Idaho Auto Insurance Rates: What Factors Drive Your Premium

Your Idaho auto insurance rates depend on more than just luck. Insurance companies use specific factors-your driving history, age, vehicle type, and location-to calculate what you pay each month.

At Matt Anderson Insurance, we help Idaho drivers understand these factors so they can make smarter choices about their coverage and find real ways to save money.

What Really Drives Your Idaho Auto Insurance Premium

Your Driving Record Sets the Foundation

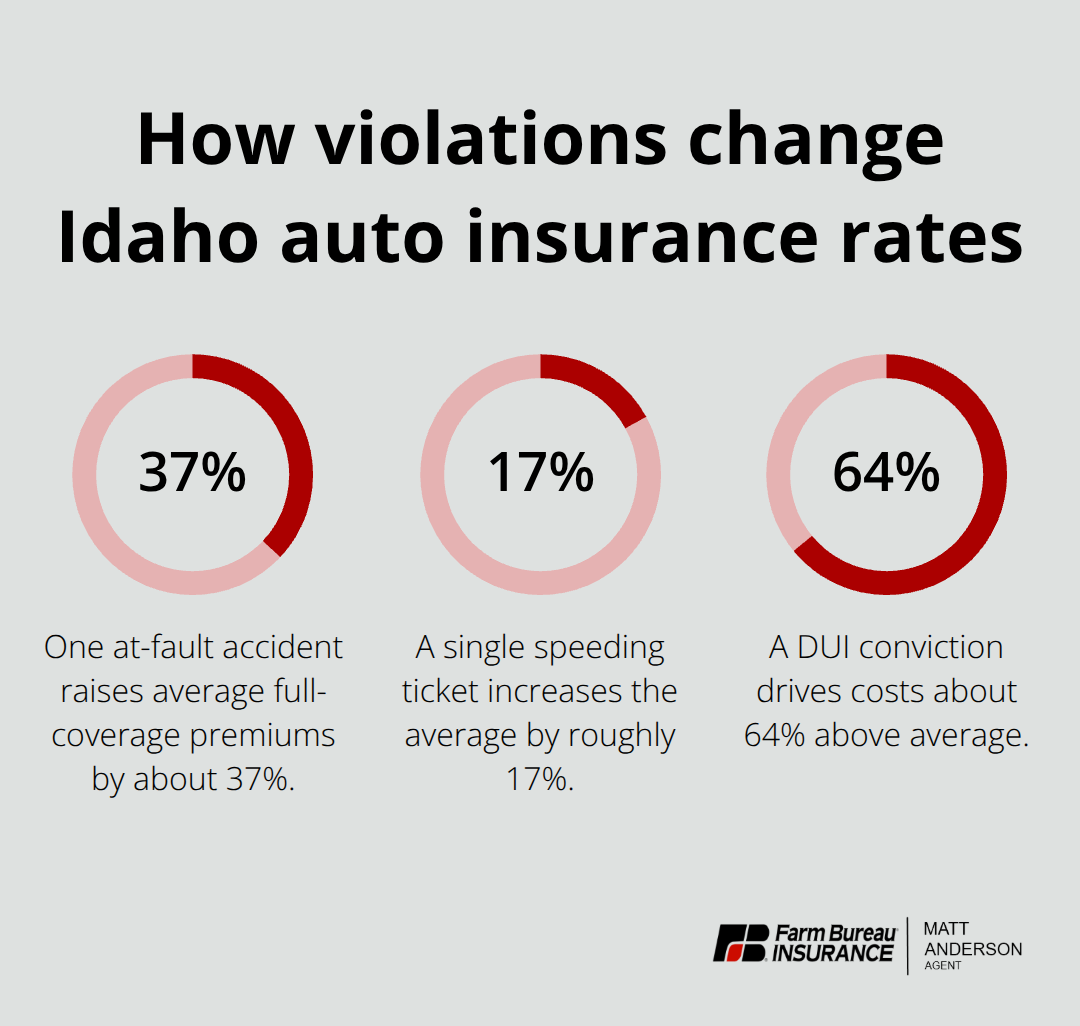

Your driving record is the single biggest factor insurers examine when calculating your rate, and the data backs this up. A clean record keeps you around the Idaho average of roughly $1,476 per year for full coverage, according to Bankrate’s analysis of Quadrant Information Services data from November 2025. One at-fault accident raises that to about $2,023 per year-a 37 percent jump. A speeding ticket alone pushes you to around $1,731 per year, roughly 17 percent higher. A DUI conviction is far worse, landing you at approximately $2,423 per year, about 64 percent above average.

Claims history matters just as much as individual incidents. Frequent claims signal higher risk and keep your premiums elevated for three to five years after each incident. This means avoiding small claims is often smarter than filing them-you pay a few hundred dollars out of pocket for minor damage and protect your rate from climbing significantly.

Age and Experience Shape Your Cost

An 18-year-old on their own policy pays around $4,580 for full coverage, roughly 76 percent more than the state average, while a 20-year-old pays about $3,278, still 46 percent above average. These costs drop steadily as you age; by 25, premiums fall to around $1,951, and by 60, they settle near $1,313. Insurers view younger drivers as higher risk because they lack experience behind the wheel and statistically cause more accidents.

Vehicle Type and Safety Features Impact Your Premium

Your vehicle choice directly affects your bill. A Toyota Camry costs about $1,476 per year to insure, while a BMW 330i runs approximately $1,878, and a Honda Odyssey comes in around $1,277. Luxury and high-performance vehicles cost significantly more because repair parts and labor are expensive. A vehicle’s safety rating also influences your premium-cars with higher ratings qualify for discounts that lower your annual cost. When you choose a vehicle with excellent safety features and reasonable repair costs, you save money over the life of ownership.

These three factors-your driving record, age, and vehicle-form the core of how insurers price your policy. But location within Idaho and your personal financial profile add another layer of complexity to your final rate.

Where You Live and Your Money Matter More Than You Think

Location Within Idaho Creates Real Price Differences

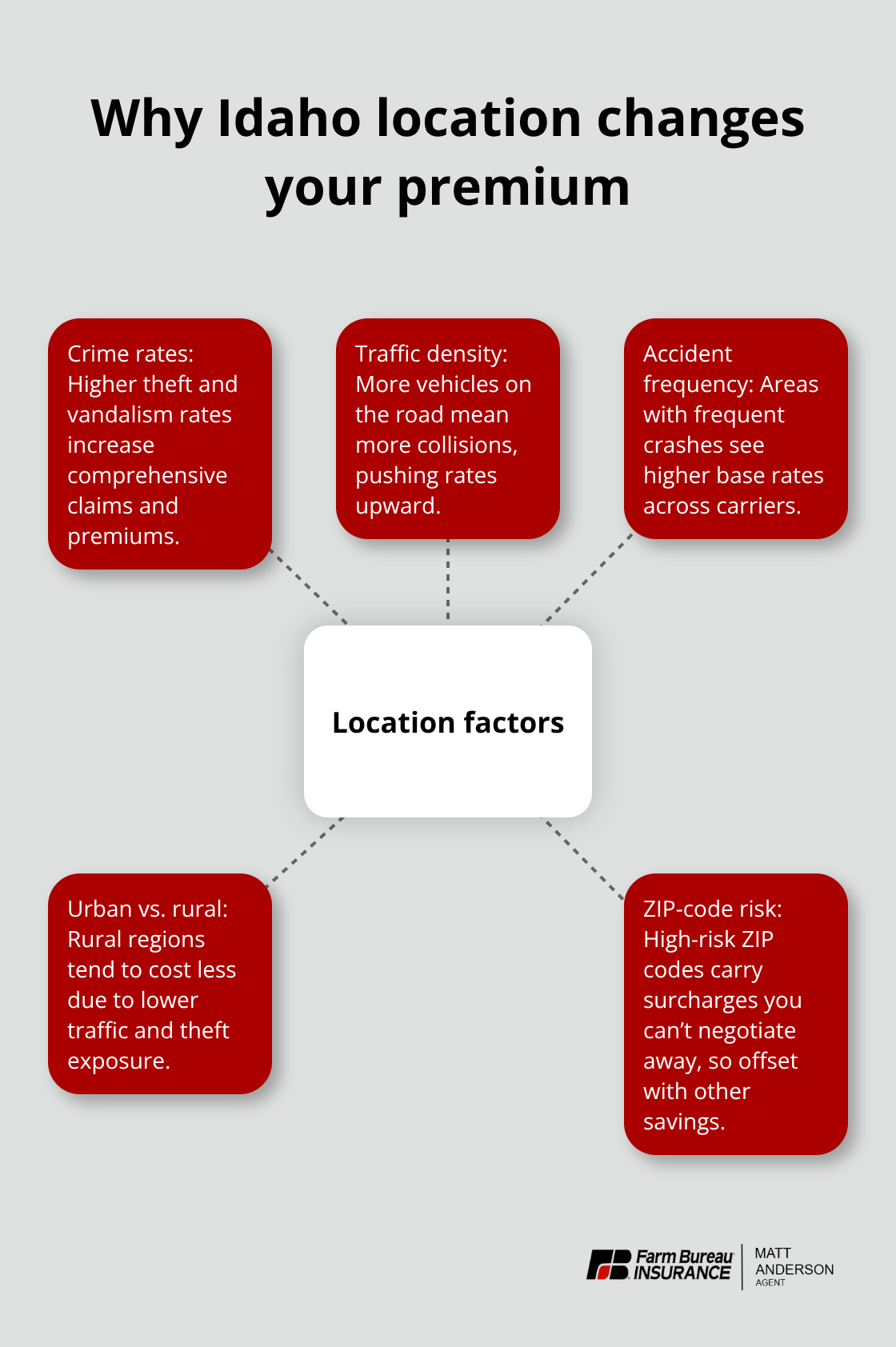

Where you live in Idaho fundamentally shapes what you pay for auto insurance, and the differences are substantial. Boise drivers pay around $1,354 per year for full coverage, while Caldwell residents pay approximately $1,493 and Nampa drivers around $1,454, according to Bankrate’s November 2025 analysis. These variations stem from local crime rates, traffic density, and accident frequency in each area. Rural Idaho generally offers lower premiums than urban centers because fewer cars on the road means fewer collisions and theft incidents.

If you live in a high-risk ZIP code, you cannot negotiate your way out of that geographic penalty, but you can control other factors to offset it.

Your Credit Score Carries Surprising Weight

Your credit score directly influences your rate in Idaho, and the impact is severe. Drivers with poor credit pay roughly 49 percent more than the state average, while those with excellent credit save about 11 percent compared with average rates. This means a driver with poor credit might pay $2,200 annually while an excellent-credit driver in the same location pays around $1,310. Improving your credit takes time, but even modest increases over six to twelve months can lower your next renewal quote. Payment history matters as much as your overall score-consistently paying bills on time signals financial responsibility to insurers, and they reward that stability with lower rates.

Deductibles and Coverage Limits Control Your Out-of-Pocket Costs

How you structure your coverage directly controls your premium. Raising your deductible from $500 to $1,000 typically reduces your annual premium by 10 to 25 percent, which translates to $150 to $370 in savings depending on your base rate. Higher deductibles work well if you have emergency savings and drive carefully; lower deductibles suit drivers who cannot absorb unexpected out-of-pocket costs.

Idaho requires minimum liability coverage of $25,000 per person and $50,000 per accident for bodily injury, plus $15,000 for property damage, but these minimums leave you exposed to serious financial risk. If you cause an accident and someone’s medical bills exceed your coverage limits, you become personally liable for the remainder. Upgrading to $50,000 per person and $100,000 per accident costs more monthly but protects your assets far better. Most drivers renew on autopilot without adjusting anything, yet your financial situation and driving patterns change annually-a review of your coverage limits each year makes real sense.

These location, credit, and coverage decisions set the stage for the final piece of the puzzle: the concrete actions you can take to lower your costs without sacrificing protection.

How to Actually Lower Your Idaho Auto Insurance Costs

Bundle Policies for Immediate Savings

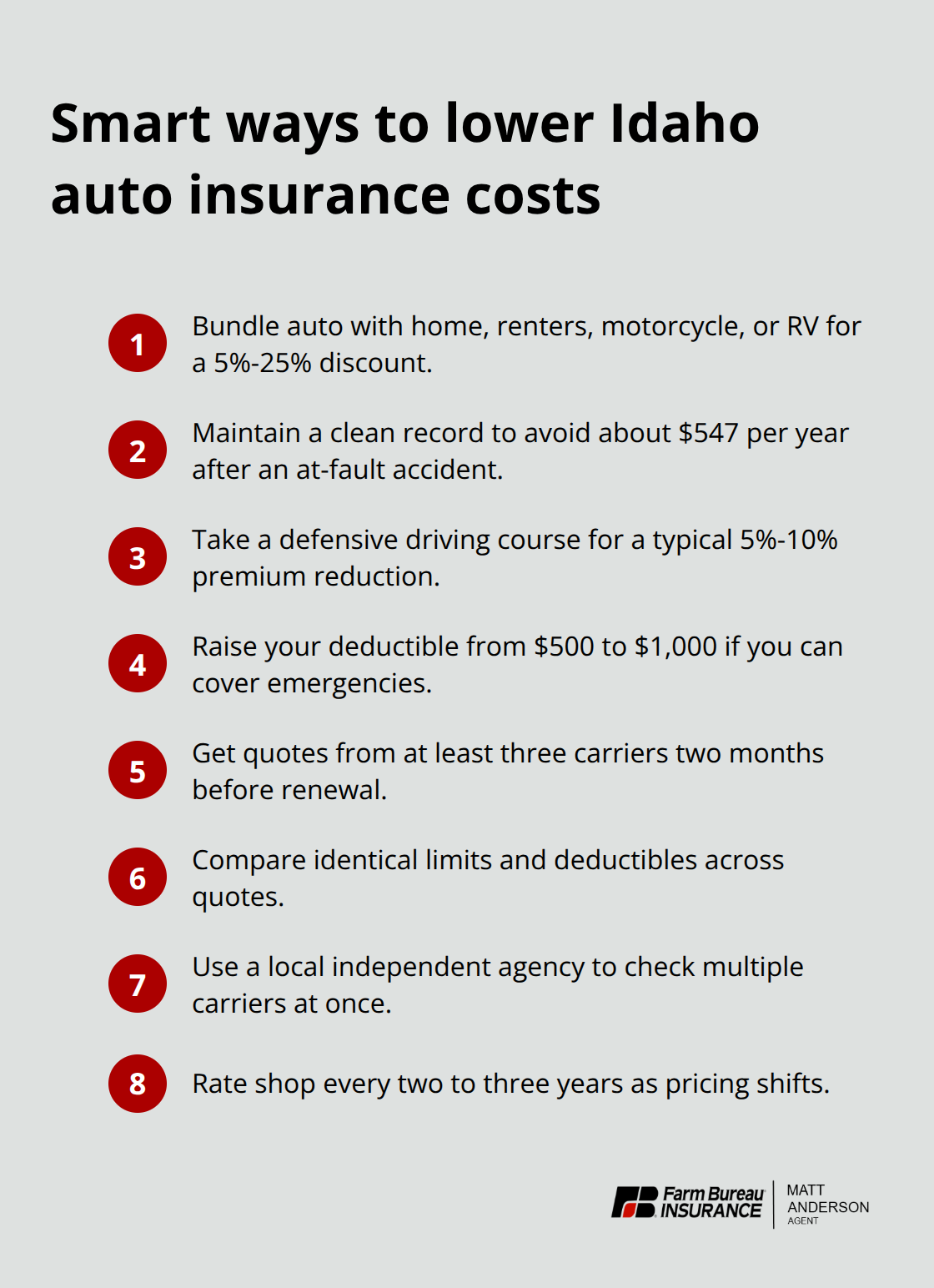

Combining insurance policies cuts your premium without sacrificing coverage. Clients who combine auto with homeowners, renters, motorcycle, or RV coverage under one policy save 5%-25% discount on their total costs. If you own a home and a car, bundling those two alone typically saves hundreds annually. The discount applies immediately at renewal, so consolidating separate policies through different companies with a single agency that offers multiple lines creates instant savings. Many Idaho drivers overlook this because they never ask their current insurer about bundling options, yet it remains one of the most straightforward ways to reduce what you owe each month.

Maintain a Clean Driving Record

Your driving record cannot change overnight, but maintaining a clean record going forward is the single most powerful lever you control. Each year without an accident or ticket keeps your rate stable or allows it to drop as you age and build experience. A single at-fault accident costs you roughly $547 more per year compared to the state average, and that premium penalty sticks around for three to five years. Defensive driving courses offered through organizations like the Idaho Transportation Department can qualify you for discounts with most carriers, typically saving 5 to 10 percent on your annual premium. The investment in a course costs $30 to $50 but pays for itself many times over if it prevents even one minor incident that would have triggered a claim. Committing to habits that reduce risk-avoiding phone use while driving, leaving extra space between vehicles, and adjusting your speed for weather conditions-all lower your accident likelihood and protect your rate.

Shop Multiple Carriers Before Renewal

Rates for identical coverage vary dramatically across insurance companies, sometimes by hundreds of dollars annually for the same driver profile. According to Bankrate’s November 2025 analysis, some carriers price 9 percent below the Idaho state average while others charge well above it for the same risk level. Waiting until your renewal notice arrives and paying the quoted amount is expensive. Instead, get quotes from at least three carriers two months before your renewal date, providing identical coverage limits and deductibles to each one. This comparison takes roughly 30 minutes online or by phone and frequently uncovers $200 to $400 in annual savings.

Local independent agencies compare multiple carriers at once rather than forcing you to contact each company separately, which saves time and often reveals discounts you would miss shopping alone. Rate shopping every two to three years, not just once, matters because carrier pricing shifts constantly as they adjust for local claims experience and market conditions.

Final Thoughts

Idaho auto insurance rates reflect your driving habits, age, vehicle choice, location, credit profile, and coverage decisions. You now control where you save money and where you accept higher costs based on your priorities. Your driving record remains the foundation-one accident or ticket costs hundreds more annually for years, while bundling policies, raising deductibles, and shopping multiple carriers offset geographic penalties that location creates.

Review your current coverage without waiting for renewal and check whether your deductibles and liability limits still match your financial situation. Many Idaho drivers carry outdated coverage that no longer fits their lives, paying for protection they do not need while leaving gaps where they do. Raising a deductible from $500 to $1,000 typically saves 10 to 25 percent annually, and upgrading liability limits from state minimums to $50,000 per person and $100,000 per accident costs more but protects your assets if you cause a serious accident.

Contact Matt Anderson Insurance for a free review of your current coverage and a comparison of rates from multiple carriers. A few minutes of conversation often uncovers hundreds in annual savings while ensuring you have the protection your family actually needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.