Idaho Homeowners Insurance Discounts: Maximize Your Savings

Idaho homeowners insurance discounts can significantly reduce what you pay each year. We at Matt Anderson Insurance know that most homeowners leave money on the table by not taking advantage of available savings.

This guide walks you through the main discount opportunities available to Idaho homeowners, from bundling policies to upgrading your home’s safety features. You’ll learn exactly which changes qualify for discounts and how to stack them for maximum savings.

How Bundling Policies Creates Your Biggest Savings

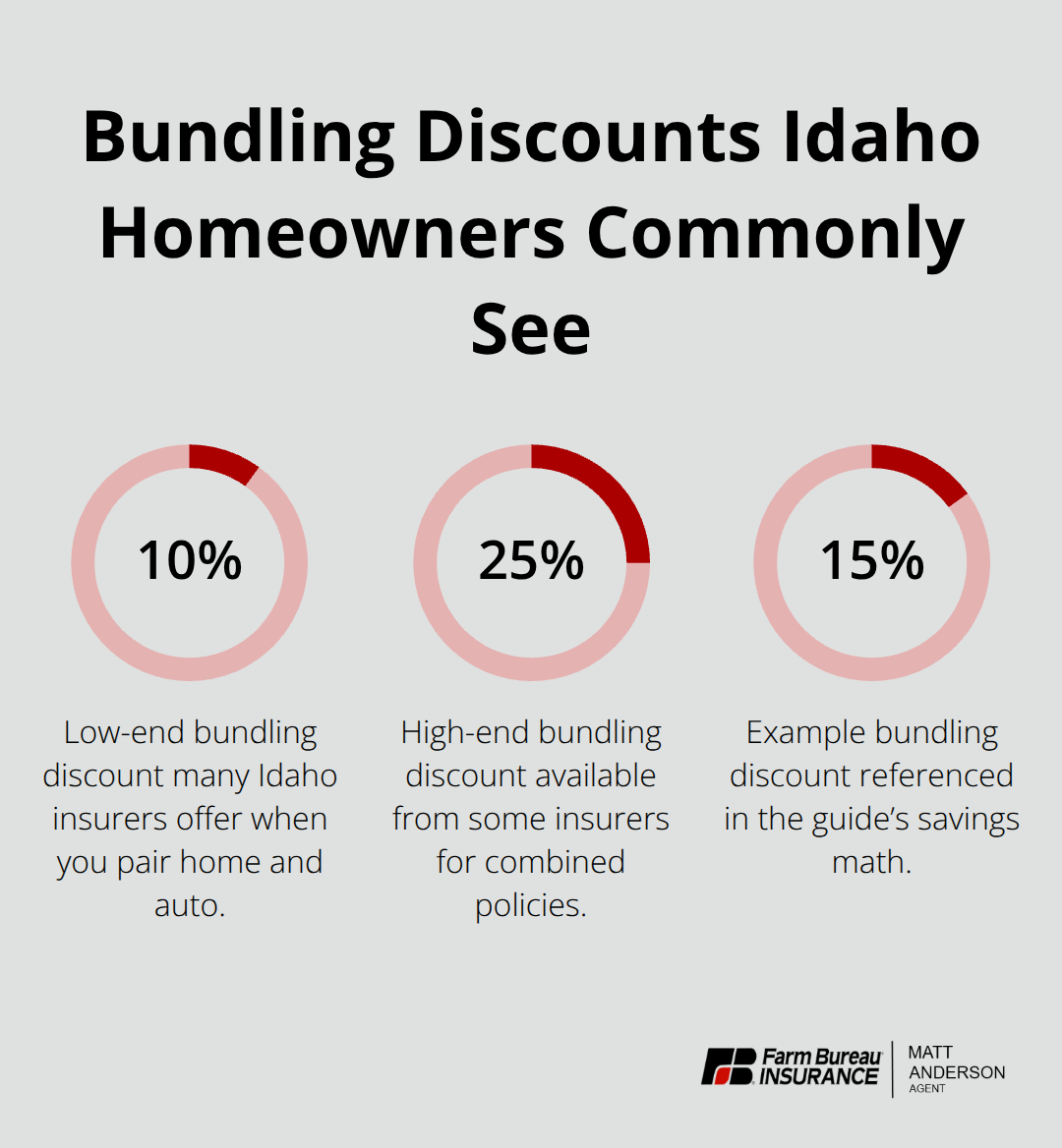

Combining your home and auto insurance with a single provider is the fastest way to reduce your annual premiums. Most Idaho insurers offer bundling discounts that range from 10% to 25% off your total bill when you pair policies together. Allstate is known for a broad set of discounts including bundling incentives, while State Farm provides strong digital tools to manage multiple policies in one place. We at Matt Anderson Insurance help Idaho homeowners and vehicle owners bundle their coverage across auto, home, boats, RVs, short-term rental properties, and umbrella policies-all designed to stack savings and simplify management.

The key is requesting identical coverage limits and endorsements from each insurer when you compare quotes, so you’re comparing apples to apples and can see the true bundling discount.

Stack Additional Coverage for Multiplied Discounts

Adding a third or fourth policy amplifies your savings significantly. If you own a boat, RV, or manage a short-term rental property, bundling that coverage with your home and auto policies often triggers additional discount layers. Bundling home and auto with umbrella coverage extends your liability protection beyond standard homeowners limits while lowering your combined premium. Homeowners who maintain a clean claims history qualify for loyalty discounts on top of bundling savings, creating a compounding effect. Your agent should provide a detailed breakdown showing what each discount contributes to your final bill-bundling, claims-free status, safety features, and any other applicable reductions. This transparency lets you see exactly where your savings come from and what additional steps might unlock more discounts.

Pay Your Premium Upfront to Capture Extra Savings

Paying your full annual premium in one lump sum rather than in monthly installments often qualifies you for an additional discount of 2% to 5%. This savings applies whether you bundle or not, but it compounds when combined with other discounts. If you have the cash flow available, this is one of the simplest ways to reduce costs without changing your coverage. The math is straightforward: a typical Idaho homeowners policy could drop by $28 to $70 just by paying upfront. When you layer this onto a bundling discount of 15%, your total annual savings can exceed $300 or more depending on your specific rates and coverage choices.

Home improvements and safety features offer another powerful path to lower your premiums-and we’ll show you exactly which upgrades qualify for the biggest discounts.

Which Home Upgrades Deliver the Biggest Insurance Discounts

Roof Replacement Offers Your Fastest Savings

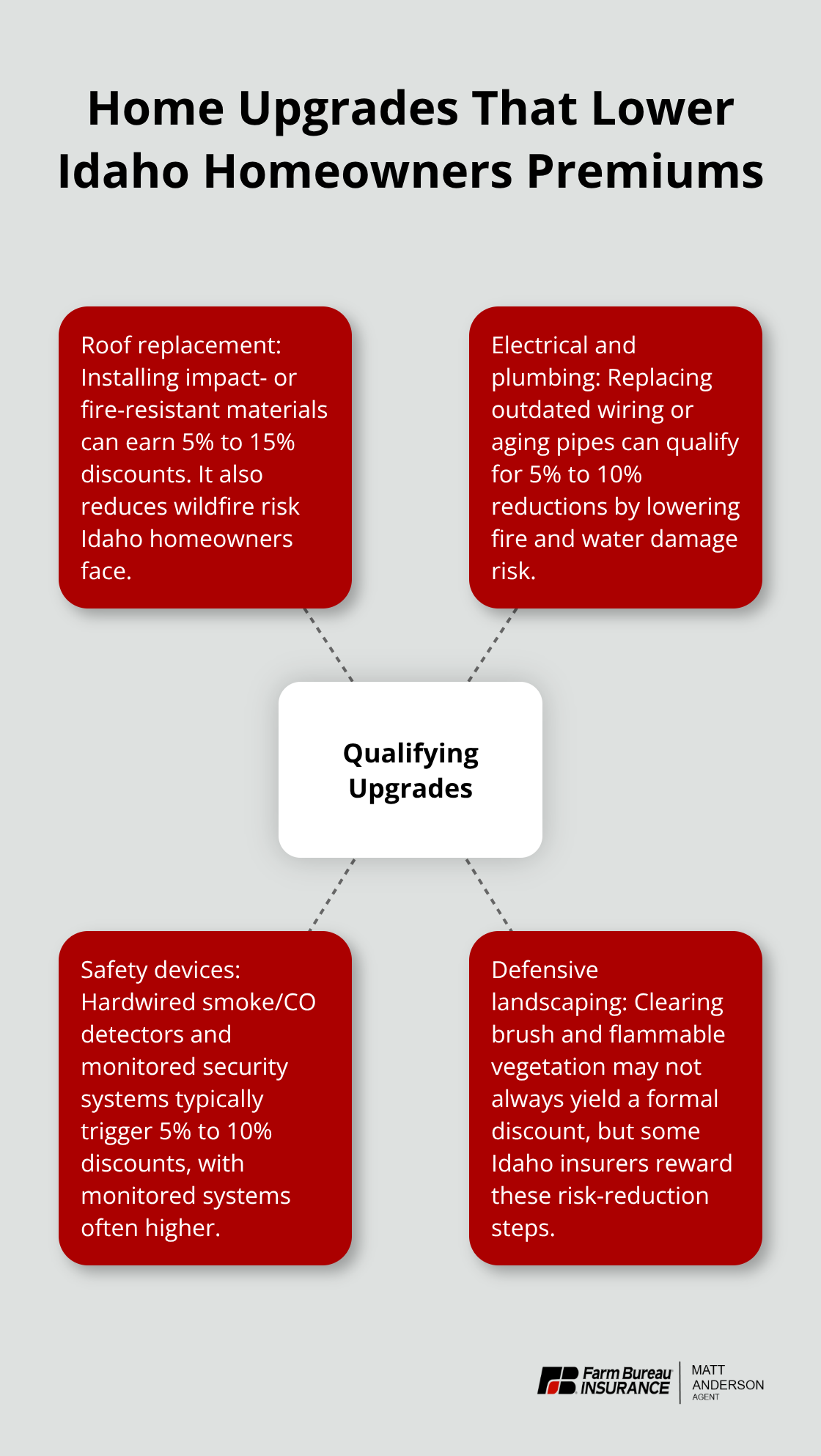

Installing a new roof stands out as the single most effective upgrade for lowering your Idaho homeowners premium. A roof replacement with impact-resistant or fire-resistant materials qualifies you for discounts ranging from 5% to 15% depending on your insurer and the materials you select. One Idaho homeowner received a roughly $140 discount after installing a new roof, which prevented what could have been a 50% premium increase. This matters because Idaho faces serious wildfire risk-the state logged 15 of the nation’s 100 fastest fires over two decades, second only to California according to fire research from the University of Colorado. When you upgrade to Class A fire-rated roofing or impact-resistant shingles designed to handle hail and wind, insurers recognize the reduced risk and price accordingly.

Ask your insurer upfront what roofing materials qualify for the largest discount before you commit to a contractor. Metal roofing, architectural shingles with high wind ratings, and tile all tend to trigger meaningful savings. The practical approach is to request a detailed list of roofing materials your insurer recognizes for discounts, then compare the cost of each option against the annual savings you’ll receive.

Electrical and Plumbing Upgrades Reduce Hidden Risks

Upgrading electrical and plumbing systems lowers premiums because newer wiring and pipes reduce fire and water damage risk. If your home has outdated knob-and-tube wiring or aging copper pipes prone to corrosion, replacing those systems qualifies you for 5% to 10% discounts. Many insurers require electrical upgrades in homes built before 1950, and some charge higher premiums or exclude coverage until improvements are made. These upgrades address real hazards that drive claim costs, so insurers reward the investment with rate reductions that compound over time.

Safety Devices Trigger Immediate Discounts

Installing a security system or hardwired smoke detectors and carbon monoxide detectors provides another straightforward path to savings. These safety features typically trigger 5% to 10% discounts because they reduce claim frequency and severity. A professionally monitored alarm system often qualifies for a larger discount than a self-monitored system, so verify with your agent what your specific insurer recognizes.

The cost of these devices (typically $300 to $1,500 for a monitored system) pays for itself within a few years through premium reductions alone.

Defensive Landscaping and Wildfire Mitigation

Homeowners in high wildfire zones should consider defensive landscaping-removing dead trees, clearing brush within 30 feet of structures, and eliminating flammable vegetation near eaves and decks. While defensive landscaping doesn’t always trigger a formal discount, some Idaho insurers reward these steps with rate reductions or waived rate increases. Call your current insurer and ask for a detailed list of safety upgrades and home improvements they offer discounts for, then prioritize the changes that deliver the fastest return on investment. A $5,000 roof upgrade earning a $140 annual discount takes roughly 36 years to break even on cost alone, but the real value lies in reduced wildfire risk, better home resale value, and avoided premium increases that could exceed $500 per year in volatile markets like Idaho’s.

These home improvements form one pillar of your savings strategy. Your claims history and loyalty to your insurer create another powerful opportunity to lower what you pay each year.

How Your Claims History and Loyalty Shape Your Premiums

Your claims history is the single most predictive factor insurers use to price your policy, often overshadowing home value and location. Homeowners who avoid filing claims for small damages qualify for loyalty discounts that accumulate year after year, sometimes reaching 10% to 20% off your base premium depending on your insurer. The math is straightforward: if you have a $1,400 annual premium and maintain a clean claims history for five years, that 10% to 15% discount translates to $700 to $1,050 in total savings. Idaho’s insurance market has tightened significantly-total homeowner policies declined roughly 9% from 2022 to 2023 according to the Idaho Department of Insurance, and premiums rose about 37% during that same period. In this volatile environment, insurers reward stability and low-risk customers with better rates. Staying with your current insurer matters because most companies offer explicit loyalty discounts after three to five years without a lapse, even if you shop around occasionally.

Why Small Claims Cost More Than You Think

The key is avoiding the temptation to file a claim for minor damage that falls below or slightly above your deductible. A $2,000 roof leak repair might trigger a $500 to $1,000 rate increase over three years, completely offsetting any insurance payout after you subtract your deductible. Most insurers keep claims history for five to seven years, meaning a water damage claim filed today could drive up your premiums for the next half-decade. Ask your agent for a detailed breakdown of how filing a claim would affect your rate before you submit anything. Some insurers offer claim forgiveness programs for your first claim or waive rate increases if you maintain five years of clean history, so verify what your specific policy includes.

If you face a $3,000 loss and your deductible is $1,000, you net only $2,000 in coverage-but filing that claim could cost you $500 to $800 annually in higher premiums over five years, totaling $2,500 to $4,000 in extra costs. The practical approach is to pay small damages out of pocket and reserve insurance claims for genuinely catastrophic losses that exceed $5,000 or more.

Request a Complete Discount Inventory From Your Insurer

Contact your insurer directly and request a complete list of discounts you currently qualify for and what additional steps would unlock more savings. Many homeowners miss out on discounts simply because they never ask. Insurers often have 15 to 25 different discount categories, but agents only mention the most common ones unless you push for a full accounting. Ask specifically about good homeowner discounts, which some companies offer for maintaining continuous coverage without lapses, paying on time, and avoiding claims. Your agent should provide a detailed breakdown showing what each discount contributes to your final bill-bundling, claims-free status, safety features, and any other applicable reductions. This transparency lets you see exactly where your savings come from and what additional steps might unlock more discounts.

Final Thoughts

Idaho homeowners insurance discounts stack together to create substantial savings when you take action. Bundling home and auto coverage typically saves 10% to 25% off your total premium, while roof replacements and security systems reduce your bill by another 5% to 15%. A homeowner paying $1,400 annually can realistically drop that to under $900 with the right combination of discounts and upgrades.

Contact your insurer today and request a complete discount inventory. Ask which safety upgrades, home improvements, and coverage adjustments would lower your premium, and demand a detailed breakdown showing exactly what each discount contributes to your final bill. If your insurer cannot provide this transparency, that signals you should shop around for better service.

We at Matt Anderson Insurance help Idaho homeowners identify and stack these savings without sacrificing coverage. Our licensed agents work with you to bundle auto, home, boats, RVs, and umbrella policies while uncovering discounts you might otherwise miss. Contact us today for a free policy review and discover how much you can save on Idaho homeowners insurance discounts.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.