Idaho Liability Auto Insurance: Understanding Your Auto Liability Coverage

A single accident can wipe out your savings and damage your financial security for years. Idaho liability auto insurance is the legal shield that protects you from paying those costs out of pocket.

Most Idaho drivers carry only the minimum coverage required by law-and that’s a mistake. We at Matt Anderson Insurance see firsthand how inadequate limits leave drivers exposed to serious financial risk.

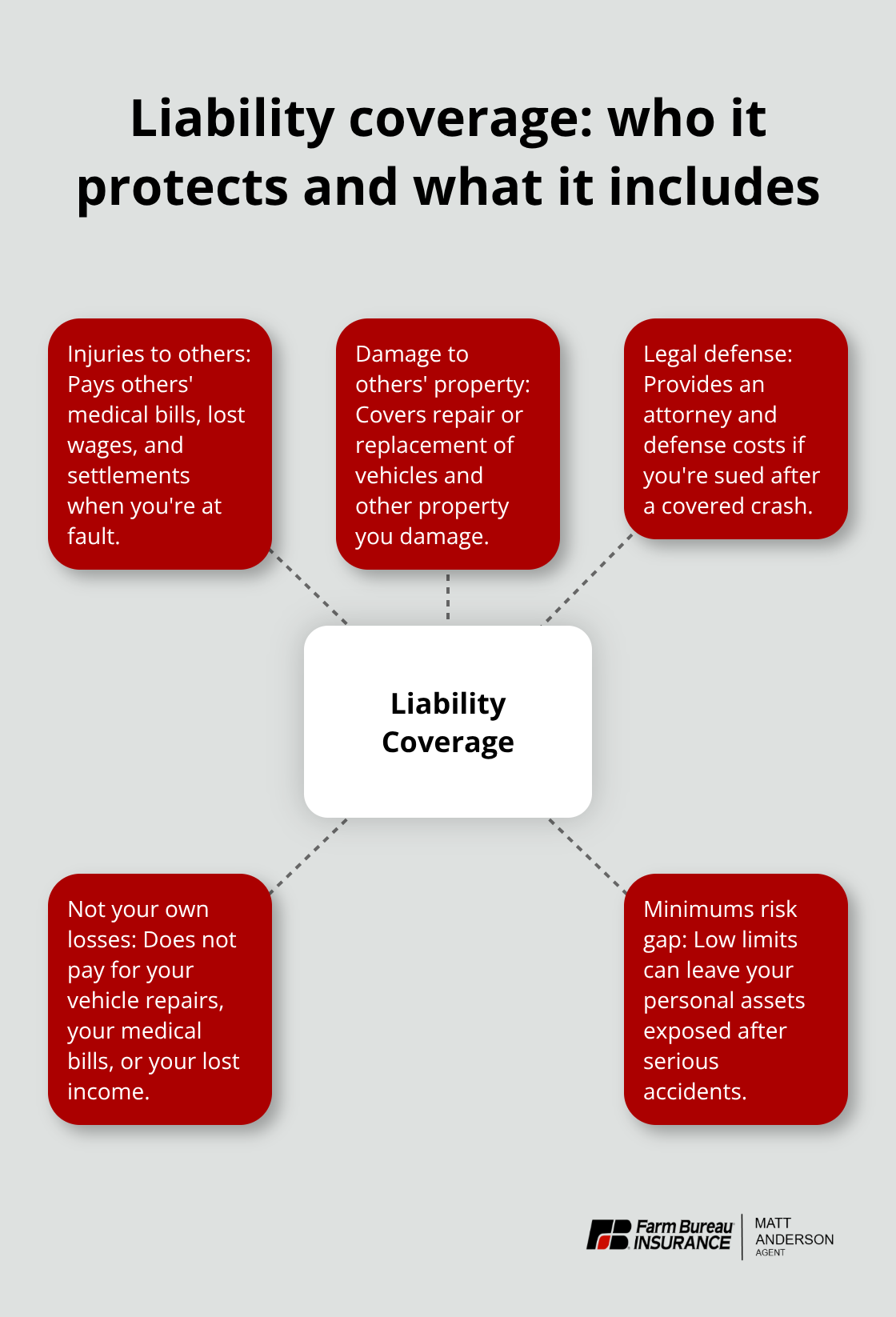

What Liability Coverage Actually Means

Auto liability insurance pays for injuries and property damage you cause to other people when you’re at fault in a crash. Idaho law requires you to carry a minimum of $15,000 in Property Damage Liability coverage, according to the Idaho Department of Insurance. If you hit another car and injure the driver, your bodily injury coverage pays for their medical bills, lost wages, and legal settlements up to your limit. Property damage liability covers the cost to repair or replace the other vehicle and any other property you damage. The critical distinction is that liability insurance protects the other person-not you. It doesn’t pay for your own vehicle repairs, your medical bills, or your lost income. That’s why so many Idaho drivers who carry only minimums end up financially devastated after serious accidents.

The Real Cost of Staying at Minimum Limits

Idaho’s minimum coverage amounts sound adequate until you see actual accident costs. A single serious injury claim can easily exceed $50,000 in medical expenses alone, not counting pain and suffering or long-term care. If you hit a vehicle with multiple occupants or cause injury to a high-income earner, you could owe far more than your policy covers. At that point, creditors can pursue your wages, bank accounts, and assets to satisfy the judgment. Moving from the state minimum to $100,000 per person and $300,000 per accident typically costs only an additional $10 to $20 per month, yet it dramatically reduces your personal liability risk. Many Idaho drivers don’t realize they can customize their limits to match their actual financial situation and the value of what they own.

How Liability Coverage Protects Your Long-Term Security

Without adequate liability coverage, a serious accident can trigger a lawsuit that follows you for years. Idaho courts regularly award damages well above the state minimums, especially in cases involving permanent injuries or multiple victims. Your liability policy also provides legal defense, meaning the insurance company pays for your attorney if you’re sued. This protection is invaluable because legal fees alone can reach tens of thousands of dollars before a case is resolved. Higher liability limits also give you negotiating power in settlement discussions-insurers with larger available coverage can resolve claims faster and for less total cost than fighting over inadequate minimums. The financial security you build through your home, retirement accounts, and business interests all becomes vulnerable if you’re underinsured.

What Happens When Your Limits Fall Short

Most Idaho drivers assume their minimum coverage will handle typical accidents. In reality, medical costs, vehicle damage, and legal judgments often far exceed what your policy can cover. A crash involving a newer luxury vehicle, multiple injured passengers, or long-term medical care can quickly exhaust your policy limits and leave you personally liable for the remainder. Courts don’t stop collecting damages just because your insurance runs out-they pursue your personal assets instead. This is where the gap between minimum coverage and adequate protection becomes painfully clear, and it’s why understanding your actual exposure matters far more than simply meeting the legal minimum.

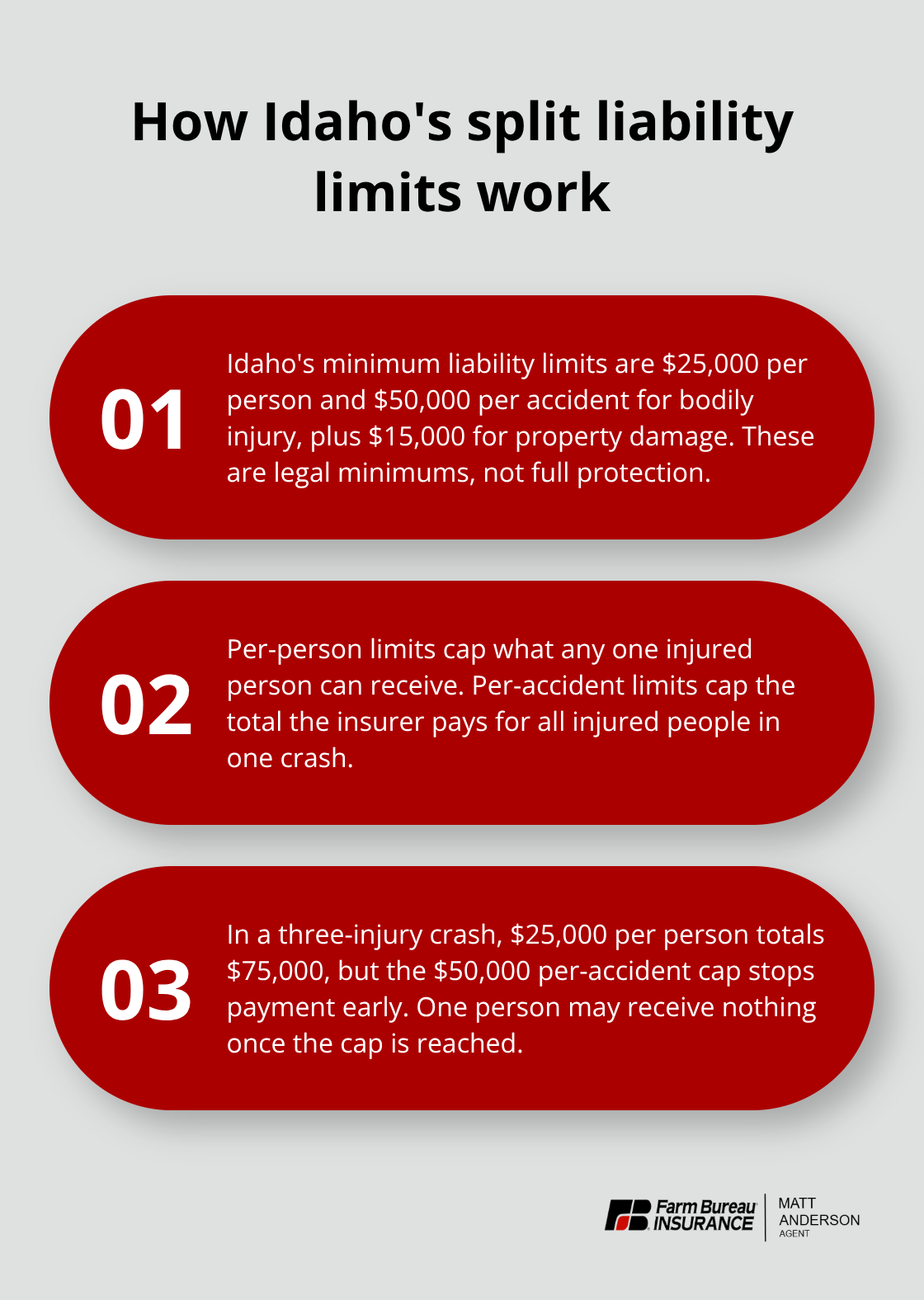

What Coverage Limits Actually Mean in Idaho

Bodily injury liability and property damage liability work together as your legal protection, but they operate independently with separate limits. Idaho’s minimum is $25,000 per person and $50,000 per accident for bodily injury, plus $15,000 per accident for property damage. The per-person limit applies to any single injured person, while the per-accident limit caps your total payout across all injured parties in one crash. If you cause an accident with three injured people and your limit is $25,000 per person, your policy pays up to $25,000 to each person-totaling $75,000-until you hit your per-accident cap of $50,000. That means the third person receives nothing from your insurance.

Property damage works with a single per-accident limit, so a crash that damages two vehicles splits your $15,000 limit between them.

Why Most Idaho Drivers Stay Underprotected

Most Idaho drivers stay at minimums because they don’t understand these limits are split, not separate pools of money for each incident. Moving to $100,000 per person and $300,000 per accident costs roughly $12 to $18 monthly but protects you when crashes involve multiple people or expensive vehicles. This modest increase in premium transforms your financial exposure from catastrophic to manageable.

Real Costs Show Why Minimums Fail

A 2024 analysis by the National Safety Council found that the average hospital stay for a serious car accident injury costs $35,000 to $50,000 before any long-term care or lost wages. If you injure someone earning $75,000 annually and they miss six months of work, you owe $37,500 in lost wages alone. Add medical bills, pain and suffering settlements, and legal fees, and you’re easily at $100,000 to $150,000-far beyond Idaho’s $25,000 minimum. Luxury vehicles involved in accidents push property damage claims past $50,000 quickly.

Umbrella Coverage Fills the Gap

Umbrella coverage sits above your auto liability limits and activates when your primary policy maxes out, protecting your home equity and retirement accounts from judgment claims. You can purchase umbrella policies starting at $1 million for drivers with significant assets, and they typically cost only $100 to $200 annually. Without this layer, a serious accident judgment forces asset liquidation or wage garnishment for years. The combination of higher auto liability limits plus umbrella protection creates a financial fortress that minimum coverage simply cannot provide.

Understanding your actual exposure to liability claims reveals why so many Idaho drivers face devastating consequences after serious accidents. The next section examines the specific types of liability coverage available and how each one protects different aspects of your financial security.

Where Idaho Drivers Go Wrong with Liability Coverage

Most Idaho drivers lock in minimum coverage at age 25 and never revisit it for the next 30 years. Life changes dramatically-you buy a home worth $350,000, your income doubles, you marry and have children-but your liability limits stay frozen. This pattern repeats constantly, and it creates a financial disaster waiting to happen. The problem isn’t that drivers are careless; it’s that they don’t understand what happens when a judgment exceeds their coverage. Idaho courts don’t care about your policy limits. If you owe $200,000 and your insurance pays $50,000, creditors pursue the remaining $150,000 through wage garnishment, asset seizure, and liens against your home. A single accident can trigger 10 years of financial hardship because you saved $15 monthly by staying at minimums.

The Mistake of Treating Liability as Optional

Drivers often assume they need collision and comprehensive for their own vehicle but skip higher liability limits because they don’t see direct benefit to themselves. This backward thinking costs Idaho drivers hundreds of thousands annually. If you own a home, have retirement savings, or earn a decent income, your liability exposure far exceeds the state minimum. A crash involving a family in a newer luxury SUV-common on Idaho roads-generates medical bills, vehicle damage, and pain-and-suffering claims that routinely hit $150,000 to $300,000. Your $50,000 auto policy limit covers only a fraction of that total.

Ignoring Life Changes That Increase Your Risk

The third critical mistake happens after major life changes. You get married, purchase property, start a business, or receive an inheritance, but you never adjust your liability coverage to match your new financial situation. Many Idaho drivers carry minimum limits while protecting $400,000 in home equity-an obvious mismatch. Life changes should trigger an automatic coverage review. Getting married, buying a home, starting a business, or significant income increases all require reassessing your liability exposure. Most people spend more time planning a vacation than reviewing insurance that protects everything they own.

How to Fix Your Coverage Today

The solution is straightforward: schedule an annual policy review, not as a chore but as essential financial maintenance. Increasing to $100,000 per person and $300,000 per accident costs roughly $12 to $20 monthly-less than a streaming subscription-yet eliminates catastrophic financial risk. Adding umbrella coverage at $1 million for $100 to $200 annually creates a financial safety net that minimum coverage cannot provide. Your liability limits should reflect what you own and earn, not what the state legally requires.

Idaho’s minimums exist as a floor, not a ceiling, and staying there while building real wealth is financial negligence disguised as prudence.

Final Thoughts

Idaho liability auto insurance protects everything you’ve worked to build, not just your legal obligation to carry coverage. A single serious accident triggers judgments that exceed your policy limits, forcing wage garnishment, asset seizure, and years of financial hardship-but moving from Idaho’s $25,000 per person minimum to $100,000 per person costs only $12 to $20 monthly. Adding umbrella coverage at $1 million for $100 to $200 annually creates a financial fortress that protects your home, retirement accounts, and future earnings.

We at Matt Anderson Insurance work with Idaho drivers every day to align their coverage with their actual financial situation rather than the legal minimum. Our licensed agents understand Idaho’s specific requirements and help you build a protection strategy that covers your home, your income, and your family’s security. We offer comprehensive personal coverage including auto, home, umbrella, and more, with bundling discounts that reduce your total cost while increasing your protection.

Start by reviewing your current policy limits today-if you’re carrying minimums, schedule a conversation with one of our agents to discuss higher liability limits and umbrella coverage options. Contact Matt Anderson Insurance to schedule your free policy review and get the coverage that matches your real financial situation, not just the legal requirement.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.