Idaho Contractor Equipment Coverage: Safeguarding Tools and Machinery

Your tools and machinery are the backbone of your contracting business. Without proper protection, a single theft, accident, or equipment failure can derail your projects and drain your finances.

Idaho contractor equipment coverage exists to prevent exactly this scenario. At Matt Anderson Insurance, we help contractors like you understand what protection options are available and how to choose the right coverage for your specific needs.

Why Equipment Protection Matters for Idaho Contractors

Theft Targets Your Most Valuable Assets

Theft on Idaho job sites is a real problem. Rural and remote locations create prime conditions for equipment theft because many contractors store tools and machinery in unsecured areas overnight. Thieves know that excavators, skid steers, and generators sell quickly, and they target these assets regularly. A single stolen piece of heavy equipment costs $10,000 to $50,000 or more to replace, depending on the machinery.

Without coverage, that loss comes directly from your business bank account and forces you to delay or cancel projects.

Vandalism and Accidents Disable Your Operations

Vandalism adds another layer of risk-broken windows, slashed hydraulic lines, and intentional damage happen frequently on construction sites, especially in areas with high overnight exposure. Equipment damage from accidents compounds the problem. A dropped excavator bucket, collision between machinery, or operator error disables equipment for weeks while repairs happen. During that downtime, you cannot complete jobs, your crew sits idle, and your clients grow frustrated.

Standard Business Insurance Leaves Critical Gaps

Your general liability policy protects against third-party injuries and property damage claims, not your own equipment losses. If your equipment is stolen, damaged, or breaks down, that policy pays nothing. Many contractors don’t realize that standard business property insurance excludes mobile equipment and machinery, leaving them completely unprotected when these incidents occur.

Mechanical Failures Strike Without Warning

Equipment breakdown coverage specifically addresses mechanical failures-compressor failures, engine problems, hydraulic system malfunctions-that can happen without warning. Cold weather can affect machinery and tools, making them more prone to malfunction. On-site storage creates vulnerability because equipment left at job sites overnight faces theft, weather damage, and vandalism. Equipment in transit between jobs also needs protection; moving machinery across Idaho’s roads exposes it to collision damage and accidents.

Multi-Location Protection Prevents Exposure Gaps

Coverage that protects equipment both on-site and during transport keeps you protected throughout your entire operation. Without this layered protection, a single incident eliminates your profit margin for months and forces you to spend capital reserves on emergency replacements instead of growing your business. Understanding what types of equipment coverage exist helps you identify the right solutions for your specific contracting operation.

Equipment Coverage Types for Idaho Contractors

Inland Marine Insurance Protects Mobile Equipment

Inland marine insurance stands as the strongest option for protecting mobile equipment that moves between job sites. This coverage specifically addresses what standard property policies exclude-machinery in transit, stored at remote locations, and used across multiple project areas. Inland marine covers excavators, skid steers, bulldozers, backhoes, track loaders, compactors, trenchers, and directional drills against theft, vandalism, damage caused by fire, accidents, and natural disasters like floods or lightning.

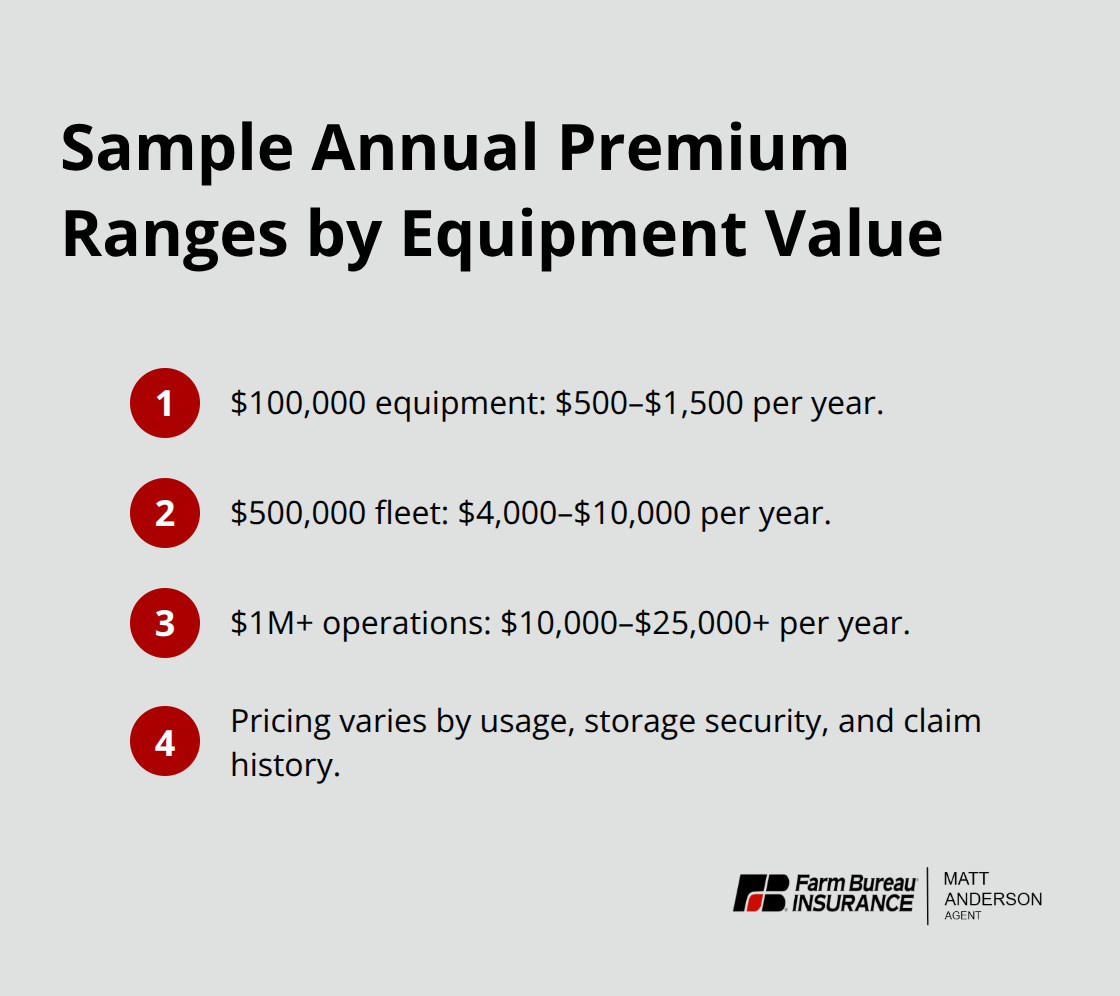

Annual costs vary based on equipment value and fleet size. For a $100,000 equipment value, you’ll pay $500 to $1,500 annually. A $500,000 fleet runs $4,000 to $10,000 per year, while $1 million-plus operations pay $10,000 to $25,000 or higher. These estimates depend on usage patterns, storage security, and claim history.

Inland marine also covers rented or borrowed equipment, which matters when you lease machinery for specific projects.

GPS tracking and secure storage in locked yards reduce your premiums significantly compared to leaving assets exposed at open job sites. The investment in security measures pays dividends through lower insurance costs and reduced theft risk.

Builder’s Risk Insurance Covers Construction Projects

Builder’s risk insurance protects materials and equipment during construction and renovation projects, covering on-site property losses and financial impacts from delays. Standard coverage includes framing, cleanup, and debris removal, with protection against fire, flood, theft, and weather damage. You can customize timeframes for new construction, remodeling, or rehabilitation work, and the policy extends to temporary structures like project trailers.

Add-ons cover penalties or unexpected costs tied to project disruption. Idaho’s winter conditions and spring thaw create genuine performance risks that influence both coverage needs and pricing. Working with a local Idaho specialist ensures your coverage aligns with regional climate risks, construction practices, and seasonal hazards specific to your operation.

Equipment Breakdown Coverage Prevents Costly Downtime

Equipment breakdown coverage addresses mechanical failures that happen without warning-compressor failures, engine problems, hydraulic system malfunctions. This coverage reimburses repair or replacement costs when machinery stops working, which prevents the costly downtime that forces you to rent replacements or disappoint clients.

Higher deductibles lower your annual premiums, but they increase your out-of-pocket costs when claims occur. Evaluate this trade-off based on your cash flow and risk tolerance. The right balance between premium savings and manageable deductibles depends on your specific business situation and equipment replacement capacity.

Understanding these three coverage types gives you the foundation to assess your protection needs. The next step involves taking inventory of your equipment and determining which coverage options align with your contracting operation’s size, scope, and risk profile.

Choosing Equipment Coverage That Matches Your Operation

Create a Complete Equipment Inventory

Start with a complete equipment inventory-this step is non-negotiable. List every piece of machinery and tools your business owns, including excavators, skid steers, generators, compressors, hand tools, and anything else that generates revenue for your contracting work. Assign a realistic replacement cost to each item based on current market prices, not what you paid five years ago. Equipment values matter because they directly determine your insurance premiums and coverage limits.

A $100,000 fleet costs far less to insure than a $500,000 operation, and undervaluing your assets creates a critical gap when you file a claim. Many contractors underestimate replacement costs and discover too late that their equipment coverage limits don’t match actual losses. Document everything with photos and serial numbers, which speeds up claims and proves ownership if theft occurs.

Assess Your Storage and Transportation Practices

Next, assess where your equipment sits and moves. Equipment stored in a locked, secured yard costs less to insure than machinery left exposed at open job sites. Equipment transported frequently between jobs faces different risks than stationary tools stored in a shop. Remote job sites in northern Idaho carry higher theft risk than urban Boise locations, which affects your premium pricing.

Insurers ask detailed questions about security measures, and misrepresenting your setup can lead to claim denials. Honest answers about your storage practices help underwriters price your coverage accurately and ensure you have adequate protection when incidents occur.

Balance Coverage Limits Against Deductibles

Coverage limits and deductibles create a direct trade-off between monthly costs and out-of-pocket expenses when problems happen. Raising your deductible from $500 to $2,500 lowers your annual premium noticeably, but you absorb the first $2,500 of every claim yourself. For contractors with strong cash flow and older equipment, higher deductibles make financial sense.

For operations running tight margins or relying on financed machinery, lower deductibles protect against unexpected repair bills that could disrupt operations. Don’t chase the lowest premium price alone-evaluate what you can actually afford to pay out of pocket when a loss occurs.

Compare Quotes from Multiple Providers

Compare what three different insurance providers offer for the same equipment and coverage type. Get detailed quotes that specify exactly what’s covered, what’s excluded, and what endorsements cost extra for high-value items. Some providers specialize in contractor equipment and understand Idaho-specific risks like winter weather damage and rural storage challenges, while generalist insurers apply one-size-fits-all pricing that misses your actual exposure.

The quote process typically takes one to three business days, so request multiple quotes simultaneously to compare side by side. Ask each provider how GPS tracking or security improvements reduce your premiums, because implementing theft prevention often lowers costs enough to pay for itself within a year.

Final Thoughts

Equipment protection isn’t optional for Idaho contractors-it’s a business necessity. The three coverage types we’ve covered address the real threats your operation faces daily: theft from remote job sites, vandalism, mechanical failures, and transport accidents happen regularly in Idaho, and standard business policies leave you completely exposed when they occur. Your next step is straightforward: pull together your equipment inventory with current replacement values, document your storage and transportation practices honestly, and decide what deductible level works for your cash flow situation.

Request quotes from multiple providers who understand Idaho contractor equipment coverage specifically, and don’t settle for generic quotes from insurers who treat your excavators the same way they treat office furniture. The quote process takes just a few days, and comparing three different options reveals significant price differences and coverage variations. Some providers offer discounts for GPS tracking or security improvements that pay for themselves through lower premiums, while others bundle equipment coverage with your general liability and workers’ compensation policies to create savings you won’t find buying policies separately.

We at Matt Anderson Insurance understand Idaho contractors and the specific risks your equipment faces. Contact us today to discuss your equipment coverage needs and get a quote that reflects your actual operation, because your equipment protects your livelihood, and your insurance should protect your equipment without gaps or surprises.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.