling your materials, your standard auto policy may not respond because the vehicle isn’t owned by your business. These gaps exist in most contractor policies because insurers assume you’ll address them separately-but most builders never do.

When you request quotes from Idaho insurers, specifically ask about hired and non-owned vehicle coverage. This addition costs $300 to $800 annually but prevents catastrophic exposures that could exceed $50,000 or more on a single claim. Your registration with the Idaho Contractors Board requires general liability proof, yet that minimum protection leaves you exposed on every project. Build a complete coverage picture by identifying these gaps now rather than discovering them during a claim.

Final Thoughts

Your Idaho contractor insurance coverage must match the real risks you face on every project. General liability, workers’ compensation, and equipment protection form the foundation, but completed operations, pollution liability, and hired vehicle coverage fill the gaps that sink most builders. The state minimum of $300,000 in general liability satisfies legal requirements, yet the market standard of $1 million per occurrence and $2 million aggregate exists because real accidents exceed minimums.

Start by gathering your business details: annual revenue, number of employees, typical project types, and project values. Request quotes from at least three Idaho-licensed insurers and ask specifically about endorsements for completed operations, pollution liability, and hired and non-owned vehicle coverage. A $500 annual investment in completed operations coverage prevents $10,000 repair bills you would pay out-of-pocket, while pollution and vehicle endorsements cost similarly but protect you from exposures that could exceed $50,000 on a single claim.

We at Matt Anderson Insurance work with Idaho contractors to build complete coverage that protects your business, your employees, and your clients. Contact us today to review your current coverage and identify the gaps that could cost you thousands.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.