Idaho Auto Insurance Discounts: Ways To Lower Your Premiums

Idaho auto insurance premiums don’t have to drain your budget. There are real discounts available right now that most drivers overlook, and we at Matt Anderson Insurance want to show you exactly how to claim them.

This guide walks through the discounts you qualify for, proven strategies to cut costs, and how working with a local agent gets you the best rates in your area.

Idaho Auto Insurance Discounts That Actually Lower Your Premiums

Safe Driving Rewards Your Clean Record

Safe driving is the single most effective way to reduce what you pay for auto insurance in Idaho, and carriers reward it aggressively. If your household has no accidents or traffic violations, you qualify for a good driver discount that can lower your premium noticeably. State Farm, for example, offers a Good Driving Discount for drivers without claims in the household, and their Defensive Driving Course Discount applies to drivers 55 and older who completed an approved Motor Vehicle Accident Prevention Course within the last three years. A clean driving history directly translates to lower premiums, and staying accident-free protects that discount year after year.

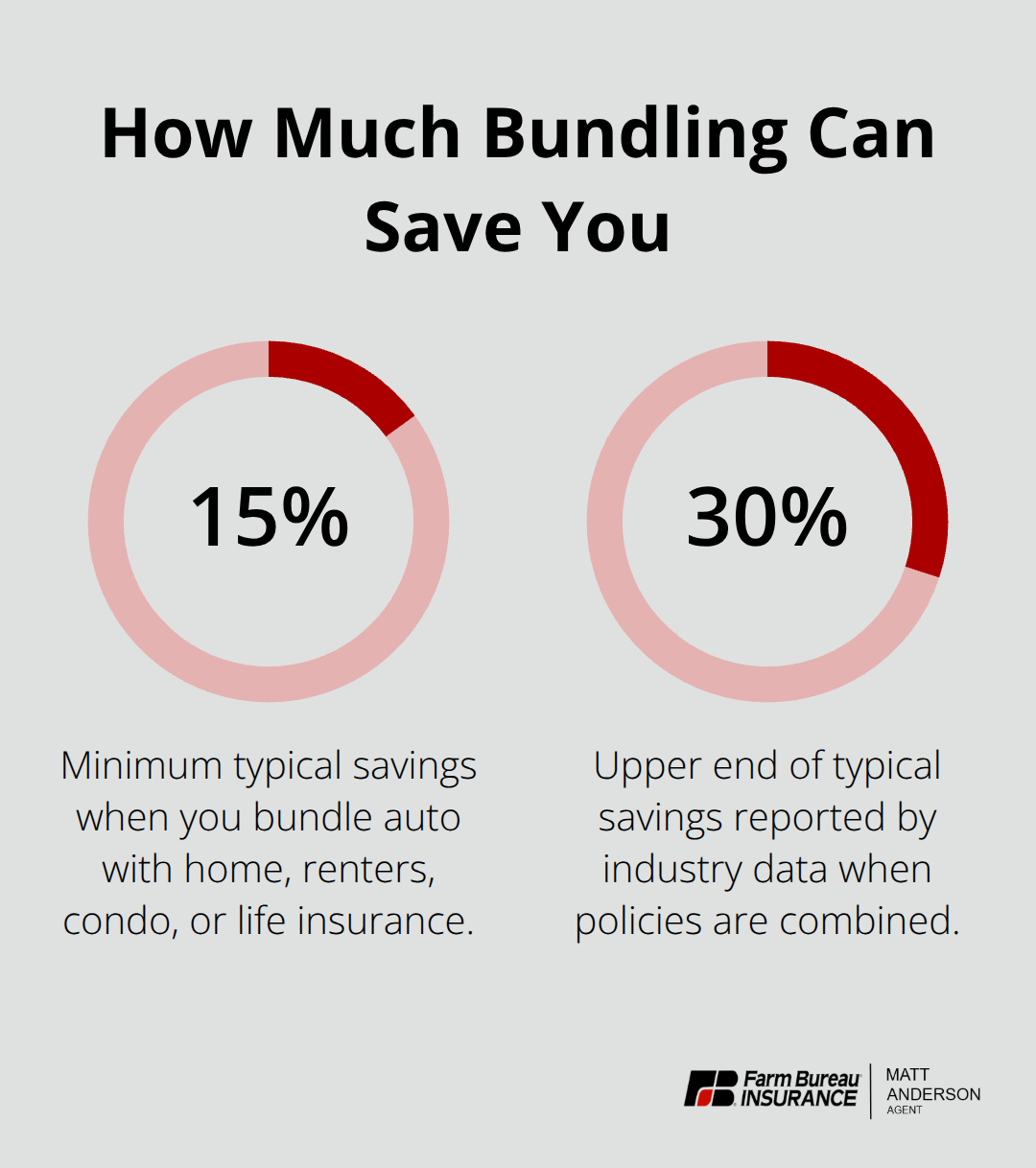

Bundling Multiple Policies Unlocks Substantial Savings

Beyond safe driving, bundling multiple policies with the same insurer delivers substantial savings. When you combine auto with homeowners, renters, condo, or life insurance, you can save 15–30% according to industry data-and sometimes more depending on which carrier you choose. Bundling works because insurers reward customer loyalty and the reduced administrative cost of managing multiple policies under one roof. If you insure a home and a vehicle separately with different companies, you leave hundreds of dollars on the table each year.

Student Discounts Recognize Academic Responsibility

Good student discounts apply to drivers under a certain age (typically 25) who maintain a B average or higher, or to full-time students who leave their vehicle at home while away at school. This discount recognizes that academic responsibility correlates with safer driving behavior. The discount typically ranges from 5% to 10%, depending on the carrier and your specific situation. A young driver with good grades, a clean record, and bundled policies can stack discounts that compound into meaningful annual savings.

Vehicle Safety Features and Additional Discounts

Vehicle safety features also matter: anti-theft devices and advanced safety technology can reduce your premium, and some carriers now offer discounts for electric vehicles. You may qualify for multiple discounts simultaneously, and the key is asking your agent about every discount you might qualify for-carriers don’t automatically apply them all. Most drivers miss discounts related to affiliations, payment methods, or specific vehicle features simply because they didn’t ask. Annual policy reviews catch these opportunities and help you adjust coverage to match your actual driving patterns and life circumstances, which sets the stage for the next critical step: knowing which strategies actually maximize your savings beyond discounts alone.

Strategies To Maximize Your Savings on Auto Insurance

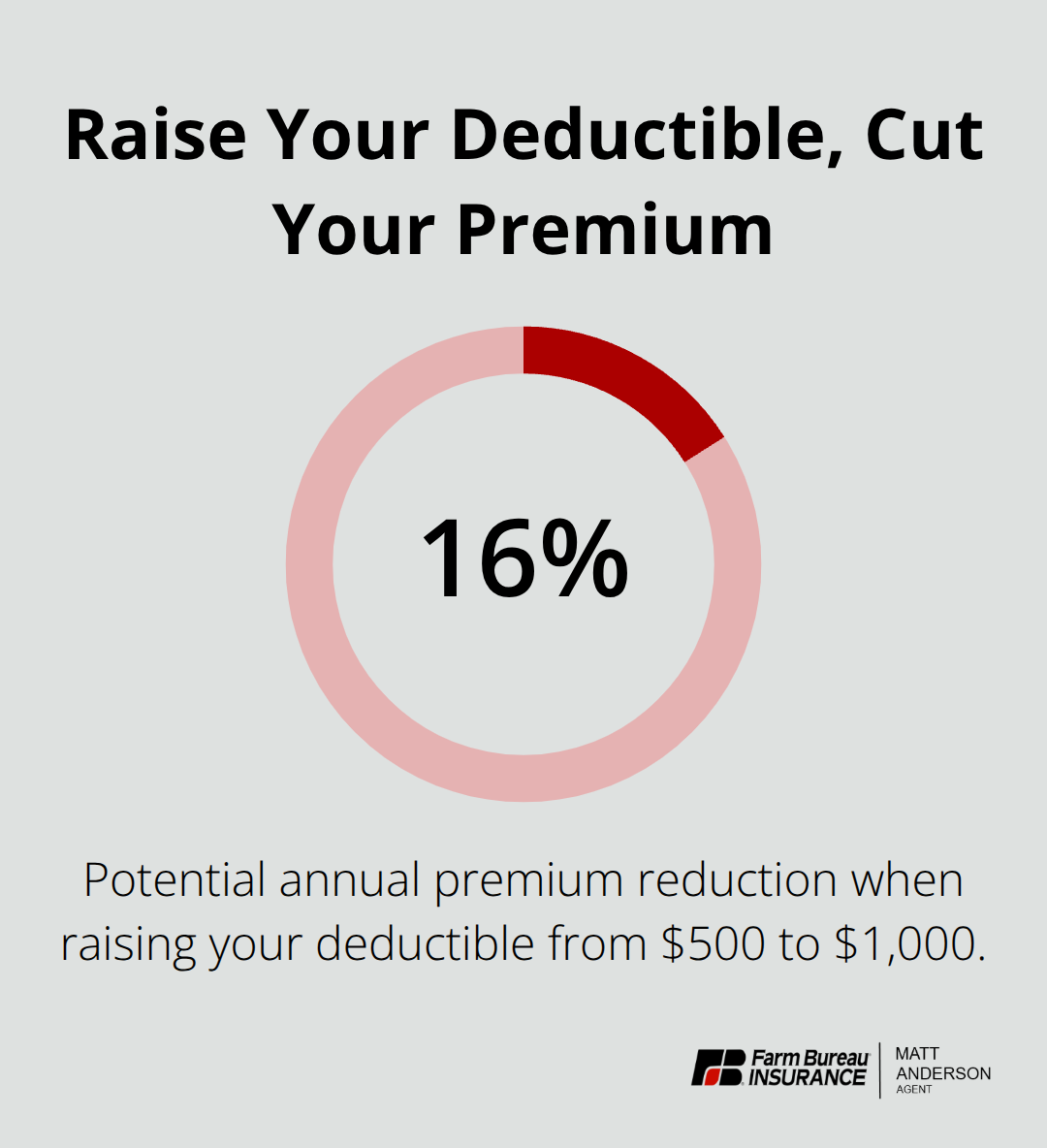

Increase Your Deductible to Lower Monthly Payments

The fastest way to lower your premium starts with deductible decisions. Increase your deductible from $500 to $1,000 and you can reduce your annual premium by up to 16 percent. The math is straightforward: a $500 increase in deductible saves you real money every month, and unless you file a claim every few years, you come out ahead.

However, this strategy only works if you can actually afford to pay $1,000 out of pocket when an accident happens. If a $1,000 unexpected expense would strain your budget, stick with the lower deductible even if your premium stays higher. Make an intentional choice based on your savings capacity, not on chasing the lowest premium regardless of whether you can cover the deductible.

Match Your Coverage to Your Vehicle’s Actual Value

Your coverage mix matters more than most drivers realize. Many people carry full coverage on a vehicle worth $6,000 while paying $1,200 yearly in collision and comprehensive premiums, which means they recover their car’s entire value in five years of claims. If your vehicle is older or has low market value, dropping collision coverage saves hundreds annually and makes mathematical sense. Conversely, if you financed or leased your vehicle, your lender requires full coverage, so this decision is already made for you. Annual policy reviews catch these misalignments and help you identify what coverage actually protects you versus what you’re paying for unnecessarily.

Adjust Coverage Based on Your Driving Patterns

Your driving patterns directly affect which coverage you need. If you work from home and drive 5,000 miles yearly instead of 15,000, you may qualify for low-mileage discounts or usage-based programs that reward lighter driving. Set a calendar reminder each year to review your vehicle values, your driving patterns, and your coverage limits. This annual check ensures your policy reflects your real life, not coverage that made sense five years ago. Idaho Department of Insurance resources and local agents can help you identify which coverage actually protects you and which policies you can safely reduce.

Why Local Agents Beat Online Quotes Every Time

Online Platforms Show Only a Fraction of Available Rates

Shopping for auto insurance online feels fast, but speed costs you money. When you compare quotes on a single website, you see only carriers that pay to advertise there, not necessarily the ones offering the best rates for your specific profile. An independent agent accesses multiple carriers and runs your exact situation through each one, revealing rate differences that online tools simply miss. A driver in Boise might see a $1,200 annual quote online, but when an agent shops your profile across five carriers, one might quote $950 while another quotes $1,100-a $250 gap that compounds to thousands over a decade.

Agents Uncover Discounts You’d Never Find Alone

Agents catch discounts you would never find on your own. You might qualify for an affiliation discount through your employer, a good student discount you forgot about, or a bundling opportunity that stacks 15–30% in savings. Most online platforms ask basic questions and apply standard discounts, but they do not investigate your actual situation the way a local independent agent does. An agent reviews whether your current deductible aligns with your emergency savings, whether your coverage limits match Idaho’s rising repair costs, and whether dropping collision on that older vehicle makes sense financially.

This personalized approach takes 30 minutes of conversation but saves hundreds annually because the agent knows the carriers, knows Idaho’s market, and knows which combinations work best for drivers in your area.

Local Support Matters When Claims Happen

Claims support matters significantly. When you file a claim with an online carrier, you talk to a call center in another state. A local independent agent handles claims with knowledge of Idaho weather patterns, local repair shops, and how claims actually work in your community. An agent advocates for you during the claims process, explains what coverage applies versus what does not, and helps you navigate the complexity. Online quotes do not include that support-you handle everything alone when something goes wrong, which is exactly when you need someone in your corner.

Final Thoughts

Idaho auto insurance discounts work best when you combine them strategically with coverage that matches your actual situation. Safe driving records, bundled policies, and student discounts form the foundation, but your real savings come from reviewing your policy annually and adjusting your deductible and coverage limits to fit your vehicle’s value and driving patterns. The gap between what you pay now and what you could pay is often substantial, and most drivers never close it because they shop online once and assume they found the best rate.

Working with a local agent changes that equation entirely. An agent accesses multiple carriers at once instead of showing you only advertised options, identifies every discount you qualify for, and structures your coverage to protect you without overpaying. This conversation reveals which Idaho auto insurance discounts apply to your profile and how much you can actually save-often hundreds of dollars annually that online quotes miss.

Contact Matt Anderson Insurance for a personalized review of your current coverage and driving situation. The process takes 20 minutes, and most drivers find savings they did not know existed.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.