Idaho Farm Home Insurance: Protecting Rural Homes And Farm Assets

Farm properties face insurance challenges that standard homeowners policies simply don’t cover. Barns, equipment, livestock, and liability from farm operations require specialized protection that we at Matt Anderson Insurance understand deeply.

Idaho farm home insurance needs to account for your unique rural setup. This guide walks you through the coverage options that actually matter for your farm.

Why Farm Properties Need Different Insurance

Standard Homeowners Policies Leave Farm Operations Unprotected

Farm homes sit on land that operates as both a residence and a business, which creates coverage gaps that standard homeowners policies won’t touch. A typical homeowners policy protects your house and personal belongings inside, but it explicitly excludes farm operations, equipment, and liability from animals or farm activities. The moment you add barns, grain storage, tractors, or livestock to your property, you’ve moved beyond what a regular policy covers. Farmers often call after a barn fire or equipment theft only to discover their homeowners policy won’t pay because farm structures and machinery fall outside standard residential coverage. Your farm isn’t just a place to live; it’s an operation with distinct risks that demand specialized protection.

Physical Differences Drive Insurance Complexity

The physical differences between farm properties and suburban homes directly impact your insurance needs. Farm buildings use different materials and construction methods than residential structures-metal roofing on barns, concrete floors in equipment storage, and open-sided sheds don’t fit the standard building classifications that insurers use for houses. Your equipment inventory changes seasonally and includes high-value items like combines, tractors, and hay balers that depreciate differently than household goods.

Farm liability exposure on rural properties is significantly higher because visitors, hired workers, and contractors move through your property regularly, and animals create injury risks that homeowners policies explicitly exclude.

Liability Costs Can Exceed Half a Million Dollars

A single incident involving a visitor injured by livestock or a neighbor’s child hurt on farm equipment can result in claims exceeding $500,000 in medical and legal costs. Farm home insurance accounts for these realities by providing separate coverage categories for structures, equipment, liability, and animals rather than lumping everything into one residential package. This specialized approach protects your operation from the ground up, addressing risks that standard policies ignore entirely.

Understanding these differences sets the stage for evaluating the specific coverage options that actually protect your farm operation.

What Your Farm Home Insurance Actually Covers

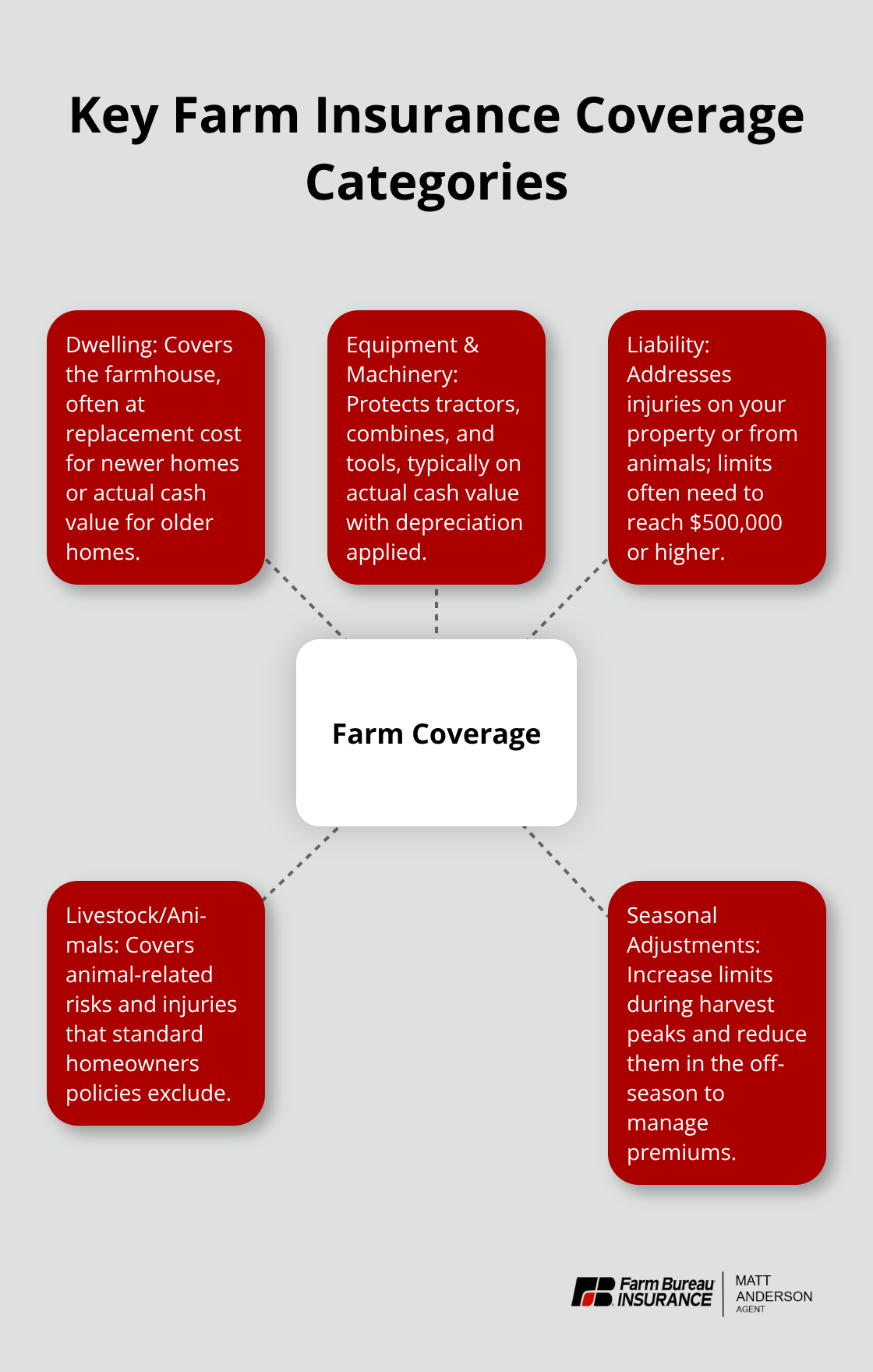

Dwelling Coverage Protects Your Main Farmhouse

Idaho farm home insurance splits protection into distinct coverage categories that work together to address your operation’s real risks. The main farmhouse receives dwelling coverage that pays to rebuild or repair the structure if fire, wind, theft, or other covered perils damage it. Dwelling coverage for your house typically starts at replacement cost for newer structures but shifts to actual cash value for homes built before the 1970s, which means you absorb depreciation on older properties. This distinction matters significantly-a farmhouse constructed in 1965 will cost less to insure under actual cash value than a newly built home, but you’ll recover less after a total loss.

Equipment and Machinery Need Accurate Inventory Values

Equipment and machinery coverage protects your tractors, combines, balers, and other farm tools-typically valued at actual cash value rather than replacement cost, which means depreciation applies. Equipment coverage requires you to provide an accurate inventory, as many farmers underestimate machinery values and end up underinsured when a combine or tractor needs replacement. Peak-season adjustments matter for grain storage and harvested crops, allowing you to increase limits during harvest months and reduce them during off-season periods, which lowers your annual premium while keeping you protected when risk is highest. Ask any potential provider specifically whether their farm policies include coverage for foreign object ingestion on equipment since rocks and debris cause expensive breakdowns, and whether they offer custom farming endorsements if you perform agricultural work for neighbors or other operations.

Liability Coverage Addresses Farm-Specific Injury Risks

Liability coverage handles medical bills and legal costs when someone gets injured on your property or by your animals, and this is where farm policies diverge sharply from homeowners coverage because farm liability limits often need to reach $500,000 or higher to reflect the actual risk. Liability protection for farm operations should include extensions for hired workers and contractors since your standard coverage may not apply when someone else works on your property. Most Idaho farm policies also include coverage for farm outbuildings like barns and storage sheds, though you’ll want to verify whether structures built before 1990 receive replacement cost or actual cash value coverage since older buildings affect premium calculations differently.

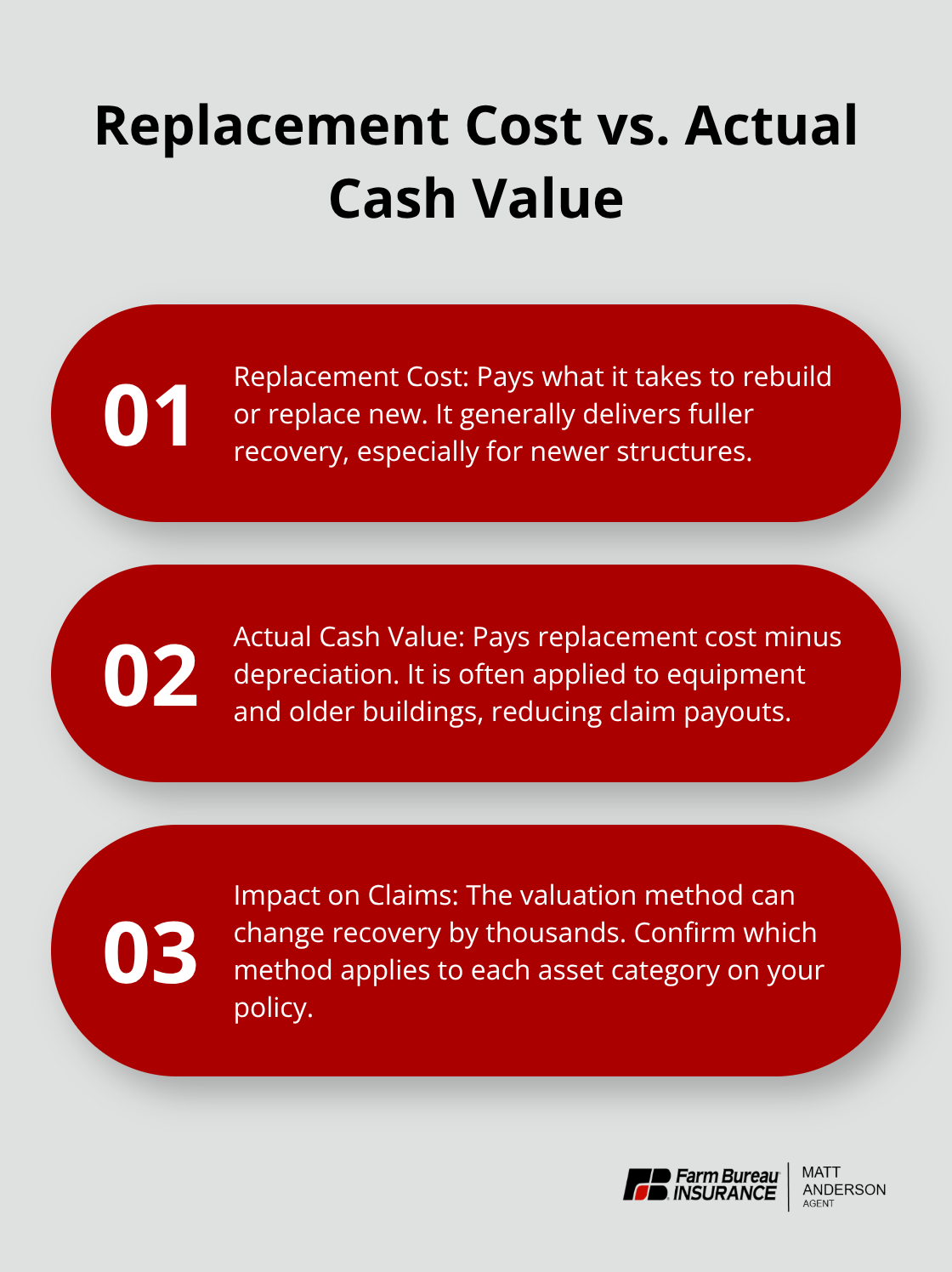

Choosing Between Replacement Cost and Actual Cash Value

The coverage you select directly impacts what happens after a loss. Replacement cost coverage pays what it costs to rebuild or replace an item new, while actual cash value subtracts depreciation from that amount. Newer farm buildings typically qualify for replacement cost protection, but insurers often apply actual cash value to equipment and older structures.

This difference can mean thousands of dollars in recovery after a significant loss, so clarify with your provider which valuation method applies to each asset category on your farm.

Tailoring Coverage to Your Seasonal Operations

Farm operations shift dramatically across seasons, and your insurance should reflect those changes. Higher grain storage during harvest months creates different risk profiles than winter months when silos sit empty. Adjusting your coverage limits seasonally prevents you from overpaying during low-risk periods while maintaining adequate protection when your assets reach peak value. Your provider can help you establish a schedule that matches your actual operational calendar rather than applying one-size-fits-all limits year-round.

Understanding these coverage categories positions you to evaluate which specific limits and endorsements your farm operation actually needs.

Selecting Farm Coverage That Matches Your Actual Operation

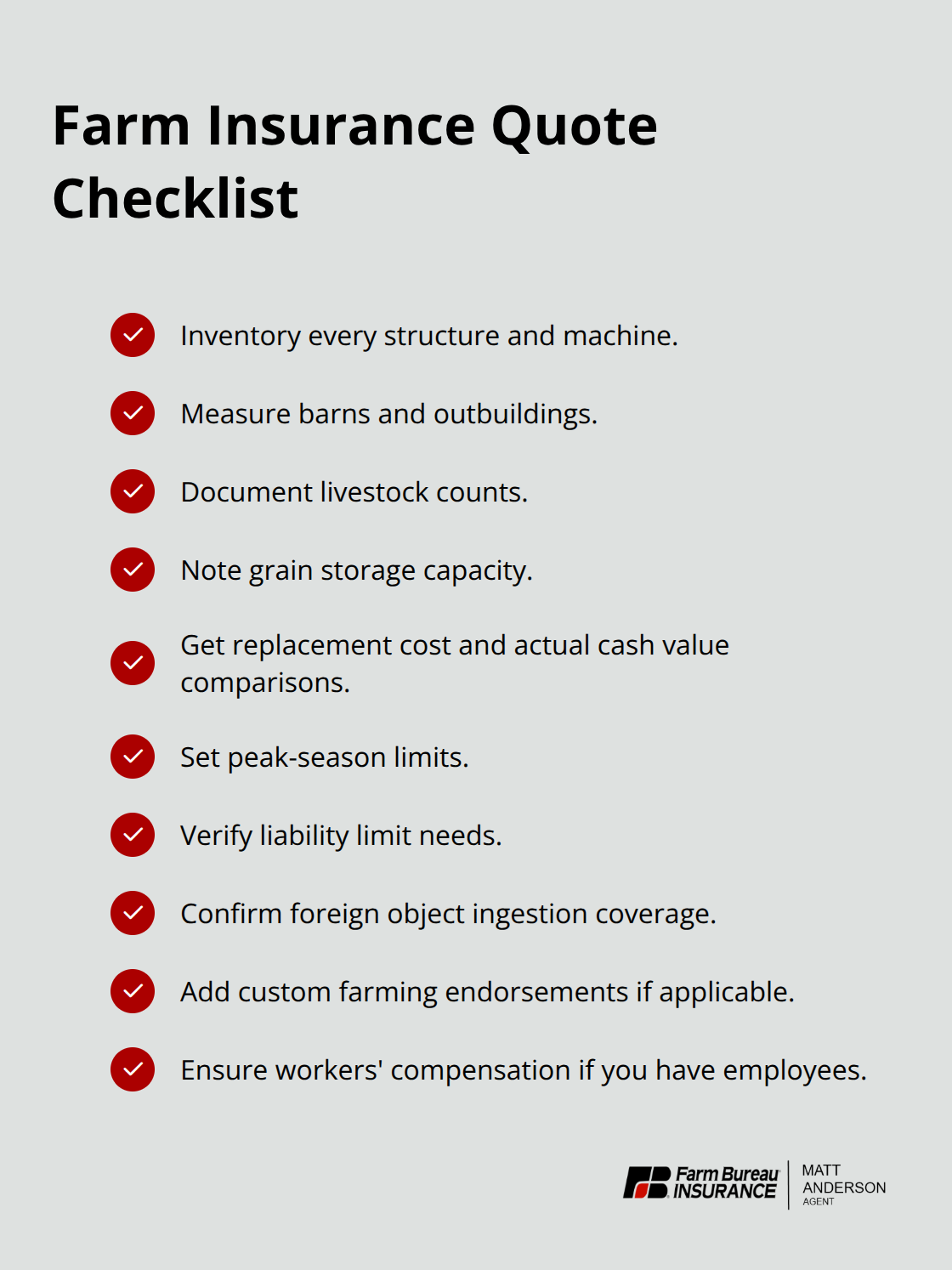

Inventory Every Asset on Your Property

Walk through your property with a notepad and photograph every structure, piece of equipment, and asset that generates value. Most farmers significantly underestimate what they own until they physically inventory it. Measure your barns and outbuildings, list every piece of equipment with its age and condition, document livestock counts, and note any grain storage capacity. This isn’t theoretical-underinsurance on farm properties means you absorb the loss yourself after a claim. A combine purchased five years ago for $350,000 may be worth $210,000 today under actual cash value, but many farmers insure it at the original purchase price and then face a significant shortfall if it’s stolen or damaged.

Compare Replacement Cost Against Actual Cash Value

Get replacement cost quotes for new structures and equipment, then compare those figures against actual cash value estimates to understand the real difference in coverage and premium. Your farm’s seasonal nature demands specific attention: if you store 50,000 bushels of grain during harvest but hold only 5,000 bushels in winter, your peak-season coverage should reflect that higher value while your off-season limits drop accordingly. Request quotes that explicitly show how liability limits scale-$300,000 in coverage may feel adequate until you consider that a serious injury on your property can generate $500,000 or more in medical and legal expenses.

Account for Workers’ Compensation Requirements

Idaho farm operations with employees must also account for workers’ compensation, which is required by the Idaho Industrial Commission for any business with employees (including seasonal labor). This coverage protects your workers and shields your operation from liability if an employee suffers a work-related injury on your farm.

Request Detailed Quotes From Multiple Providers

When comparing providers, request detailed quotes that break down dwelling coverage, equipment and machinery protection, liability limits, and any endorsements your operation requires. Ask each provider whether their policies include foreign object ingestion coverage for equipment, whether custom farming endorsements are available if you perform work for other operations, and whether livestock coverage extends to attacks by dogs or wild animals. Some insurers apply replacement cost to barns built after 1990 but shift to actual cash value for older structures, which affects your long-term costs significantly.

Verify that liability coverage includes medical payments for visitors and that it protects you if contractors work on your property-this gap leaves many farmers exposed. Request quotes for peak-season adjustments during your highest-value months rather than paying year-round rates for maximum coverage you only need four months annually.

Prioritize Coverage Fit Over Price Alone

The most common mistake farmers make is shopping primarily on price rather than on whether the policy actually covers their operation-a $200 annual savings means nothing if a claim reveals your equipment or structures fell outside your coverage.

Final Thoughts

Idaho farm home insurance protects what standard homeowners policies won’t touch, and adequate coverage makes the difference between financial recovery and catastrophic loss after a claim. Your farm operation faces distinct risks that demand specialized protection across dwelling structures, equipment, liability, and seasonal asset fluctuations. A barn fire, equipment theft, or serious injury on your property can generate costs exceeding $500,000, and underinsurance means you absorb those expenses yourself rather than your insurer covering them.

The coverage decisions you make now directly impact your financial security during Idaho’s farming cycles. Choosing replacement cost over actual cash value, adjusting limits seasonally to match your operational calendar, and including endorsements for foreign object ingestion and custom farming work all shape whether your policy actually protects your operation when you need it most. Many farmers discover coverage gaps only after a loss occurs, which is why you should walk through your property to inventory every asset and compare detailed quotes from multiple providers before you commit to a policy.

We at Matt Anderson Insurance understand the specific protection rural Idaho families and farms require. Contact us to discuss your farm’s unique insurance needs and get a quote that reflects your actual assets and seasonal operations.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.