Idaho Builder Insurance: Protecting Your Projects And Profits

Construction projects in Idaho face real financial risks. Weather damage, theft, and accidents can wipe out profits faster than you’d expect.

That’s where Idaho builder insurance comes in. We at Matt Anderson Insurance know that standard business policies leave contractors exposed to gaps that can cost thousands when something goes wrong.

What Builder’s Risk Insurance Actually Covers

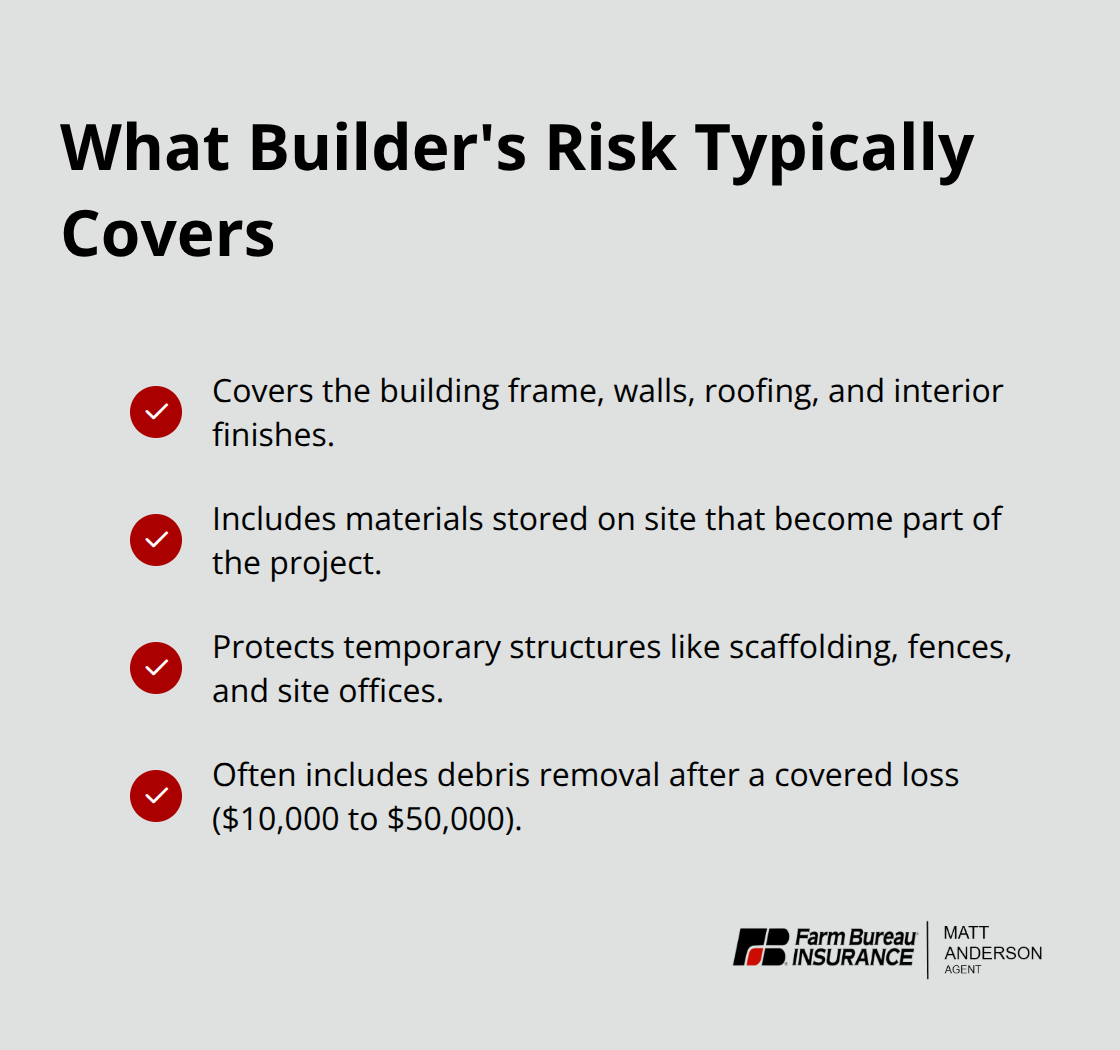

Builder’s risk insurance protects the physical structure, materials, and temporary installations on your job site from fire, hail, theft, and vandalism. The policy covers the building frame, walls, roofing, interior finishes, and materials stored on site-essentially everything that becomes part of the finished project. It also covers temporary structures like scaffolding, fences, and site offices that support construction operations. Many policies include debris removal costs if a covered loss occurs, which can run $10,000 to $50,000 on larger projects.

What Builder’s Risk Does Not Cover

The coverage typically ends when construction is complete, so you’ll need separate business property insurance afterward to protect the finished building. Builder’s risk does not cover your personal tools, equipment, or vehicles on site-those require separate inland marine or equipment coverage. The policy also excludes land itself, vegetation, and damage caused by poor workmanship or ordinary wear and tear, so understanding these boundaries prevents costly surprises when you file a claim.

Liability Coverage During Construction

Builder’s risk policies can include liability protection for bodily injury and property damage claims that arise from your construction work, though this varies by policy and endorsement. If someone is injured on your job site or your work damages a client’s existing property, liability coverage pays medical expenses, legal defense costs, and settlement amounts. Importantly, most contractors also carry a separate general liability policy that covers these same risks, and many clients require proof of at least $1,000,000 per occurrence before awarding contracts.

Defense Costs and Policy Coordination

The Hartford and other major carriers offer policies with defense costs paid outside the coverage limits, meaning your $1,000,000 limit stays intact while the insurer pays legal fees. If you work on residential projects over $2,000, Idaho law requires you to disclose your insurance details to the homeowner in writing, so having clear documentation of your liability coverage protects both you and the client. Coordinating builder’s risk liability with your general liability policy prevents gaps and overlaps that can complicate claims or leave you underinsured on high-value projects. Understanding these coverage layers helps you select the right protection before your next bid.

Why Idaho Contractors Really Need Builder’s Risk

Idaho construction sites operate in a high-risk environment that standard business policies simply don’t address. A single hailstorm damages roofing materials worth $20,000 to $100,000, and theft from job sites costs Idaho contractors thousands annually. Weather patterns in Idaho-including spring hail, winter snow loads, and summer wind events-create specific exposures that generic commercial policies exclude or severely limit. If you rely on a standard business property policy to cover materials and structures under construction, you’re almost certainly underinsured. These policies are designed for completed buildings and established operations, not for the dynamic, exposed conditions of active construction. The gap between what you think you’re covered for and what actually pays out destroys a project’s profitability in weeks.

Coverage Gaps That Cost You Money

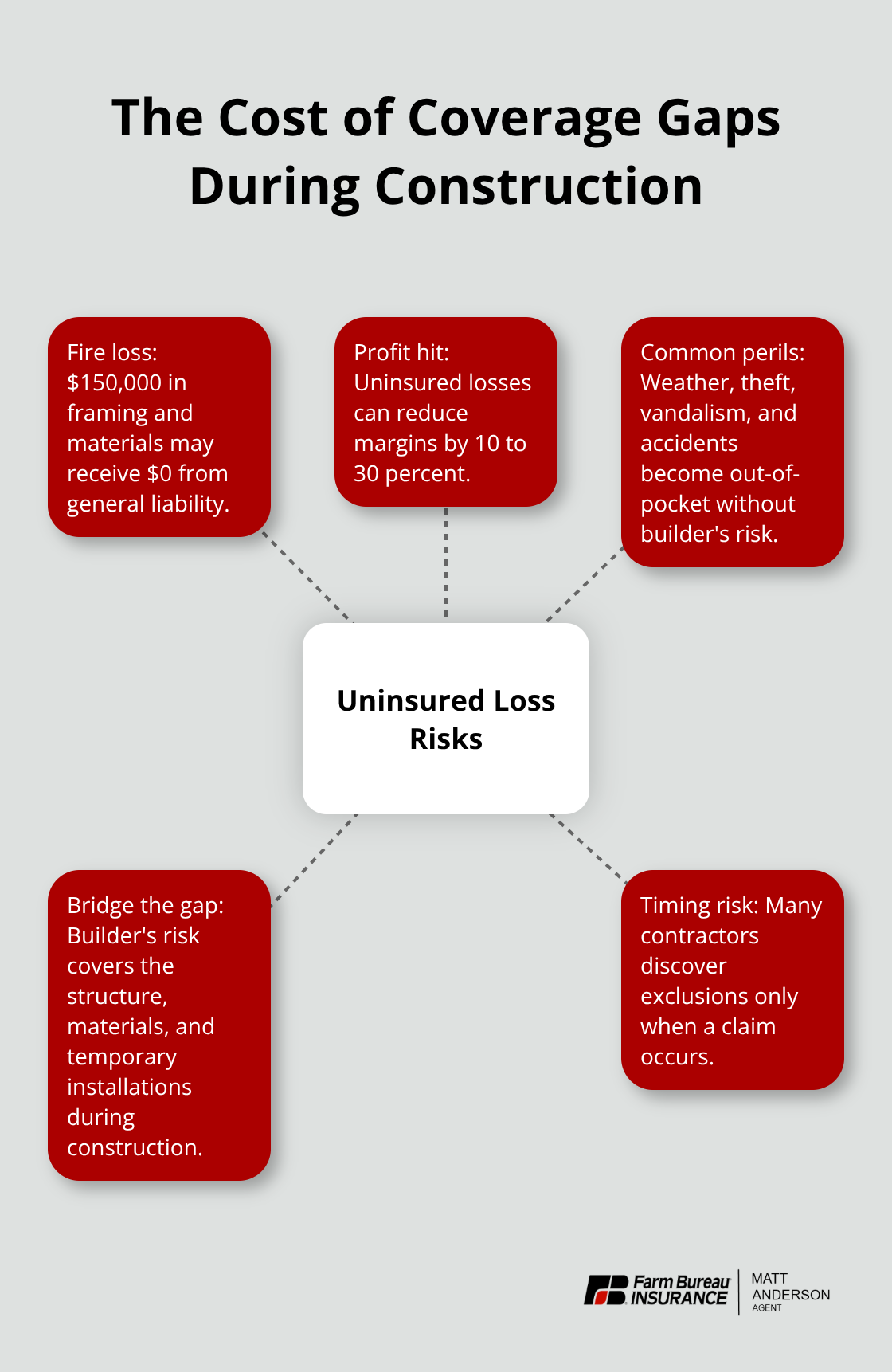

Most general contractors carry general liability insurance to meet Idaho’s registration requirements and client demands, but that policy covers only bodily injury and property damage claims-not physical loss to the building itself. If a fire damages $150,000 worth of framing and materials on your job site, your general liability policy pays nothing. That loss comes directly out of your pocket, reducing profit margins by 10 to 30 percent depending on project size. Builder’s risk fills that exact gap by covering the structure, materials, and temporary installations while construction is underway.

Without it, weather damage, theft, vandalism, and accidents become uninsured losses that force you to absorb costs or negotiate with clients to cover repairs. Contractors who thought their existing policies were sufficient often discover critical exclusions only when a claim happens-and by then it’s too late to add coverage.

Protecting Your Cash Flow and Schedule

Construction projects operate on tight timelines and tight budgets. A theft of copper wiring or HVAC equipment sets your schedule back two weeks and costs $5,000 to $15,000 in replacement and labor. Builder’s risk insurance covers these losses directly, so you file a claim and move forward rather than scrambling to fund repairs from operating capital. Debris removal endorsements, which many builder’s risk policies include, cover the cost of clearing wreckage after a covered loss-expenses that reach $10,000 to $50,000 on larger projects. Without this endorsement, you pay for cleanup out of pocket while your crew sits idle and your schedule slips further. The policy also protects your financial stake in materials ordered in advance or stored on site, so if a delivery is damaged before installation, you recover the cost rather than absorbing it as a loss.

Meeting Client Requirements and Legal Obligations

For residential projects over $2,000, Idaho law requires you to disclose your insurance to homeowners in writing anyway, so having robust builder’s risk coverage demonstrates professionalism and protects the client relationship when unexpected damage occurs. Many clients now demand proof of builder’s risk coverage before awarding contracts, especially on larger residential and commercial projects. This coverage requirement has become standard in the industry because clients understand that uninsured losses often lead to disputes, delays, and cost overruns. When you present a complete insurance package-including builder’s risk-you position yourself as a professional operator who takes project protection seriously. This advantage matters when competing for bids against contractors who carry only the state minimum coverage.

How to Match Coverage to Your Actual Project Risk

Builder’s risk policies are not one-size-fits-all, and selecting the wrong coverage limits or missing critical endorsements can leave you exposed to exactly the losses you’re trying to prevent. Start by calculating your total project value, including materials, labor, and soft costs like permits and design fees. A $200,000 residential renovation needs different coverage than a $2 million commercial build, and your policy limits should reflect the actual replacement cost of everything on site at any given time.

Calculate Your Coverage Needs Accurately

Most Idaho contractors underestimate their coverage needs because they focus only on materials and miss the cost of temporary structures, stored equipment, and debris removal. The Hartford and Travelers both offer replacement-cost valuation rather than actual cash value, which means you recover the full cost to rebuild rather than a depreciated amount-this matters significantly on projects with older materials or long timelines. Request quotes from at least three insurers and compare not just the premium but also what’s included in the base policy versus what requires paid endorsements. A policy that includes $100,000 in debris removal coverage as standard saves you thousands compared to one that requires you to purchase this protection separately.

Choose Your Deductible Based on Cash Reserves

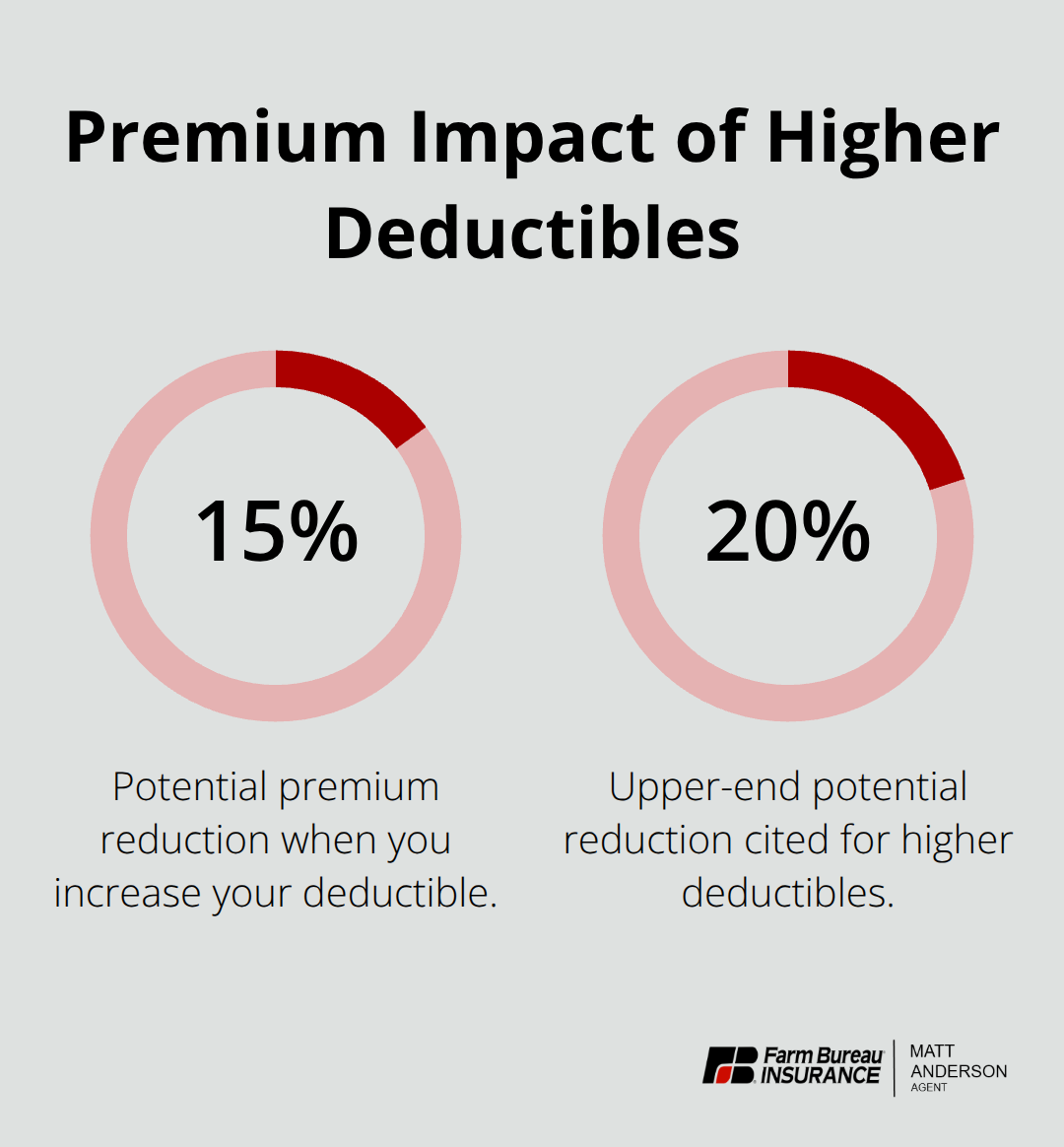

Deductibles typically range from $1,000 to $5,000, and choosing a higher deductible can reduce your annual premium by 15 to 20 percent, but only if you can afford to pay that amount out of pocket when a loss occurs. Calculate your deductible choice based on your operating capital and cash reserves-a contractor with limited liquid assets should choose a $1,000 deductible even if it costs more annually, because a $5,000 out-of-pocket loss could strain your business.

This decision directly affects both your premium and your financial stability after a claim.

Work with a Local Idaho Agent

Idaho’s specific weather patterns and regional construction practices require an agent who understands local risks rather than someone selling a generic national template. Work with a local Idaho-based agency that knows spring hail patterns, winter snow load requirements, and the building codes that affect your projects. Ask your agent directly whether they recommend endorsements for pollutant cleanup, code-change penalties, or energy-efficiency certification costs-these add $500 to $2,000 annually but prevent catastrophic gaps when a covered loss triggers these expenses.

Verify Policy Details Before Committing

Verify whether your policy’s defense costs are paid outside your coverage limits or count toward them; Chubb and The Hartford typically pay defense costs separately, which preserves your limit for actual claim payouts. Request a sample policy document before committing and have your attorney review it if the project value exceeds $500,000. When construction finishes, coordinate with your agent to transition from builder’s risk to business property insurance for the completed building, because builder’s risk automatically expires and leaves you uninsured if you don’t arrange follow-up coverage immediately. Document your project timeline clearly when applying for quotes, because policies are priced and underwritten based on the construction schedule you provide-extensions beyond the original timeline may require policy amendments or new quotes.

Final Thoughts

Idaho builder insurance protects your profits from weather damage, theft, and accidents that standard business policies ignore. A single hailstorm destroys $50,000 in roofing materials, theft of copper wiring delays your schedule by weeks, or vandalism forces you to replace windows and doors-these losses hit your bottom line hard without proper protection. Builder’s risk covers the physical structure, materials, and temporary installations on your job site while your general liability policy handles bodily injury and property damage claims, creating a complete safety net for your projects.

Selecting the right coverage means calculating your actual project value, choosing deductibles based on your cash reserves, and working with a local agent who understands Idaho’s specific weather risks and building practices. The cost typically ranges from 1 to 5 percent of your total project budget-a small investment compared to the financial damage an uninsured loss causes. When you combine builder’s risk with your general liability policy and meet Idaho’s registration requirements, you present yourself as a contractor who takes project protection seriously.

Contact Matt Anderson Insurance today for a quote on Idaho builder insurance that matches your actual exposure. Our licensed agents help contractors select coverage that protects both projects and profits. We handle claims support efficiently so you keep your schedule on track.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.