Idaho Business Auto Coverage: Tailored Protection For Your Company Vehicles

Running a business in Idaho means keeping your company vehicles protected from real risks. Accidents, theft, and liability claims can drain your budget fast, which is why Idaho business auto coverage isn’t optional-it’s essential.

At Matt Anderson Insurance, we help Idaho business owners find policies that match their actual needs. Whether you operate a single vehicle or a full fleet, the right coverage protects your bottom line.

Why Your Idaho Business Needs Auto Coverage

Liability Claims Can Devastate Your Bottom Line

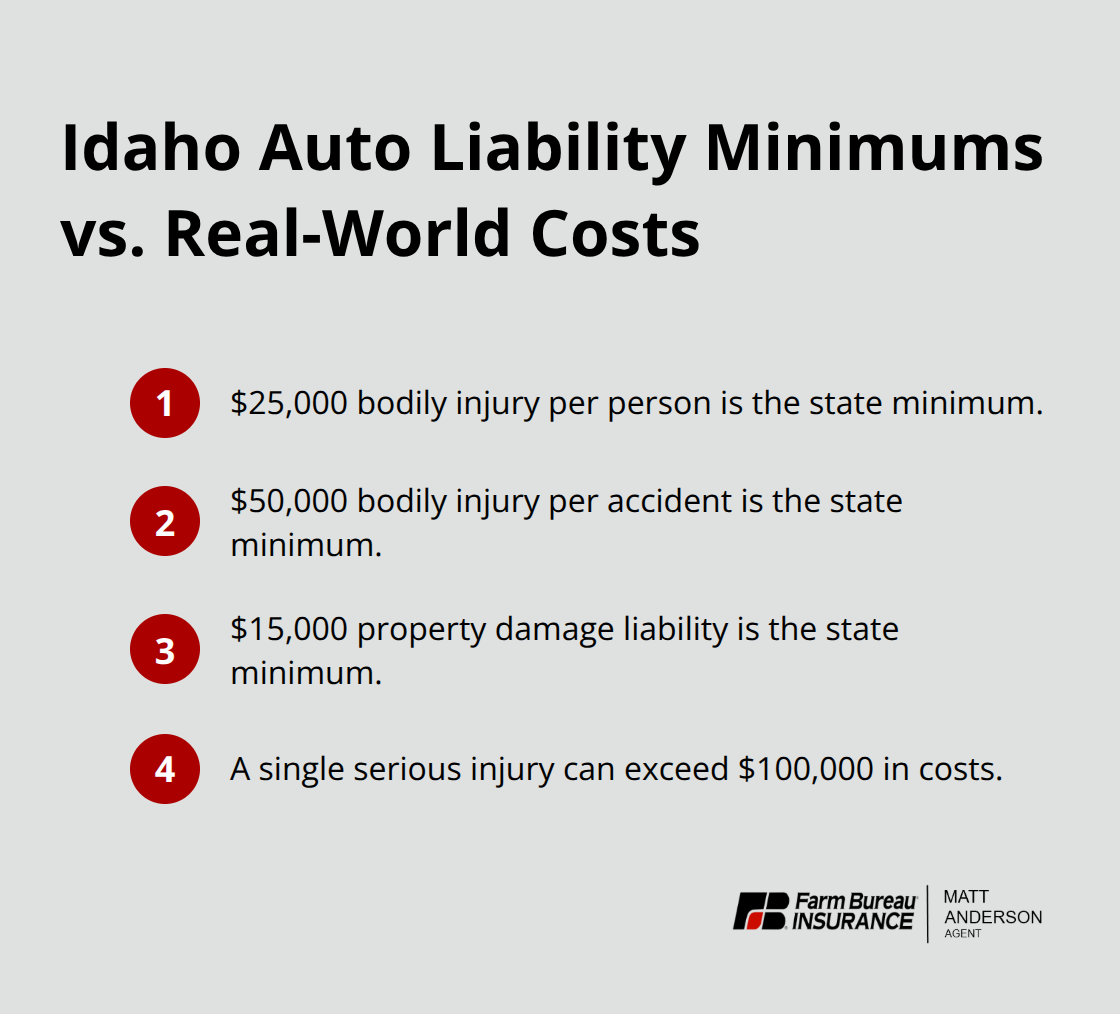

Liability claims from accidents involving your business vehicles can cost far more than you expect. When an employee or contractor driving a company vehicle causes injury or property damage, your business bears legal responsibility for those costs. Idaho law requires a minimum of $25,000 per person and $50,000 per accident in bodily injury liability coverage, plus $15,000 for property damage. However, these minimums often fall short in real accidents. A single serious injury claim can easily exceed $100,000, leaving your business vulnerable to lawsuits, wage garnishment, and operational shutdown if you lack adequate coverage.

Personal Policies Leave You Exposed

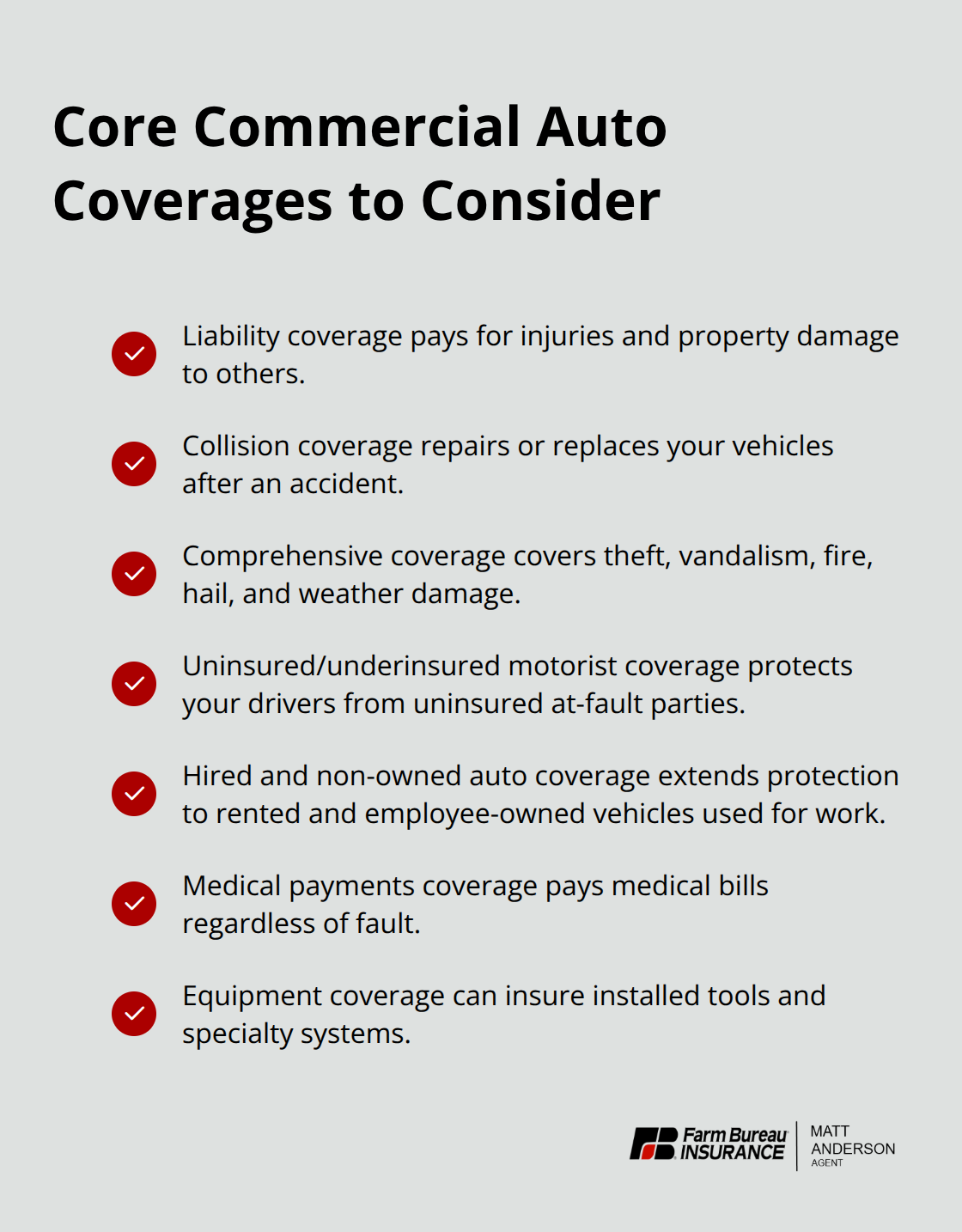

Without proper business auto insurance, a personal auto policy will deny your claim if the insurer discovers commercial use. This denial leaves you personally liable for damages. Your business vehicles face constant risk from collisions, weather damage, vandalism, and theft. Collision coverage repairs or replaces your vehicles after accidents, regardless of who caused the damage, while comprehensive coverage handles theft, fire, hail, and vandalism.

Idaho Weather and Rural Conditions Demand Protection

In Idaho, winter weather creates hazardous driving conditions and rural areas present longer response times for emergencies. Having collision and comprehensive protection means your fleet stays operational without depleting cash reserves for unexpected repairs. Commercial vehicles require coverage that personal auto policies simply do not provide. If your business uses vehicles for deliveries, client visits, or equipment transport, state law mandates commercial auto insurance rather than a personal policy.

Legal Penalties for Operating Without Coverage

Driving without proper commercial coverage exposes your business to a minimum $75 fine and potential license suspension. The investment in the right business auto policy protects your company’s assets, keeps your fleet on the road, and ensures compliance with Idaho law. Understanding what coverage options exist helps you make informed decisions about your fleet’s protection.

What Your Business Auto Policy Actually Covers

Liability Coverage Protects Your Business from Claims

Idaho business auto policies protect your company against three categories of financial risk that personal policies ignore. Liability coverage pays for injuries or property damage your business causes to others-this is non-negotiable because Idaho law requires minimum property damage liability coverage of $15,000. However, real accidents often exceed these minimums significantly. A serious injury claim can reach $100,000 or more, which is why you should evaluate higher limits based on your fleet size and vehicle types.

Collision and Comprehensive Coverage Keeps Your Fleet Running

Collision and comprehensive coverage protect your vehicles themselves. Collision pays to repair or replace your company vehicles after accidents regardless of fault, while comprehensive coverage covers theft, vandalism, hail, fire, and weather damage-critical protections in Idaho’s harsh winter conditions and rural areas where response times are longer. If you operate box trucks or utility vans for service work, collision and comprehensive coverage prevent a single hail storm or theft from grounding your fleet for weeks.

Uninsured and Underinsured Motorist Coverage Fills a Dangerous Gap

Uninsured and underinsured motorist coverage protects your drivers and employees when they’re hit by drivers who cannot pay their own liability claims. This coverage is particularly important because Idaho requires insurers to offer it unless you sign a written rejection, yet many businesses skip it to save money. This protection matters more than most Idaho business owners realize.

Additional Coverages Address Specific Business Needs

If your employees drive personal vehicles for business tasks like client visits or deliveries, you need hired and non-owned auto coverage added to your policy-this endorsement typically costs under $200 annually but covers accidents involving rented or employee-owned vehicles used for work. Medical payments coverage pays for medical expenses for your drivers and passengers after an accident, eliminating out-of-pocket costs regardless of fault. For specialized vehicles like food trucks with installed equipment or dump trucks with hydraulic systems, standard collision coverage may not fully replace expensive equipment, so discuss equipment coverage limits with your agent before an accident happens.

Understanding Your Premium and Coverage Fit

The average commercial auto insurance cost in Idaho runs about $204 per month or $2,449 annually according to industry data, though your specific premium depends on vehicle type, location, driving records, and how many miles your fleet covers annually. A contractor operating one pickup truck in Boise faces different risk than a delivery service running five vehicles across rural North Idaho, so your coverage should match your actual exposure rather than following a generic template. The right policy structure depends on what your business actually does and where your vehicles operate.

Matching Your Coverage to Your Actual Business

Inventory Your Fleet and Operations Honestly

Start with a brutally honest inventory of what your business actually operates. If you run a single pickup truck for occasional client visits, your coverage needs differ dramatically from a contractor managing five vehicles across multiple job sites or a delivery service covering hundreds of miles weekly. The vehicle types matter enormously-a box truck carrying equipment faces different risks than a passenger van, and a dump truck with hydraulic systems requires different protection than a standard sedan. Document how many vehicles you own or lease, what each one does, and whether employees drive them. This assessment directly determines your premium and reveals protection gaps. Location within Idaho also shifts your risk profile significantly. A Boise-based contractor operating within city limits faces different hazards than a business covering rural North Idaho from Coeur d’Alene to Sandpoint, where longer distances between service areas and harsher winter conditions increase accident likelihood and response times.

Calculate Mileage and Evaluate Liability Limits

Calculate your actual annual mileage and driving patterns, then evaluate whether your current liability limits match that exposure. If your fleet covers 50,000 miles annually across multiple drivers on varied terrain, Idaho’s minimum $25,000 per person and $50,000 per accident bodily injury limits become dangerously insufficient-a single serious injury can cost $100,000 or more, leaving your business personally liable for the difference. Higher limits cost more but protect your assets from catastrophic claims. The relationship between your mileage, vehicle count, and liability exposure determines whether minimums suffice or whether you need substantially higher protection.

Choose Deductibles That Match Your Financial Position

Review your deductible options carefully: a $500 deductible lowers your monthly premium but means higher out-of-pocket costs after each accident, while a $1,000 or $2,500 deductible increases monthly costs but works better if your business has minimal accident history and can absorb larger repair expenses. Consider collision and comprehensive deductibles separately-you might choose a higher deductible for comprehensive coverage since weather and theft claims occur less frequently than collision incidents. Your cash flow situation and claims history should guide this decision rather than simply selecting the lowest premium option.

Explore Bundling and Coverage Combinations

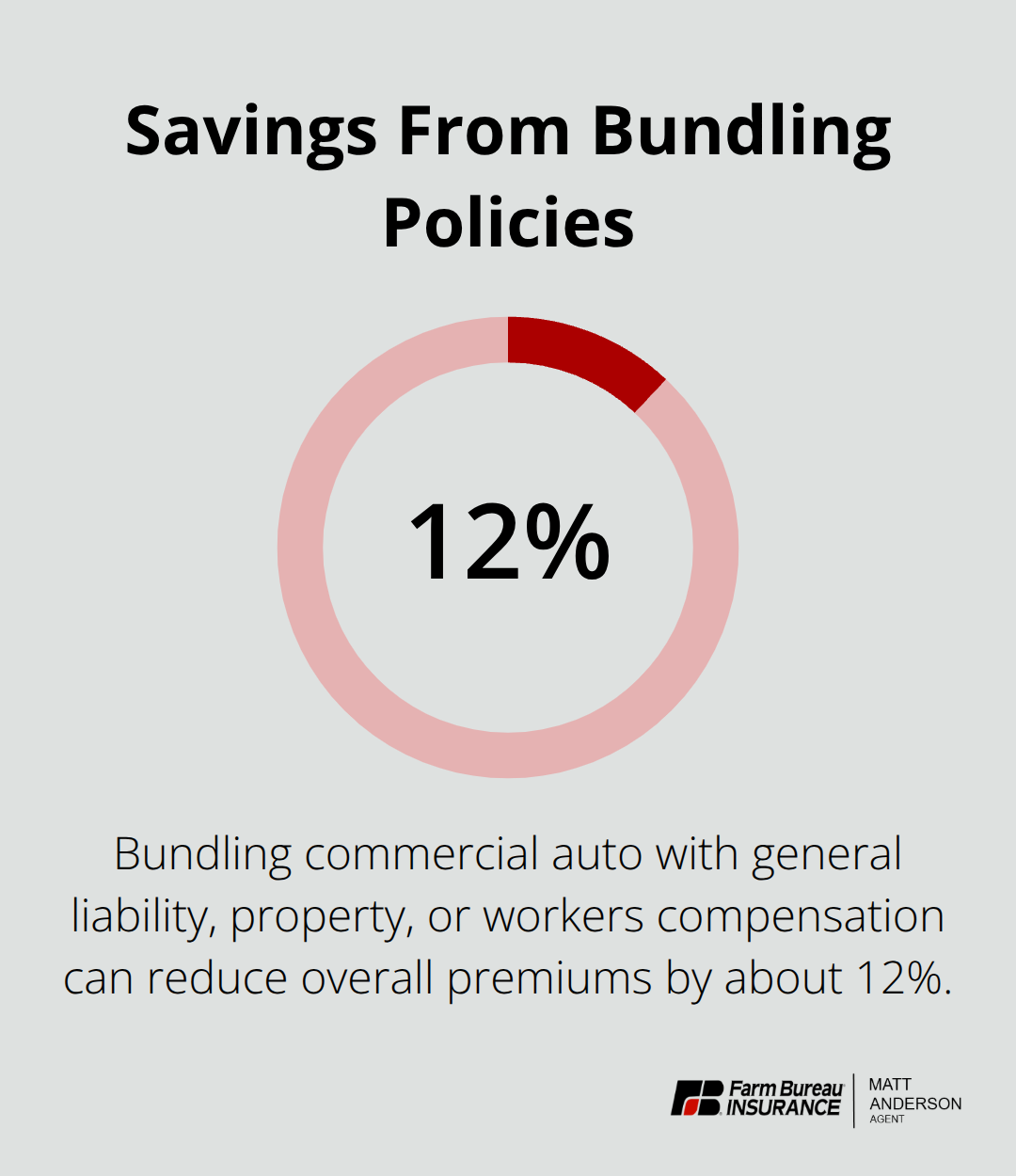

Bundling your commercial auto policy with general liability, property coverage, or workers compensation reduces your overall premium by approximately 12 percent according to industry data, making a comprehensive quote from a local agent essential before deciding. This approach simplifies your coverage structure and often delivers meaningful savings that offset the cost of higher liability limits or lower deductibles. A local independent agent can compare options across multiple carriers to identify the combination that protects your fleet while fitting your budget.

Final Thoughts

Idaho business auto coverage protects your company from liability claims, vehicle damage, and legal penalties that threaten your operations. The right policy structure reflects your actual fleet size, vehicle types, annual mileage, and where you operate across Idaho-not a generic template that ignores your specific risks. Minimum liability limits of $25,000 per person and $50,000 per accident often fall short when serious injuries occur, so higher coverage limits represent a practical investment that safeguards your assets.

At Matt Anderson Insurance, we match your coverage to real operational needs rather than forcing one-size-fits-all solutions onto your business. Our licensed agents understand how a Boise-based contractor’s risks differ from a North Idaho delivery service, and we structure policies that reflect those differences. We offer bundling discounts when you combine commercial auto with general liability, property, or other business coverages, typically reducing your overall premium by around 12 percent.

Contact Matt Anderson Insurance today to discuss your specific vehicles, operations, and coverage needs. Our agents will compare options across carriers to find protection that fits your budget while safeguarding your company’s assets. Visit mattandersoninsurance.com to request a quote and take the first step toward comprehensive protection for your business vehicles.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.