Idaho Commercial Vehicle Liability: Why It Should Be Your Policy Priority

One accident involving a commercial vehicle can cost your Idaho business tens of thousands of dollars-or more. Without proper Idaho commercial vehicle liability coverage, you’re personally responsible for medical bills, vehicle repairs, and legal fees that could bankrupt your company.

At Matt Anderson Insurance, we’ve seen too many Idaho business owners operate without adequate protection. This guide walks you through what coverage actually protects you, why it matters in Idaho, and how to pick the right limits for your fleet.

What Commercial Vehicle Liability Actually Protects

Bodily Injury Liability Covers Medical and Wage Losses

Commercial vehicle liability coverage splits into three distinct protections that work together when your vehicle causes injury or damage. Bodily injury liability covers medical expenses, lost wages, and pain-and-suffering claims when your vehicle injures someone. If your delivery truck hits a pedestrian or your service vehicle causes a multi-car pileup, this coverage pays their hospital bills, rehabilitation costs, and any legal settlements. Idaho requires a minimum of $25,000 per person and $50,000 per accident for bodily injury. That minimum sounds reasonable until you calculate actual medical costs-a serious injury requiring surgery and ongoing physical therapy easily exceeds $50,000. Without adequate limits, your business absorbs the difference out of pocket.

Property Damage Liability Handles Repair and Replacement Costs

Property damage liability covers repairs or replacement when your vehicle damages someone else’s vehicle, building, or equipment. Your commercial truck crashes into a storefront, a parked car, or a power line-this coverage handles those repair bills. Idaho’s minimum property damage requirement is $15,000 per accident, which disappears quickly when you damage multiple vehicles or commercial property. A single accident can wipe out this limit in minutes, leaving your business liable for any excess costs.

Legal Defense and Court Settlements Protect Your Business

Legal defense costs and court settlements represent the third layer of protection. If someone sues your business after an accident, liability coverage pays your attorney fees, court costs, and any judgment against you. This protection matters more than most Idaho business owners realize. A lawsuit over a serious accident can drag on for years, generating tens of thousands in legal fees before any settlement is reached.

Why Idaho Minimums Fall Short for Most Operations

Many Idaho businesses operate with minimum coverage because they underestimate how fast costs climb. A single accident involving multiple injured parties or significant property damage can quickly exceed $50,000 in bodily injury claims and $15,000 in property damage. A contractor operating heavy equipment in populated areas faces far greater liability risk than a business with light-duty vehicles traveling primarily rural routes. Your coverage limits should reflect your real-world risk, not just Idaho’s legal minimums. The next step involves assessing your actual exposure based on your vehicle type, routes, and the people or property your operations contact daily.

Why Idaho Minimums Leave Your Business Exposed

Idaho’s Legal Requirements Don’t Match Real-World Costs

Idaho law mandates commercial vehicle liability insurance, but the minimums the state sets are dangerously low for most operations. Idaho requires $25,000 per person and $50,000 per accident for bodily injury, plus $15,000 for property damage. Driving without this coverage carries serious penalties: at least a $75 fine and potential driver’s license suspension. However, the real cost of operating without adequate coverage extends far beyond these penalties. According to Insureon data, commercial auto insurance in Idaho averages about $204 per month or $2,449 annually, yet many business owners skip this protection or settle for bare-minimum limits to save money. That decision creates catastrophic financial exposure.

A Single Accident Can Exceed Your Coverage Limits

A single accident involving serious injuries or multiple vehicles generates medical bills, repair costs, and legal fees totaling $200,000, $500,000, or more. Your business becomes personally liable for amounts exceeding your policy limits, meaning creditors pursue your company’s assets, equipment, and bank accounts to satisfy the judgment. A contractor’s heavy truck causes a multi-vehicle collision on Interstate 84, injuring four people and damaging three vehicles. Medical expenses alone-surgeries, emergency care, rehabilitation-total $180,000 across the four injured parties. Vehicle repairs and property damage add another $65,000. Your $50,000 bodily injury limit covers only a fraction of the medical costs, and your $15,000 property damage limit disappears on the first two vehicles. Your business owes the remaining $195,000 out of pocket, plus legal defense costs if the injured parties sue. Without adequate coverage, you face bankruptcy, asset seizure, and personal liability that follows you beyond the business itself.

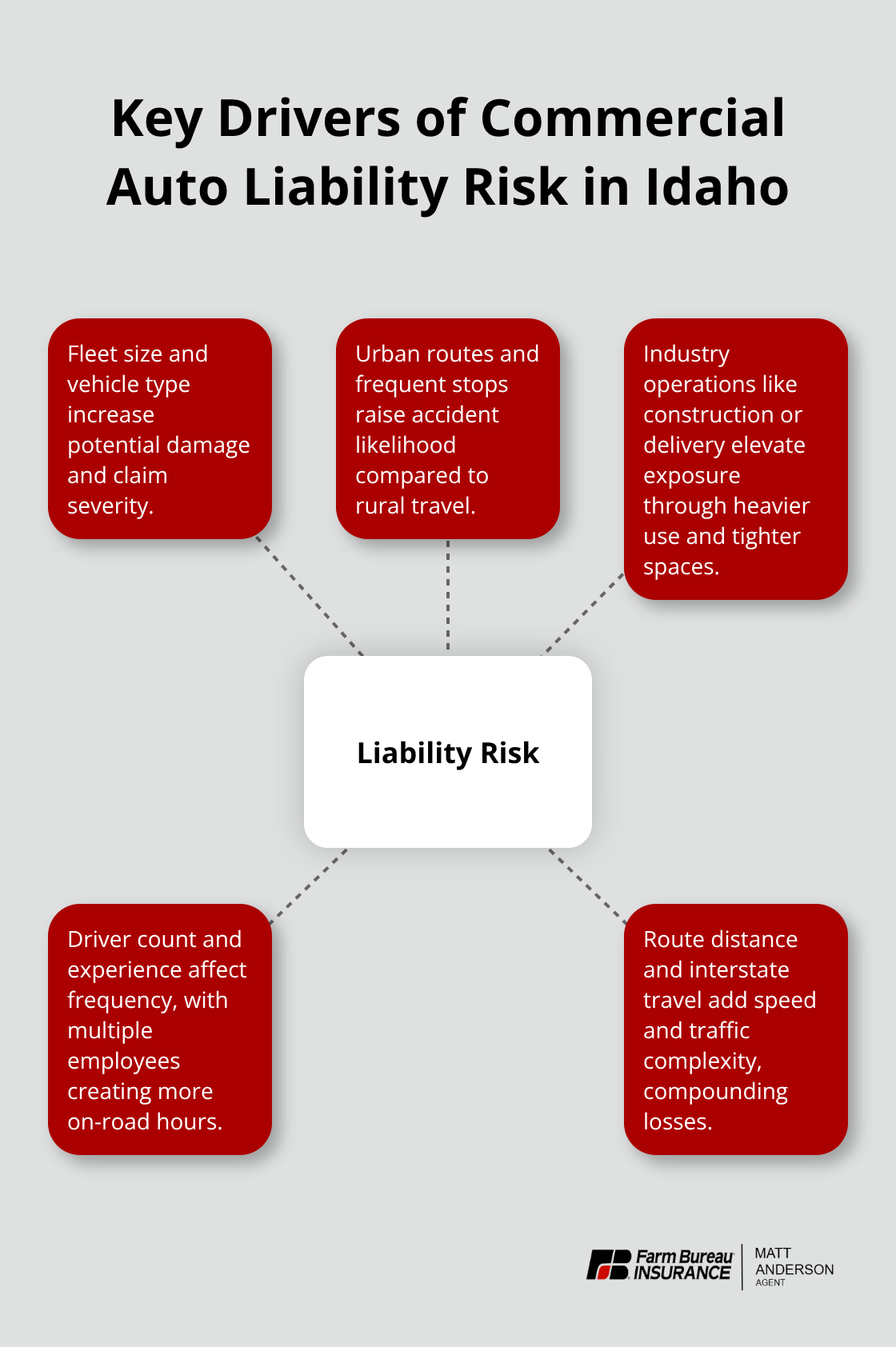

Industry and Location Amplify Your Liability Risk

Industry-specific risks amplify this exposure significantly. Contractors operating in populated areas, delivery services making frequent stops in cities, and service businesses with multiple employees all face heightened liability compared to operations confined to rural routes. A landscaping company operating multiple trucks in Meridian or Boise encounters greater claim frequency and severity than one serving smaller towns, yet many Idaho businesses fail to adjust their coverage limits accordingly. The difference between minimum coverage and adequate coverage often costs only $50 to $150 more per month, yet that small premium difference stands between financial stability and potential ruin after a serious accident.

Understanding your actual liability exposure requires honest assessment of your fleet, routes, and the people or property your operations contact daily. The next step involves matching your coverage limits to these real-world risks rather than relying on Idaho’s baseline requirements.

Sizing Your Coverage to Match Your Actual Risk

Fleet Composition Determines Your Coverage Foundation

Start with your fleet composition and daily operations, not Idaho’s legal minimums. A plumbing contractor operating two service vans in Boise faces different liability exposure than a landscaping company running eight trucks across multiple counties or a delivery service making fifty stops daily in populated areas. Your coverage limits should scale with vehicle count, vehicle size, employee count, and geographic reach. According to Insureon data, commercial auto insurance in Idaho averages $204 monthly, but this baseline shifts dramatically based on fleet size and operational complexity. A single vehicle operation might pay $150 monthly while a five-vehicle fleet could pay $400 or more.

Premium Increases Deliver Substantial Coverage Upgrades

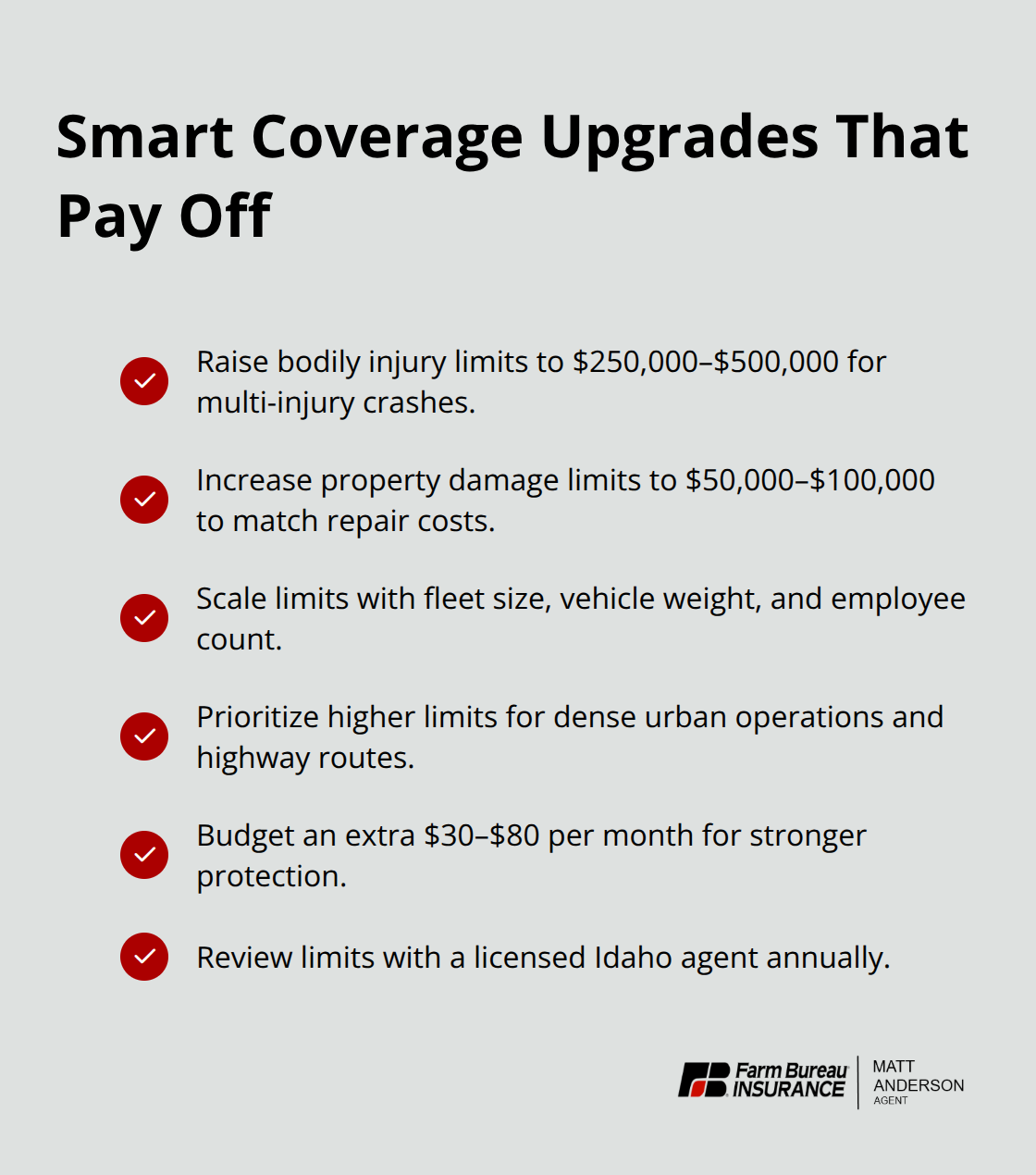

Most Idaho business owners treat insurance costs as fixed rather than recognizing that modest premium increases buy substantial coverage upgrades. Moving from Idaho’s minimum liability limits to $100,000 or $250,000 typically adds $30 to $80 monthly-roughly $360 to $960 annually. That difference becomes invaluable after an accident involving multiple injured parties or high-cost medical treatment.

Heavy equipment operators, contractors working near highways, and service businesses operating in dense urban areas should strongly consider $250,000 to $500,000 bodily injury limits and $50,000 to $100,000 property damage limits. These higher thresholds align with actual accident costs rather than relying on state minimums that haven’t been updated to reflect modern medical expenses and vehicle values.

Industry and Location Shape Your Risk Profile

Your industry and operational patterns determine specific risk categories that standard policies may not adequately address. Construction contractors operating heavy equipment, tow truck operators, and food service vehicles have distinct liability profiles requiring tailored limits. Travel radius matters significantly-local service routes within a single city carry lower risk than regional operations spanning multiple counties or interstate corridors. FMCSA data shows that large truck fatality rates vary substantially by state and carrier type, and Idaho’s position within these national patterns should inform your coverage strategy. If your operations involve hazardous materials, employee passengers, or high-value cargo, you need coverage that exceeds standard commercial auto limits.

Local Agent Review Identifies Your True Exposures

A licensed local agent who understands Idaho-specific risks and your industry’s particular exposures can analyze your vehicle types, driver profiles, past claims history, and operational footprint to recommend limits that provide genuine protection rather than false economy. Most Idaho businesses operating multiple vehicles or serving populated areas benefit from bodily injury limits between $100,000 and $300,000 and property damage limits of $50,000 to $100,000. This positioning keeps premiums reasonable while eliminating the catastrophic gap between minimum coverage and real-world accident costs that bankrupts unprepared businesses.

Final Thoughts

Commercial vehicle liability insurance protects your Idaho business from financial devastation after an accident-and the protection costs far less than most business owners expect. Moving from Idaho’s minimum coverage to adequate limits adds only $30 to $80 monthly, yet that small investment eliminates the catastrophic gap between state minimums and real-world accident costs that bankrupts unprepared operations. Your fleet, routes, and daily operations determine the specific Idaho commercial vehicle liability coverage you need, not outdated state requirements that haven’t kept pace with modern medical expenses and vehicle values.

We at Matt Anderson Insurance work with contractors, service businesses, delivery companies, and fleet operators across Idaho to build coverage that matches your actual exposure. Our licensed agents analyze your vehicles, your operations, and the people or property you contact daily to recommend limits that provide genuine protection without unnecessary cost. Contact Matt Anderson Insurance to schedule a coverage review and discover what adequate protection truly costs for your business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.