Idaho Farm Bureau Homeowners: A Community-Backed Policy Choice

Homeowners across Idaho are discovering that Farm Bureau policies offer real value through local support and competitive rates. At Matt Anderson Insurance, we’ve seen firsthand how Idaho Farm Bureau homeowners benefit from personalized service and strong financial backing when claims happen.

This guide walks you through why Farm Bureau stands out for Idaho families, what coverage options protect your home, and how their approach compares to larger national insurers.

Why Idaho Families Trust Farm Bureau

Local Agents Who Know Idaho Risks

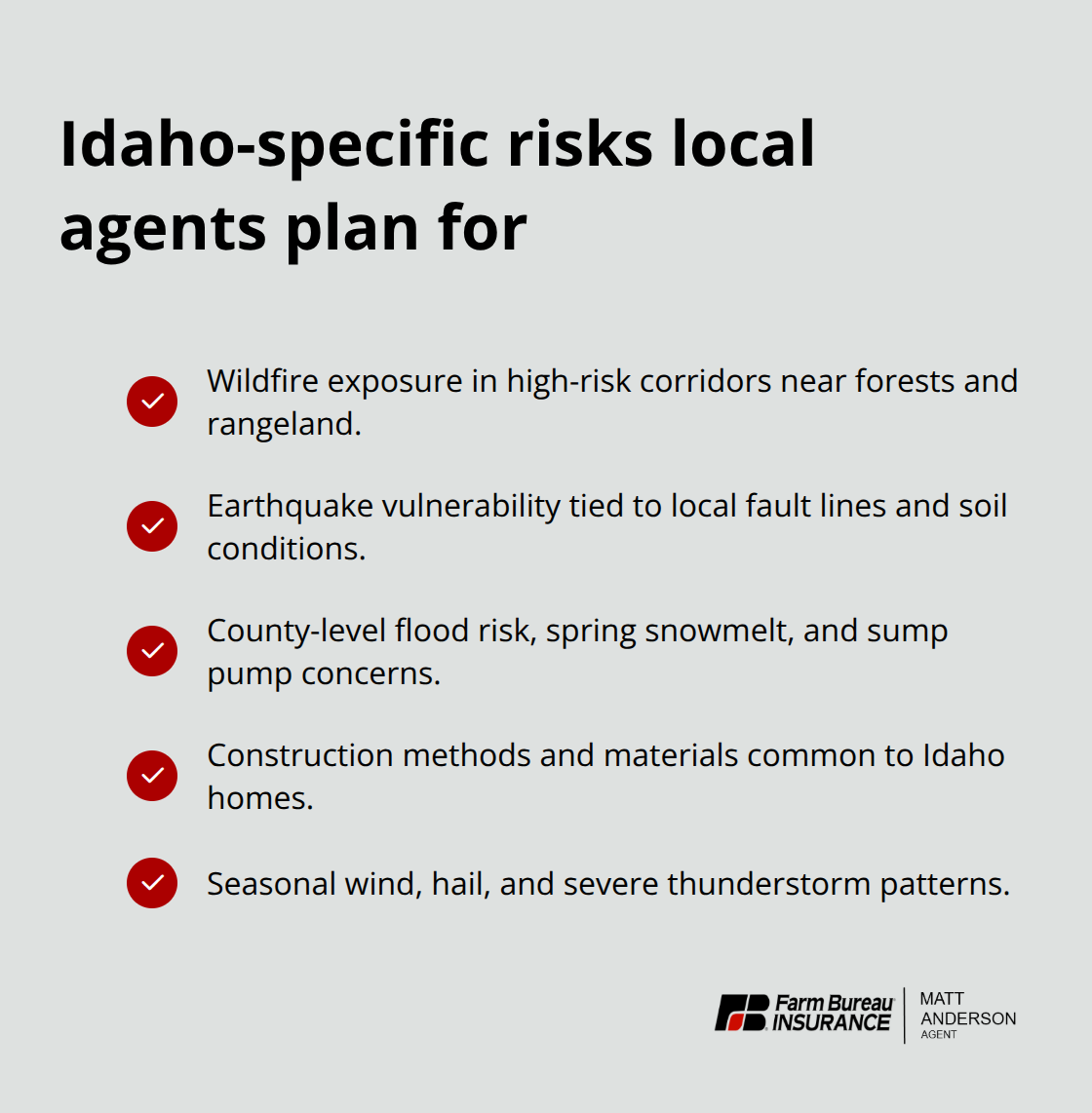

Idaho homeowners need agents who understand local hazards-wildfire exposure, earthquake vulnerability, and flood risk in specific counties. Farm Bureau delivers that expertise. Their agents know Idaho properties inside and out, which means when you call with a claim or coverage question, you talk to someone familiar with how homes in your area are actually built and what threats they face. That local knowledge saves time and prevents coverage gaps that national call centers often miss.

Financial Stability Backs Real Claims Support

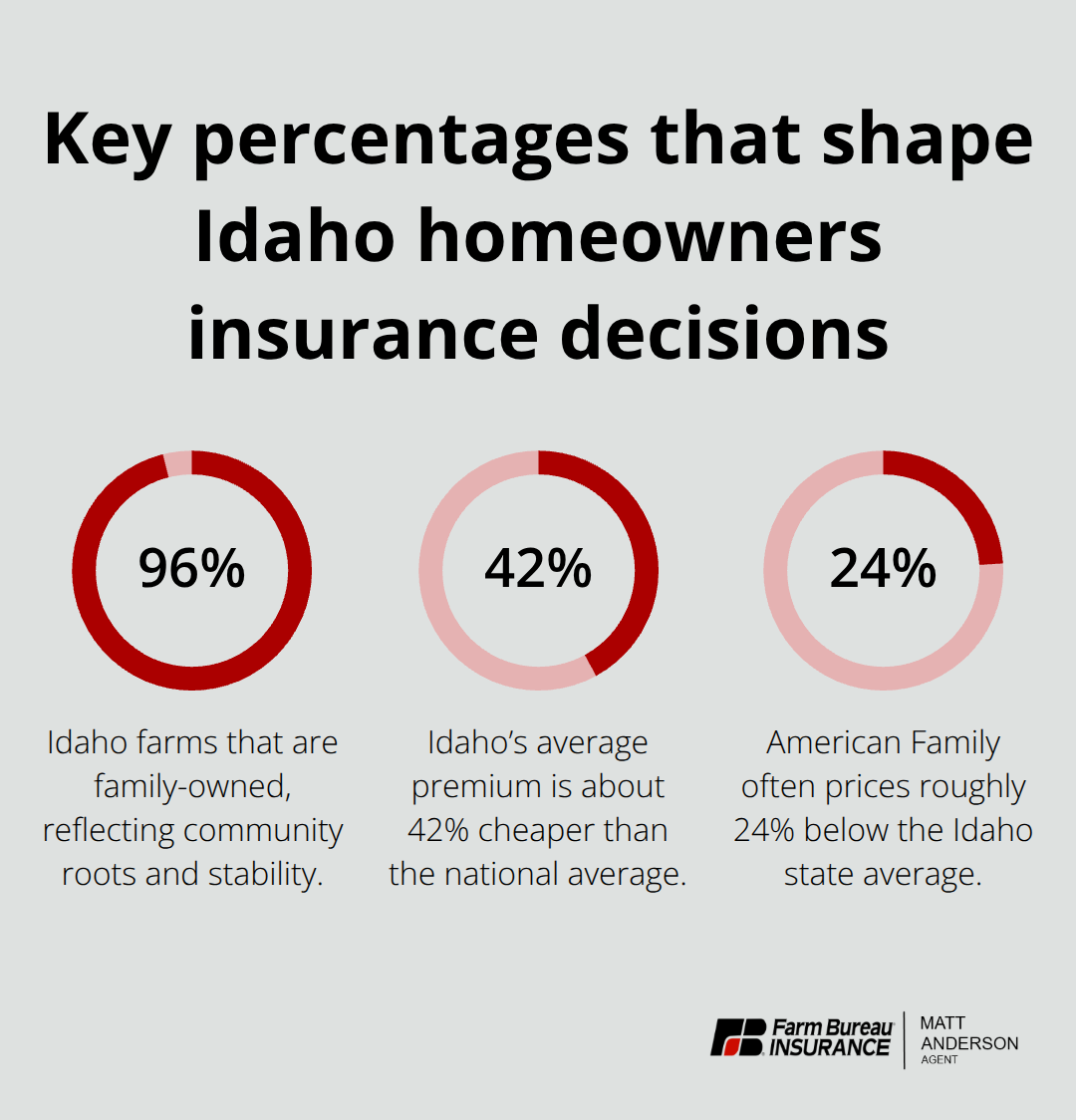

The financial numbers matter. About 96 percent of Idaho farms are family-owned, and that community focus extends to how Farm Bureau operates. Their financial stability supports fast, reliable claims processing when a pipe bursts or a storm damages your roof. Families count on that speed when damage happens, and Farm Bureau’s track record reflects their commitment to Idaho homeowners.

Bundling Cuts Your Overall Premium

Bundling auto, farm, or boat coverage with your home policy typically cuts your overall premium by 10 to 15 percent, depending on your insurer. We recommend getting specific quotes from Farm Bureau and comparing them side by side with national carriers, because bundling discounts vary significantly. The key is comparing identical coverage limits and deductibles across quotes. Idaho homeowners also benefit from Farm Bureau’s endorsement options tailored to state hazards.

Endorsements Address Real Idaho Threats

Water backup coverage protects against sump pump failures and heavy rain damage-a real concern in flood-prone Idaho counties. Personal articles floaters cover valuable items like jewelry or electronics separately from your standard policy limits. These endorsements address actual risks Idaho homes face, not theoretical add-ons. When you evaluate any homeowners policy, ask your agent which endorsements apply to your property’s location and what they cost. That conversation with a local agent beats generic online quotes every time.

Your coverage options matter just as much as your agent’s local knowledge. Understanding what Farm Bureau policies actually protect-and what gaps might exist-helps you make the right choice for your home.

Coverage Options That Protect Idaho Homes

How Farm Bureau Policies Cover Your Dwelling and Structures

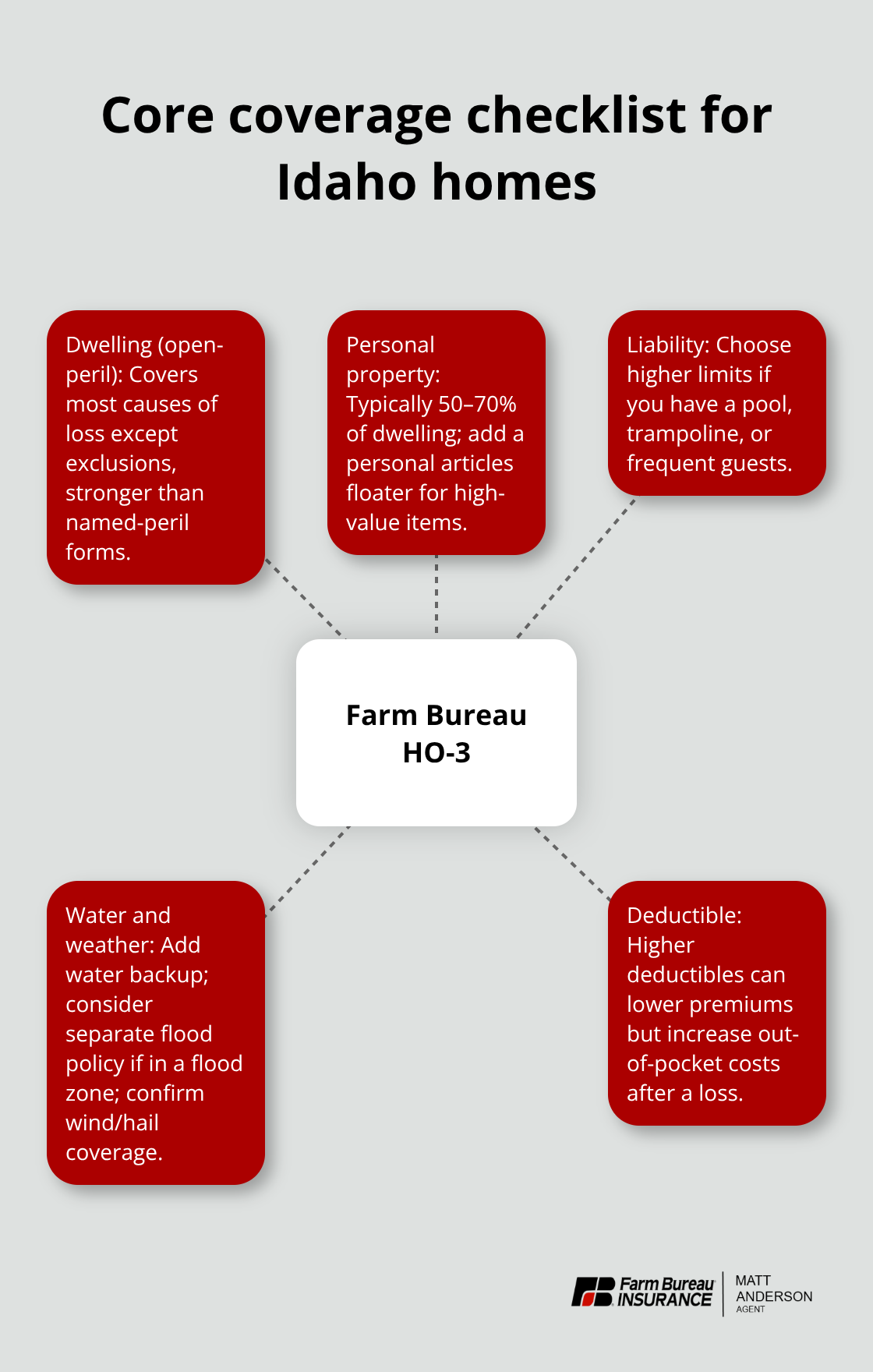

Idaho Farm Bureau homeowners policies protect your dwelling structure on an open-peril basis, which means they cover damage from most causes except those specifically excluded in your policy. That’s stronger than named-peril coverage, which only pays for damage listed in your contract. Your dwelling coverage pays to rebuild or repair the house itself, while other structures coverage handles detached garages, sheds, or fences. The standard form in Idaho is the HO-3, and it provides solid protection for the physical building you live in.

Personal Property Coverage and High-Value Items

Personal property coverage reimburses you for furniture, electronics, and clothing inside your home if theft or weather damage occurs. The standard HO-3 limits personal property to a percentage of your dwelling coverage, typically 50 to 70 percent. If you own high-value items like jewelry, cameras, or collectibles, that percentage won’t cover replacement costs. You need a personal articles floater, which costs extra but covers those items separately and often at replacement cost rather than actual cash value. Most Idaho homeowners underestimate what their belongings are worth until they need to replace everything after a fire or theft.

Liability Protection When Accidents Happen

Liability coverage protects you financially when someone is injured on your property or you accidentally damage someone else’s property. Farm Bureau policies typically include liability coverage that pays legal costs and damages up to your limit, usually between $100,000 and $500,000 depending on what you choose. Idaho homeowners with pools, trampolines, or who frequently host guests should lean toward higher limits because injury claims add up fast.

Water Damage and Weather-Related Endorsements

Water damage coverage is essential in Idaho, where heavy spring snowmelt and summer thunderstorms cause basement flooding and sump pump failures. Standard policies exclude flood damage from natural water events, so you need either water backup coverage as an endorsement or a separate flood insurance policy through the National Flood Insurance Program if you’re in a designated flood zone. Weather-related endorsements like wind and hail coverage are sometimes separate from your base policy, so ask your agent whether your coverage includes damage from severe storms or if you need additional protection.

Choosing the Right Deductible for Your Budget

The cost difference between a $500 deductible and a $1,000 deductible typically saves you 10 to 15 percent on your annual premium, but only raise your deductible if you can actually pay that amount out of pocket after a loss without financial strain. Your deductible choice directly affects both your monthly costs and your financial readiness when damage happens. Understanding these coverage pieces helps you compare Farm Bureau policies against other Idaho insurers and spot where your protection might fall short.

How Farm Bureau Stacks Up Against National Insurers

Price Versus Local Expertise

Farm Bureau homeowners policies in Idaho cost about $2,528 annually for a $300,000 dwelling, according to Bankrate’s 2025 analysis. That price sits above the Idaho state average of roughly $1,409 per year-about 42 percent cheaper than the national average-but the difference reflects what you actually receive. National carriers like USAA, State Farm, Allstate, and Travelers operate through call centers and online systems built to process claims at scale, not to understand that your Meridian home sits in a wildfire corridor or that your Coeur d’Alene property faces seasonal flood risk. Farm Bureau agents know these specifics because they live in Idaho communities and work with local properties every day.

Customer Satisfaction and Eligibility Across Carriers

USAA ranks highest in customer satisfaction according to JD Power surveys, but eligibility requires military service or veteran status, which excludes most Idaho residents. State Farm offers strong online tools and maintains a broad local agent network across the state. American Family typically undercuts the state average by roughly 24 percent. Travelers provides green home endorsements for LEED-certified features. None of these options, however, combine local presence with Idaho-specific coverage the way Farm Bureau does, and that combination carries a cost premium that reflects actual expertise rather than processing efficiency.

Claims Handling and Regional Knowledge

The real difference emerges when you file a claim. Farm Bureau agents handle claims through people who understand Idaho property construction, local building codes, and how claims adjusters evaluate damage in your region. National insurers route claims through regional centers where adjusters may have never experienced an Idaho winter or handled properties built to withstand earthquake risk. Speed and accuracy matter when your home needs repairs, and local knowledge accelerates both.

Bundling Options and Specialized Coverage

Bundling auto, farm, or boat coverage with your home policy saves 10 to 15 percent across carriers, but Farm Bureau’s bundling options include coverage for snowmobiles, boats, and ATVs that national carriers often exclude or charge separately. This tailored approach addresses how Idaho families actually live-with recreational equipment and farm assets that standard national policies treat as afterthoughts. The bundling savings compound when you add multiple policies, making the overall premium comparison more favorable than a homeowners-only quote suggests.

Making Your Decision

The answer to whether Farm Bureau’s premium justifies the local expertise depends on your risk tolerance and whether you value having an agent who already knows your property’s specific threats versus saving money upfront with a national company that treats your claim like any other in their system.

Final Thoughts

Idaho Farm Bureau homeowners policies deliver what national carriers cannot: an agent who understands your specific property risks and a company rooted in your community. When a wildfire threatens your neighborhood or spring snowmelt floods your basement, you need someone who has handled similar claims in your exact region, not a claims processor working through a national queue. Farm Bureau’s local presence and Idaho-specific endorsements address real threats your home faces, and that expertise justifies the premium difference for families who prioritize reliability over the lowest upfront cost.

The decision ultimately hinges on what matters most to you. If you want the absolute lowest rate and don’t mind managing claims through a national call center, carriers like American Family or State Farm offer competitive pricing. If you value having an agent who knows your property’s earthquake vulnerability, flood risk, and local building standards, Idaho Farm Bureau homeowners coverage delivers that peace of mind. Most Idaho homeowners fall somewhere in between, which is why comparing actual quotes side by side matters more than relying on averages.

Contact Matt Anderson Insurance to request quotes from Idaho Farm Bureau and compare them directly with other carriers using identical coverage limits and deductibles. Ask about bundling discounts for auto, farm, or boat coverage, and request specific endorsements for water backup and personal articles if you need them. Your agent can walk you through which coverage options match your property’s actual risks rather than selling you generic add-ons.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.