Idaho Contractor Workers Compensation: Keeping Your Team Protected

Running a contracting business in Idaho means managing multiple risks, and one of the biggest is protecting your workers when injuries happen on the job. Idaho contractor workers compensation insurance isn’t optional-it’s a legal requirement that shields both your team and your business from financial disaster.

At Matt Anderson Insurance, we help contractors understand their coverage options so they can make informed decisions. The right policy keeps your employees protected and gives you peace of mind.

Why Contractors Need Workers Compensation Coverage

Idaho law requires workers compensation coverage the moment you hire your first employee, including part-time and occasional workers. Operating without it is a misdemeanor that can result in criminal charges, fines, and potential jail time. The state takes this seriously because the financial consequences of an uninsured injury are catastrophic. If an employee gets hurt without coverage, you face liability for all medical expenses, recovery costs, and lost wages-costs that can easily exceed $100,000 for a serious injury. Idaho sets minimum coverage limits at $100,000 per occurrence for bodily injury and $100,000 per employee for bodily disease, though contractors in high-risk trades typically need higher limits to stay protected.

What Happens Without Coverage

The penalties extend far beyond fines. An injured worker without compensation coverage can sue you directly for damages, and you’ll have no insurance to back the claim. You could lose your business, your personal assets, and face wage garnishment. Misclassifying workers as independent contractors to avoid coverage is a serious violation with its own set of legal consequences. Beyond legal trouble, an uninsured injury devastates your team. Workers lose income during recovery while you lose productivity, and the stress of an unsupported injured worker often leads to retention problems. The damage to your reputation in Idaho’s contractor community spreads fast when word gets out that you don’t protect your team.

Medical Care and Wage Replacement

Workers compensation in Idaho covers immediate medical care-ambulance, emergency room visits, x-rays, surgery, and prescription medications-plus ongoing treatment like physical therapy for chronic injuries. Wage replacement typically covers about two-thirds of lost wages during recovery, which helps your injured worker stay afloat financially while you avoid the liability. Death benefits and funeral costs go to the worker’s family, protecting them from financial ruin.

Your Coverage Options in Idaho

You can choose from multiple paths: private insurance through licensed carriers, the Idaho State Insurance Fund as a backup option, the assigned risk pool for difficult-to-insure operations, or self-insurance if you meet payroll thresholds. An independent agent shops multiple carriers side-by-side, which matters because premiums vary significantly based on your industry risk, payroll size, and worker classifications. The right agent understands contractor operations and helps you find the right carrier without overpaying for coverage you don’t need.

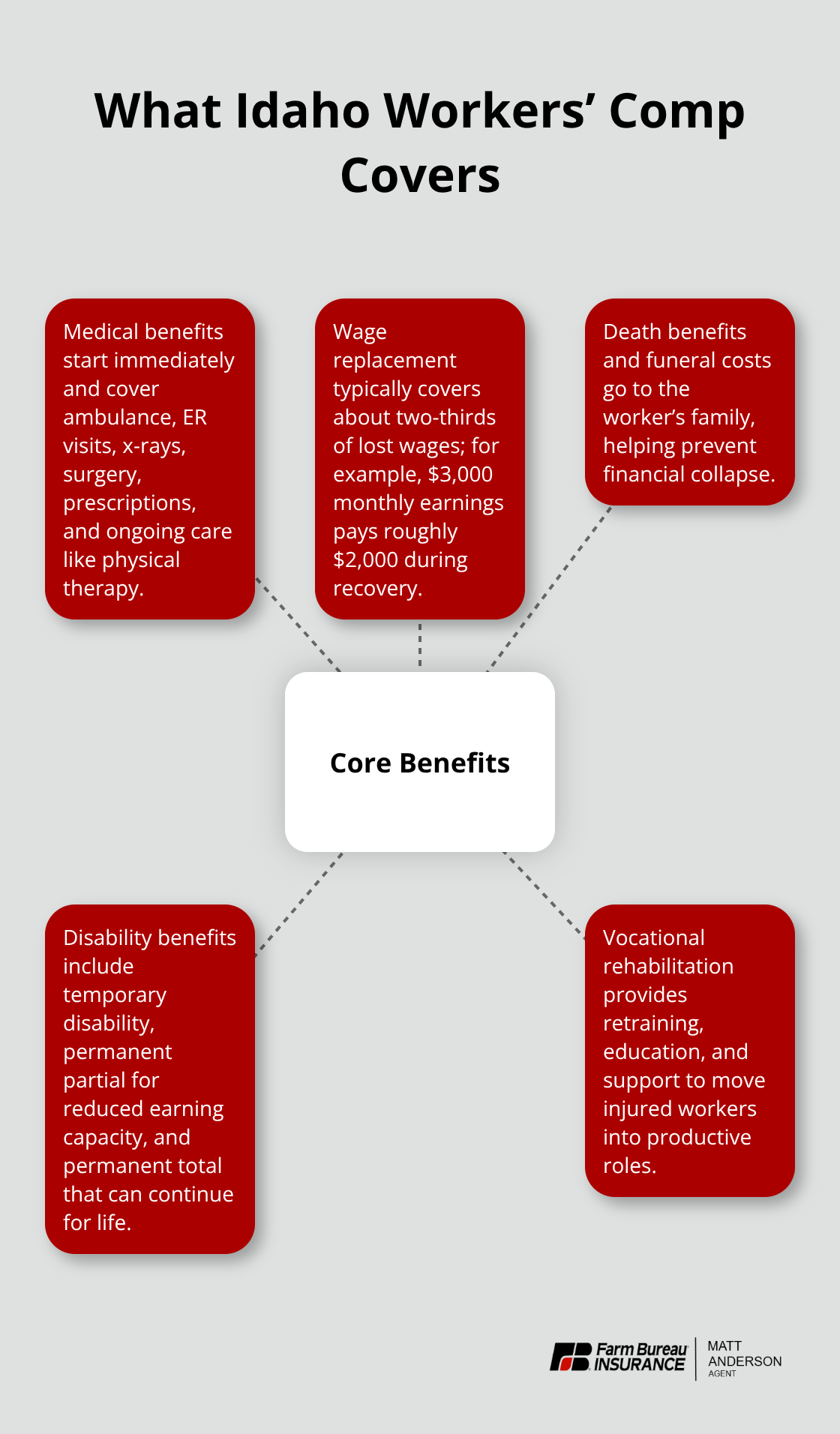

What Your Idaho Workers Compensation Policy Actually Covers

Idaho workers compensation covers far more than just emergency room visits, and understanding exactly what your policy includes prevents nasty surprises when an injury happens. Medical benefits start immediately and include ambulance services, emergency room treatment, x-rays, surgery, and prescription medications. Ongoing care matters just as much as initial treatment-physical therapy for a construction worker’s back injury or chronic condition management for repetitive stress damage stays covered throughout recovery. Wage replacement typically covers approximately two-thirds of lost wages, which means an employee earning $3,000 monthly receives roughly $2,000 while unable to work. This partial income replacement keeps your injured worker financially stable and reduces the desperation that leads to rushed returns to work before full recovery. If a worker dies from a job-related injury, death benefits and funeral costs go directly to their family or beneficiaries, protecting them from financial collapse.

Disability Benefits Address Both Temporary and Permanent Injuries

Temporary disability covers the immediate period when an employee cannot work, but Idaho’s system also addresses permanent disabilities. Permanent partial disability applies when an injury causes lasting impairment that affects earning capacity-a roofer with a permanent knee injury that prevents climbing ladders receives compensation reflecting that reduced ability. Permanent total disability applies to severe injuries that prevent any gainful employment, and these benefits continue for life.

Vocational Rehabilitation Moves Workers Back Into Productive Roles

Vocational rehabilitation services help injured workers transition back to work when they cannot return to their original job. A worker with a permanent hand injury receives training for a different trade, with the employer’s insurance covering education costs, training supplies, and related expenses. This service protects both the worker and your bottom line by moving someone from permanent disability payments into productive employment.

Coverage Limits Matter for Your Contractor Operation

Idaho sets minimum coverage limits at $100,000 per occurrence for bodily injury and $100,000 per employee for bodily disease, though contractors in high-risk trades typically need higher limits to stay protected. A serious injury in roofing, excavation, or heavy equipment operation can exceed these minimums quickly, leaving you exposed if your policy falls short. Assess your specific risks with an independent agent who understands contractor operations and can recommend appropriate limits for your trade.

The right coverage means your injured workers receive the support they need while you avoid the catastrophic costs of uninsured claims. Understanding these benefits helps you choose a policy that actually protects your operation when injuries happen.

Selecting the Right Policy for Your Contractor Operation

Choosing a workers compensation policy requires matching your actual business structure to the coverage you buy, not the other way around. Many Idaho contractors overpay because they select limits based on state minimums rather than their specific risk profile. An excavation contractor working with heavy machinery needs dramatically different coverage than a painting crew, yet both often settle for the $100,000 per occurrence minimum that Idaho requires.

Document Your Workforce and Job Classifications

Start with your workforce composition in detail: how many full-time employees you carry, how many seasonal or occasional workers you bring on, and which job classifications your team performs. The Idaho Industrial Commission tracks workers compensation rates by industry classification, and your premium reflects this directly. A roofer costs significantly more to insure than an office administrator because roof work carries higher injury frequency and severity. Misclassifying workers to lower your premium creates legal exposure that dwarfs any savings. If you classify a laborer as an independent contractor to avoid coverage, and that worker gets injured, Idaho’s right-to-control test examines whether you directed their work, set their hours, provided equipment, and controlled the means of production. If those factors point to employment, you face liability for the injury plus penalties for misclassification.

Match Coverage Limits to Your Actual Risk

Your coverage limits should reflect your actual risk exposure, not regulatory minimums. A serious fall from scaffolding or a crushing injury from equipment can generate medical bills exceeding $250,000 before accounting for permanent disability payments. Talk with an independent agent who works across multiple Idaho carriers rather than accepting one company’s standard products. That agent shops your operation against carriers who specialize in your trade, securing better rates and appropriate limits. Beyond workers compensation, contractor liability insurance shields your business from third-party injury and property damage claims that workers compensation doesn’t cover.

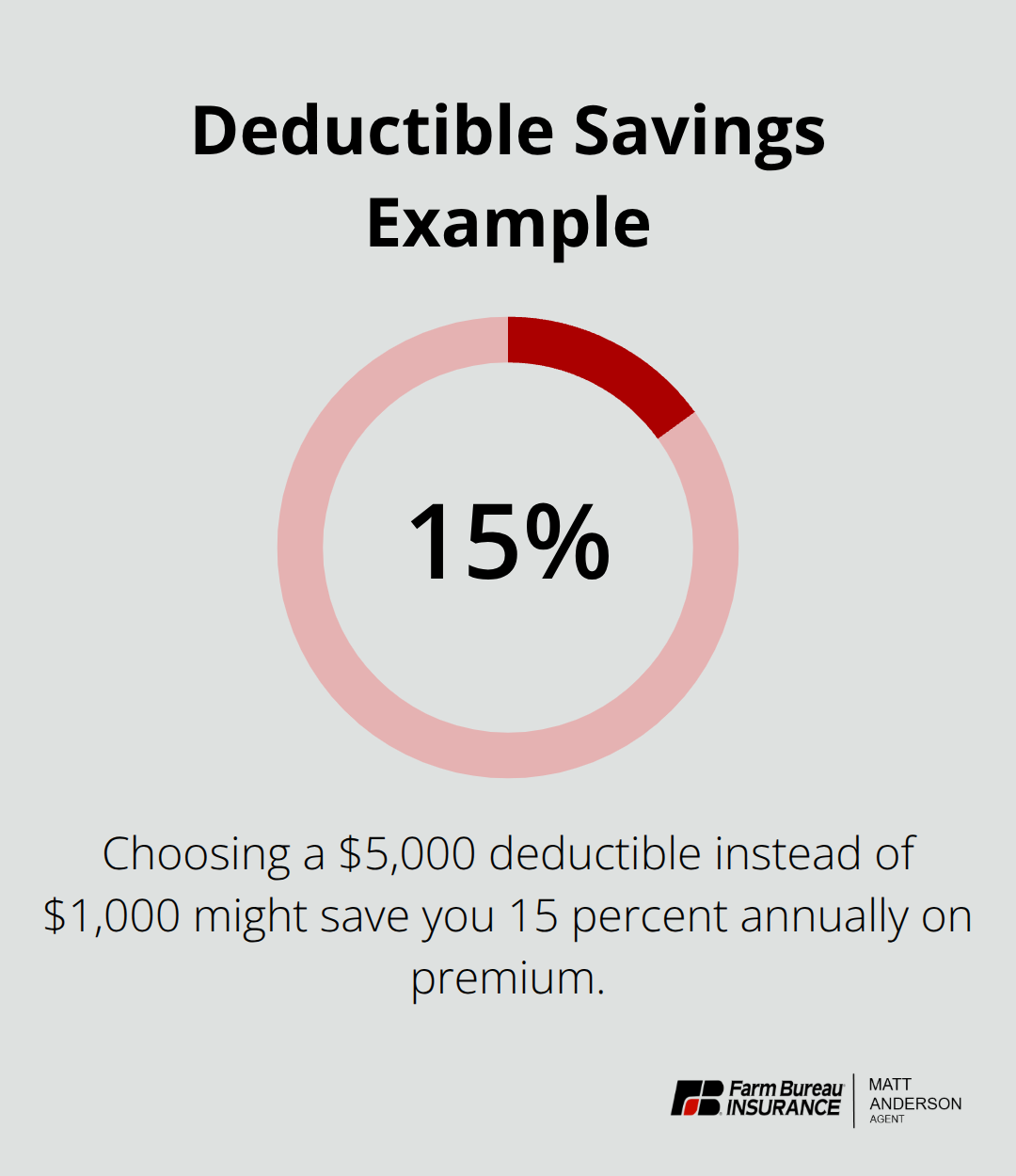

Evaluate Deductibles Against Your Cash Flow

Deductibles matter more than most contractors realize because they reduce your premium but increase your out-of-pocket exposure on each claim. A $1,000 deductible versus a $5,000 deductible might save you 15 percent annually, but a single serious injury costs you that deductible amount immediately. An independent agent familiar with Idaho contractor operations understands which deductible levels work for your cash flow and claims frequency.

Use Experience Modification Ratings to Drive Better Rates

Experience modification ratings, called mods, function like a credit score for workers compensation. After three years of premium payments, your mod reflects your safety record and claims history. A favorable mod cuts your rates substantially, while a poor mod raises them significantly. This creates financial incentive to invest in genuine safety practices rather than just compliance paperwork. An agent who helps you track safety performance uses that data to shop better rates annually as your mod improves.

Final Thoughts

Idaho contractor workers compensation protects your team when injuries happen and keeps your business operating legally. Without proper coverage, you face criminal penalties, devastating financial liability, and the knowledge that your workers lack support during their most vulnerable moments. The right policy eliminates that risk entirely and gives you peace of mind.

Your specific operation determines what coverage you actually need. Your workforce size, job classifications, industry risk, and injury exposure shape the limits and deductibles that work for your business rather than forcing you into a standard product. An independent agent who understands contractor operations matches your policy to your actual risks instead of settling for state minimums.

Contact an independent agent today to document your workforce, assess your injury risk honestly, and shop multiple carriers on your behalf. That agent handles the paperwork, explains your options clearly, and manages your policy as your business grows. We at Matt Anderson Insurance work with multiple carriers to find the right coverage for your Idaho contractor workers compensation needs without overpaying for protection you don’t need.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.