Idaho Home Insurance Claims: A Step-By-Step Guide To Filing

Home damage happens fast. When it does, knowing how to file an Idaho home insurance claim can mean the difference between a smooth recovery and months of frustration.

At Matt Anderson Insurance, we’ve helped countless Idaho homeowners navigate the claims process. This guide walks you through each step, from the moment damage occurs to getting your claim resolved.

What to Do Right After Damage Strikes

Prioritize Safety First

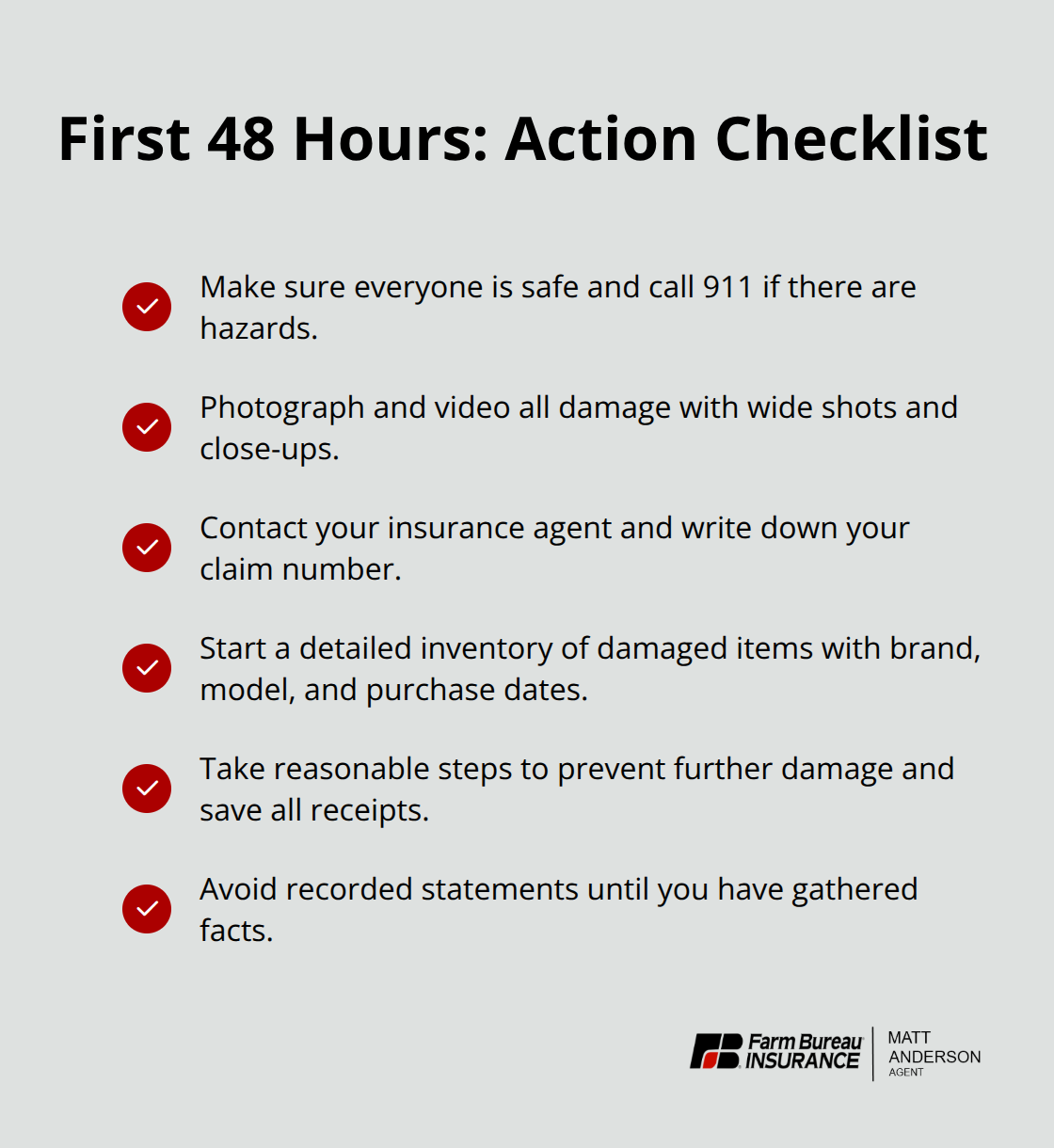

The first few hours after home damage occurs are critical. Your actions during this window directly influence how smoothly your claim moves forward and how much you’ll ultimately recover. Start by making sure everyone in your home is safe. If there’s a risk of gas leaks, downed power lines, or structural collapse, leave immediately and call 911. Once safety is confirmed, your next priority is documentation.

Document the Damage Thoroughly

Take multiple photos and videos from multiple angles of every damaged area-wide shots showing the overall scope, then close-ups of specific damage. Use your smartphone or camera in good lighting and shoot from different positions. Include the exterior of your home, interior rooms, the roof if visible, and any personal items that were damaged. The more detailed your visual record, the harder it is for an adjuster to dispute the extent of loss. If weather permits, capture images before any cleanup or temporary repairs.

Contact Your Insurance Agent Immediately

Call your insurance agent right away. Have your policy number ready and be prepared to describe what happened, when it happened, and what damage you see. Your agent will walk you through the next steps and assign a claim number-write this down and use it for all future communications. While you’re documenting, also start listing damaged items. Write down the brand, model, purchase date, and estimated value of anything that was damaged or destroyed. If you have receipts, warranty papers, or credit card statements, gather those now. Many homeowners underestimate the value of their possessions simply because they lack records.

Prevent Further Damage and Avoid Early Statements

Take reasonable steps to prevent further damage-tarp a damaged roof, board up broken windows, or stop a water leak-but don’t start major repairs or cleanup. Document what you do for mitigation and keep all receipts, as your insurer may reimburse these expenses. Avoid making recorded statements to the insurance company until you’ve had time to gather facts and think clearly about what happened.

Once you’ve completed these initial steps, your agent will guide you toward the next phase: understanding your policy coverage and preparing your formal claim submission.

Understanding Your Idaho Policy Before Filing

Review Your Coverage and Deductibles

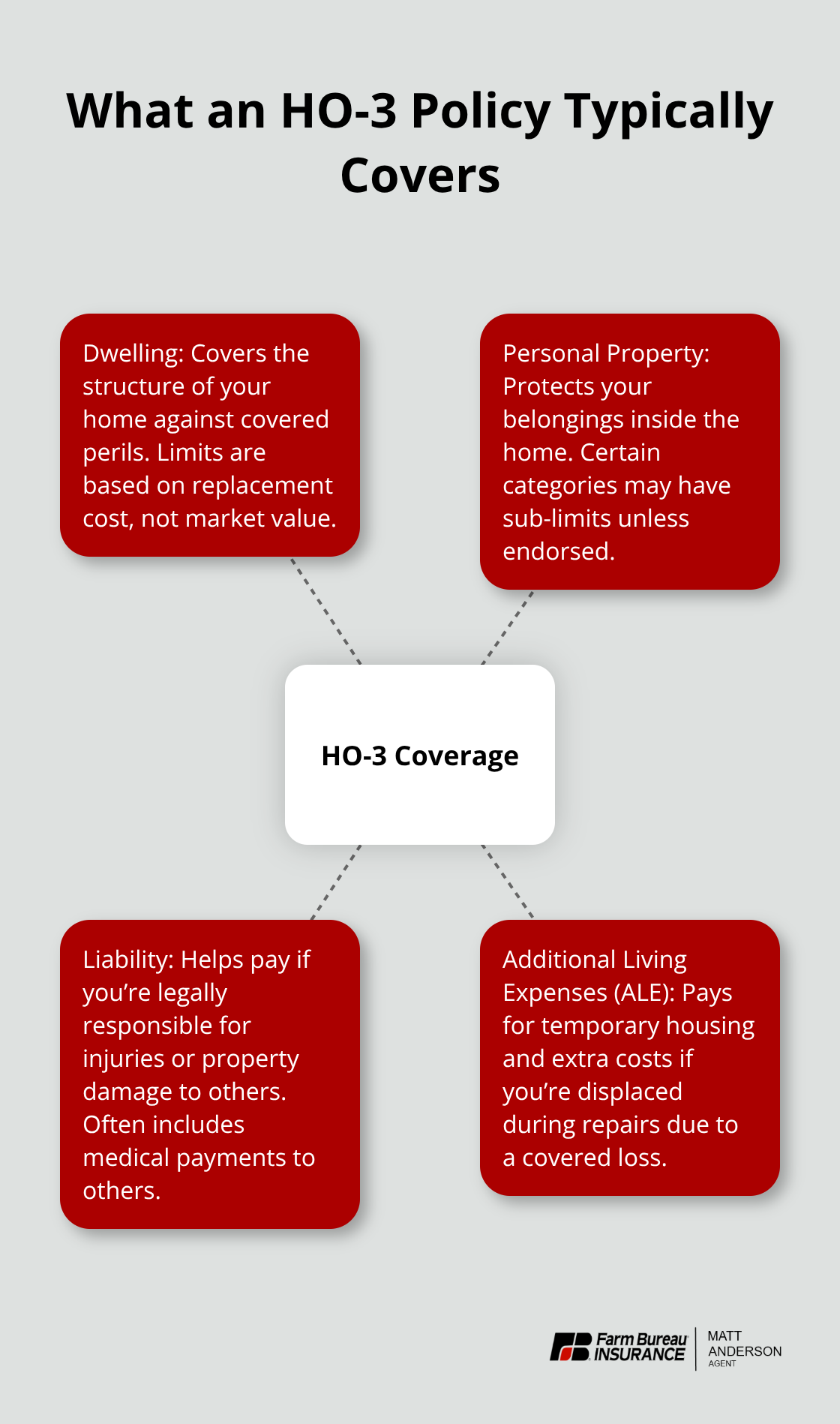

Your homeowners policy is a contract, and the fine print determines what you recover. Spend time reviewing your declarations page-the summary document that lists your coverage types, limits, and deductibles. Most Idaho homeowners carry a standard HO-3 policy, which covers the dwelling structure, personal property, liability, and additional living expenses if you’re displaced. The critical numbers are your coverage limit (the maximum the insurer will pay for dwelling damage) and your deductible (what you pay out of pocket). A common mistake occurs when homeowners assume their home’s replacement cost equals its market value.

It doesn’t. Replacement cost is what it actually costs to rebuild your home with new materials, which often runs 15 to 25 percent higher than market value in Idaho’s current construction environment.

Identify Policy Exclusions and Endorsements

Your policy also contains exclusions-damage from floods, earthquakes, and wear-and-tear are almost never covered under a standard homeowners policy. If you live in a flood-prone area or near the Yellowstone Caldera, you’ll need separate flood and earthquake policies. Review any endorsements your agent added to your policy; these are modifications that expand or restrict coverage. For example, you may have an endorsement for replacement cost on personal property, which means your insurer reimburses what it costs to replace an item new, not what it’s worth after depreciation.

Gather Required Documentation

Once you understand your coverage, gather all documentation required for your claim submission. Your insurer will request a detailed inventory of damaged items, repair estimates from licensed contractors, photos of the damage, and proof of loss-a sworn statement describing what happened and the extent of damage. The Idaho Department of Insurance recommends using IRS Publication 584 to document personal property losses; this free resource walks you through calculating replacement values for household contents.

Prepare for the Adjuster Inspection

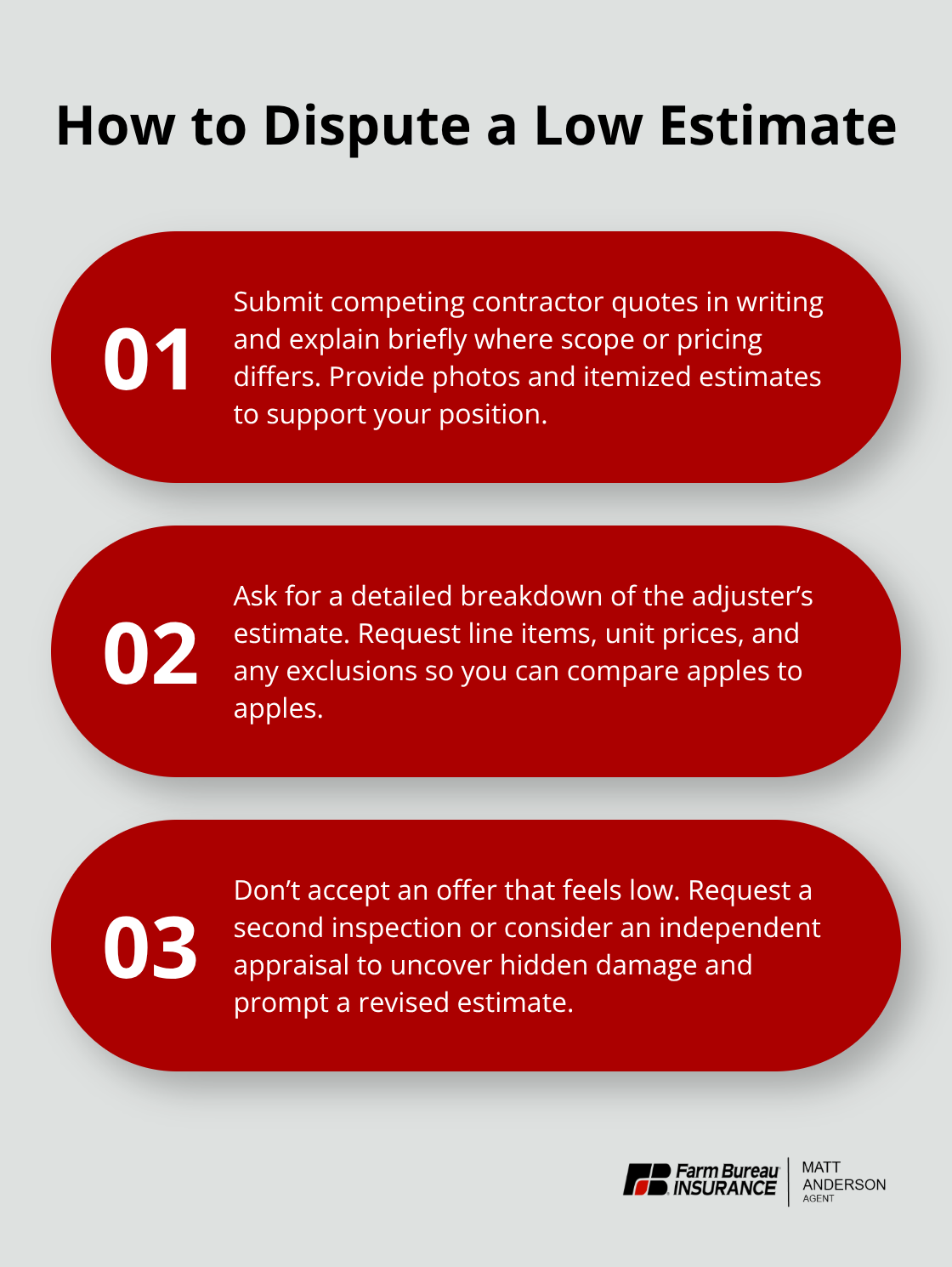

When the adjuster contacts you, they’ll verify the information in your claim, inspect the damage in person, and prepare an estimate. This is where many homeowners encounter friction. Adjusters work for the insurance company, not for you, and their priority is controlling costs. If the adjuster’s estimate seems low compared to contractor quotes you’ve obtained, provide those quotes in writing and ask for a detailed explanation of any discrepancies. Don’t accept the first settlement offer if you believe it’s unfair. Request a second inspection or hire an independent appraiser to review the damage assessment. The cost of an independent appraisal typically ranges from 300 to 800 dollars, but it often uncovers hidden damage-water intrusion, structural issues, or mold-that the initial adjuster missed. Keep all communications in writing via email, and log the dates, names, and details of phone conversations. This paper trail protects you if a dispute arises later.

With your policy reviewed and documentation in hand, you’re ready to submit your formal claim and work with the adjuster to establish the scope of repairs needed.

How to Speed Up Your Claim Settlement

Organize Your Documentation Immediately

Once your adjuster inspects the damage and provides an initial estimate, the resolution phase begins. Organization becomes your competitive advantage at this point. Create a dedicated file-physical or digital-containing every piece of documentation related to your claim. Include the adjuster’s inspection report, all contractor estimates you obtained, photos organized by room or damage type, receipts for mitigation work, your detailed inventory of damaged items with purchase dates and values, and copies of every email or written communication with your insurance company. Use a spreadsheet to track dates, claim numbers, adjuster names, and the substance of each conversation. The Idaho Department of Insurance reports that organized, complete documentation settle faster than those submitted piecemeal.

Submit Information Quickly and Completely

Insurance companies process thousands of claims annually, and yours moves faster when the adjuster doesn’t need to chase missing information. When you respond to adjuster requests, include a cover email summarizing what you’re submitting and reference your claim number on every document. Try to respond to adjuster requests within 48 hours whenever possible. Insurance companies set internal deadlines for claim closure, and delays on your end extend the entire timeline. If the adjuster requests items you don’t have, communicate in writing that you cannot provide them and explain why-don’t go silent.

Challenge Low Estimates with Evidence

If you disagree with the adjuster’s estimate, submit your own contractor quotes in writing with a brief explanation of why you believe the scope of repairs differs. Many adjusters underestimate hidden damage like water intrusion or structural issues that only surface during actual repairs. Ask the adjuster for a detailed breakdown of how they calculated the repair costs and what specific items or areas they excluded.

Don’t accept a settlement offer immediately if it feels low.

File an Appeal if the Offer Is Unfair

If you believe the offer is unfair after reviewing the adjuster’s reasoning, file a formal appeal with your insurance company. Most carriers allow a second inspection or independent appraisal at minimal cost. If your insurer denies coverage entirely or refuses to budge on a significantly low offer, contact the Idaho Department of Insurance Consumer Affairs team at 208-334-4250. They cannot force settlement, but they investigate whether the insurer violated Idaho Insurance Code provisions or acted in bad faith.

Final Thoughts

Filing Idaho home insurance claims works best when you act fast after damage strikes, document everything thoroughly, and stay organized throughout the process. Contact your insurance agent immediately with your policy number ready, review your coverage limits and deductible, and submit a complete inventory of damaged items with purchase dates, contractor estimates, and supporting receipts. Respond to adjuster requests within 48 hours when possible, challenge any low estimates with your own quotes in writing, and file a formal appeal if the settlement offer seems unfair.

We at Matt Anderson Insurance understand that navigating Idaho home insurance claims can feel stressful and complicated. Our licensed agents guide you through every step, from the initial damage assessment to final settlement, and help you understand what your policy covers and advocate for fair treatment from the insurance company. We also work with you to identify coverage gaps and recommend adjustments that better protect your home against future losses.

Your next step is simple: review your current homeowners policy and contact us if you have questions about your coverage or deductibles. Visit Matt Anderson Insurance to speak with an agent about your specific needs and get a quote today.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.