Idaho Vacation Home Insurance: Coverage For Your Seasonal Getaway

Owning a vacation home in Idaho comes with unique insurance needs that standard homeowners policies simply don’t cover. Your seasonal getaway requires specialized protection tailored to part-time occupancy, guest liability, and seasonal risks.

At Matt Anderson Insurance, we help Idaho property owners understand exactly what Idaho vacation home insurance should include. Let’s walk through your coverage options and show you how to protect your investment without overspending.

What Vacation Home Insurance Actually Covers

Vacation home insurance differs fundamentally from standard homeowners coverage because it accounts for part-time occupancy and guest interactions. This type of policy protects the structure of your seasonal property, your personal belongings inside it, and your liability if a guest gets injured or their belongings are damaged while staying with you. Standard homeowners policies assume you occupy the home year-round and often exclude or severely limit coverage for properties you don’t live in full-time. Many insurers will outright deny claims if they discover your home sits vacant for extended periods-exactly what happens with seasonal properties.

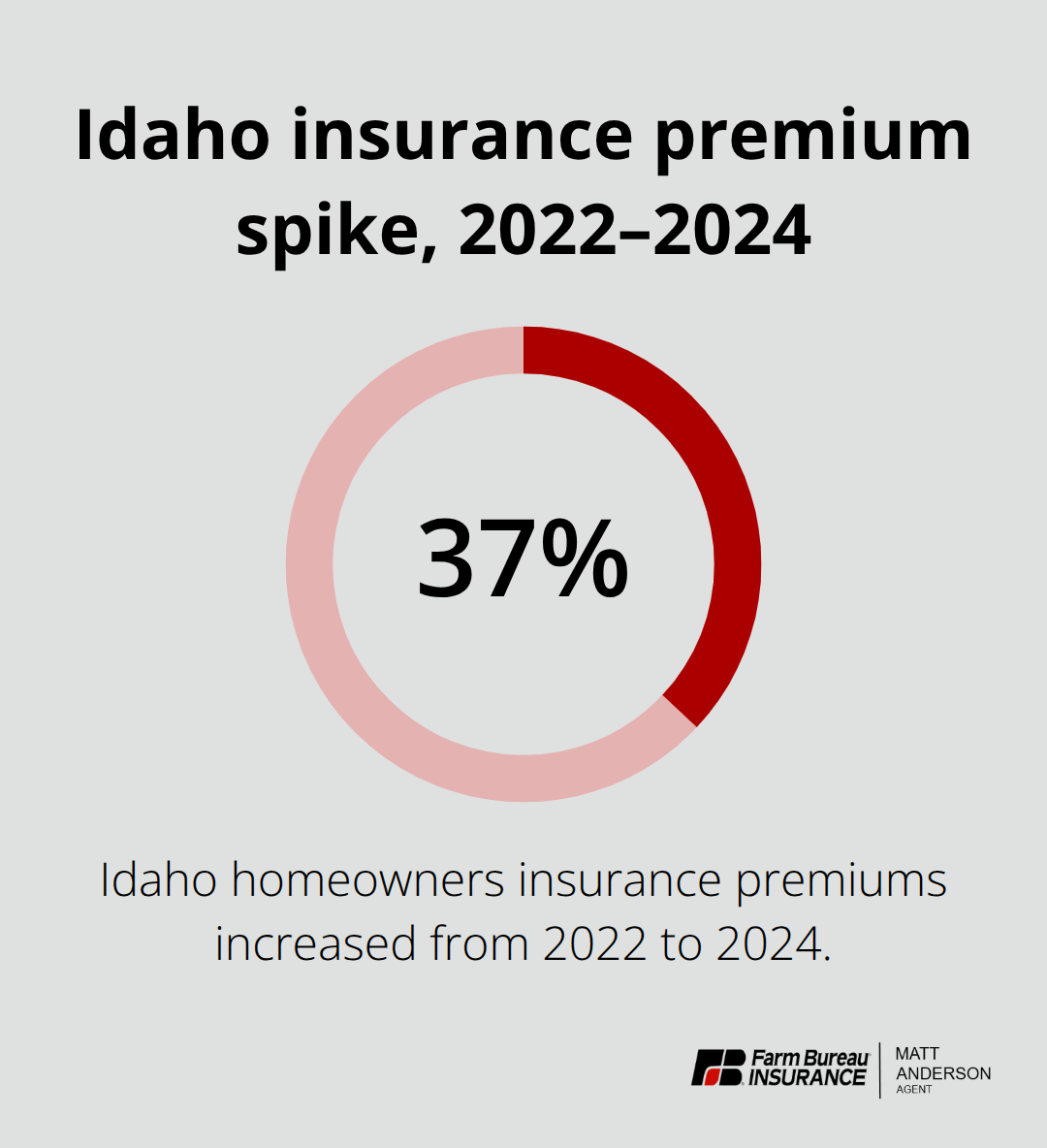

Idaho homeowners insurance premiums rose 37 percent from 2022 to 2024, making it critical to obtain the right coverage the first time rather than discovering gaps after a loss.

Why Your Current Homeowners Policy Won’t Protect Your Seasonal Home

Standard homeowners policies contain explicit exclusions for non-owner-occupied properties and business use. If you rent out your vacation home on Airbnb or Vrbo, your regular homeowners insurance will not cover guest-related incidents, theft by guests, or damage during rental periods. The platforms themselves offer some host protection, but these limits are typically low and loaded with exclusions. Landlord policies designed for long-term rentals won’t work either because they’re structured for properties where tenants occupy the home continuously under lease agreements. Idaho vacation home owners face additional pressure from the state’s wildfire risk and rising construction costs, which means rebuilding costs are substantially higher if disaster strikes, and standard policies may not provide enough coverage to actually rebuild your property.

How Vacation Home Coverage Protects Your Financial Investment

A proper vacation home policy covers dwelling damage from named perils like fire, lightning, and theft, plus liability protection when guests are injured on your property. Loss of income coverage is included in many vacation home policies, meaning if a covered claim makes the property temporarily uninhabitable or unrentable, you receive compensation for the rental income you lose during that period. This matters significantly in Idaho’s seasonal markets where summer and holiday weeks generate the bulk of annual rental income. Dwelling coverage typically uses replacement cost rather than actual cash value, meaning the insurer pays what it costs to rebuild today rather than depreciating the structure’s value. You should also confirm that your policy covers the property during vacancy periods because Idaho vacation homes sit empty for months at a time, and many standard policies void coverage when a home is unoccupied beyond a certain threshold.

What Happens When You Choose the Wrong Policy

Selecting an inadequate policy can leave you exposed to significant financial loss. A policy that doesn’t account for your rental activity won’t protect you if a guest causes damage or suffers an injury on your property. Policies with low liability limits may not cover serious guest injuries, leaving you personally liable for medical bills and legal costs. Additionally, policies that exclude loss of income coverage mean you absorb all revenue loss if the property becomes temporarily unrentable due to a covered claim. The cost of vacation home insurance varies by location, building construction type, fire risk, natural disasters, crime, and unique features of the property, so a policy that works for a friend’s vacation home in McCall may not work for your property in Coeur d’Alene. Understanding these differences upfront prevents costly coverage gaps later.

Getting Coverage That Matches Your Seasonal Use

A local Idaho agency understands seasonal occupancy patterns and can align your coverage with your actual usage, not generic assumptions about how you use the property. Your agent should ask specific questions about how many months you occupy the home, whether you rent it out, what amenities you provide to guests, and what natural disaster risks apply to your location. This conversation determines whether you need additional endorsements for specific exposures and helps you avoid overpaying for coverage you don’t need. The right policy protects your structure, your belongings, and your liability exposure while accounting for the months when your seasonal home sits empty. With these fundamentals in place, you’re ready to explore the specific coverage options that fit your Idaho vacation property and budget.

What Coverage Do You Actually Need for Your Idaho Vacation Home

Dwelling and Personal Property Protection

Dwelling protection forms the foundation of any vacation home policy and covers the structure itself against named perils like fire, lightning, wind, and theft. In Idaho, replacement cost coverage matters far more than actual cash value. Replacement cost means the insurer pays what it costs to rebuild today, not a depreciated figure that leaves you short when disaster strikes. Your personal property inside the home-furniture, electronics, kitchen equipment-receives separate coverage with its own limit, usually between 50 and 70 percent of the dwelling limit.

If you store expensive items at your seasonal home like art, collectibles, or high-end outdoor equipment, verify these limits cover your actual belongings. Standard policies cap coverage on individual items like jewelry or electronics, so you may need additional endorsements for valuable possessions.

Liability Coverage for Guest Injuries

Liability coverage protects you when a guest is injured on your property or their belongings suffer damage during their stay. We recommend minimum limits of 300,000 dollars, though 500,000 dollars or higher makes sense given Idaho’s litigation environment and the potential for serious injuries. Most vacation home policies include medical payments coverage separate from liability, which covers minor guest injuries regardless of fault up to 1,000 or 5,000 dollars. This coverage helps you avoid small claims that could otherwise damage your rental reputation.

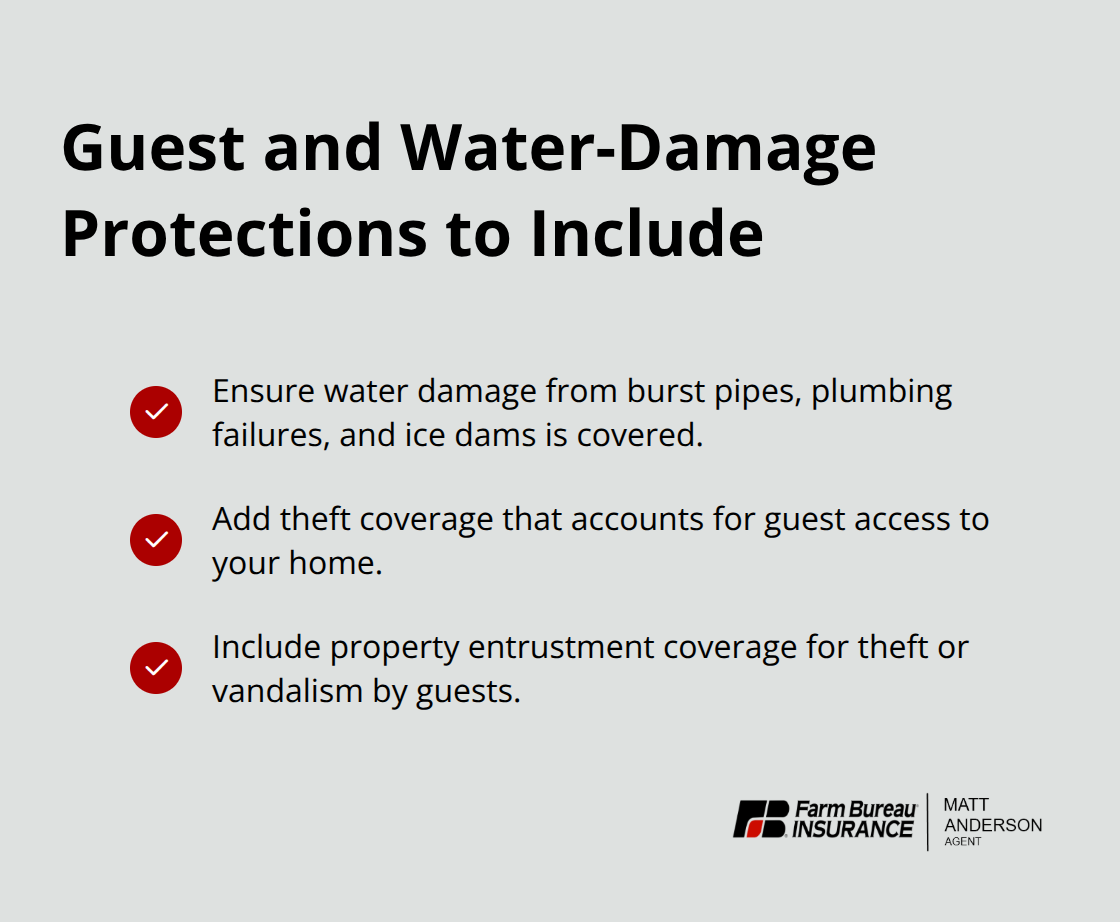

Water Damage, Theft, and Guest-Related Risks

Water damage from burst pipes, plumbing failures, or ice dam damage should be explicitly covered in your policy because standard homeowners policies often exclude or limit water damage claims. Theft coverage becomes critical when guests have access to your home, and property entrustment coverage specifically protects against theft or vandalism by guests-a gap many vacation home owners discover only after a loss.

Natural Disaster Coverage for Idaho Locations

Natural disaster coverage varies significantly by location within Idaho, so a property near the Snake River Plain faces wildfire exposure that requires explicit coverage or endorsements. Properties near rivers or floodplains need separate flood insurance through the National Flood Insurance Program (NFIP). Loss of use coverage compensates you for rental revenue lost when a covered claim makes the property temporarily uninhabitable. This protection proves essential in Idaho’s seasonal markets where summer bookings generate the majority of annual rental income.

Choosing the Right Coverage Limits

The specific coverage limits you select depend on your property’s replacement cost, the value of your personal belongings, your guest liability exposure, and your location’s natural disaster risks. A property in McCall with high wildfire exposure requires different endorsements than a property in Coeur d’Alene near water. Your agent should ask specific questions about how many months you occupy the home, whether you rent it out, what amenities you provide to guests, and what natural disaster risks apply to your location. This conversation determines whether you need additional endorsements for specific exposures and helps you avoid overpaying for coverage you don’t need. Once you understand what coverage protects your property and your liability, the next step involves evaluating how much you’ll actually pay for that protection and where you can reduce costs without sacrificing essential coverage.

How Bundling and Seasonal Adjustments Lower Your Vacation Home Costs

Multi-Policy Discounts That Add Up Fast

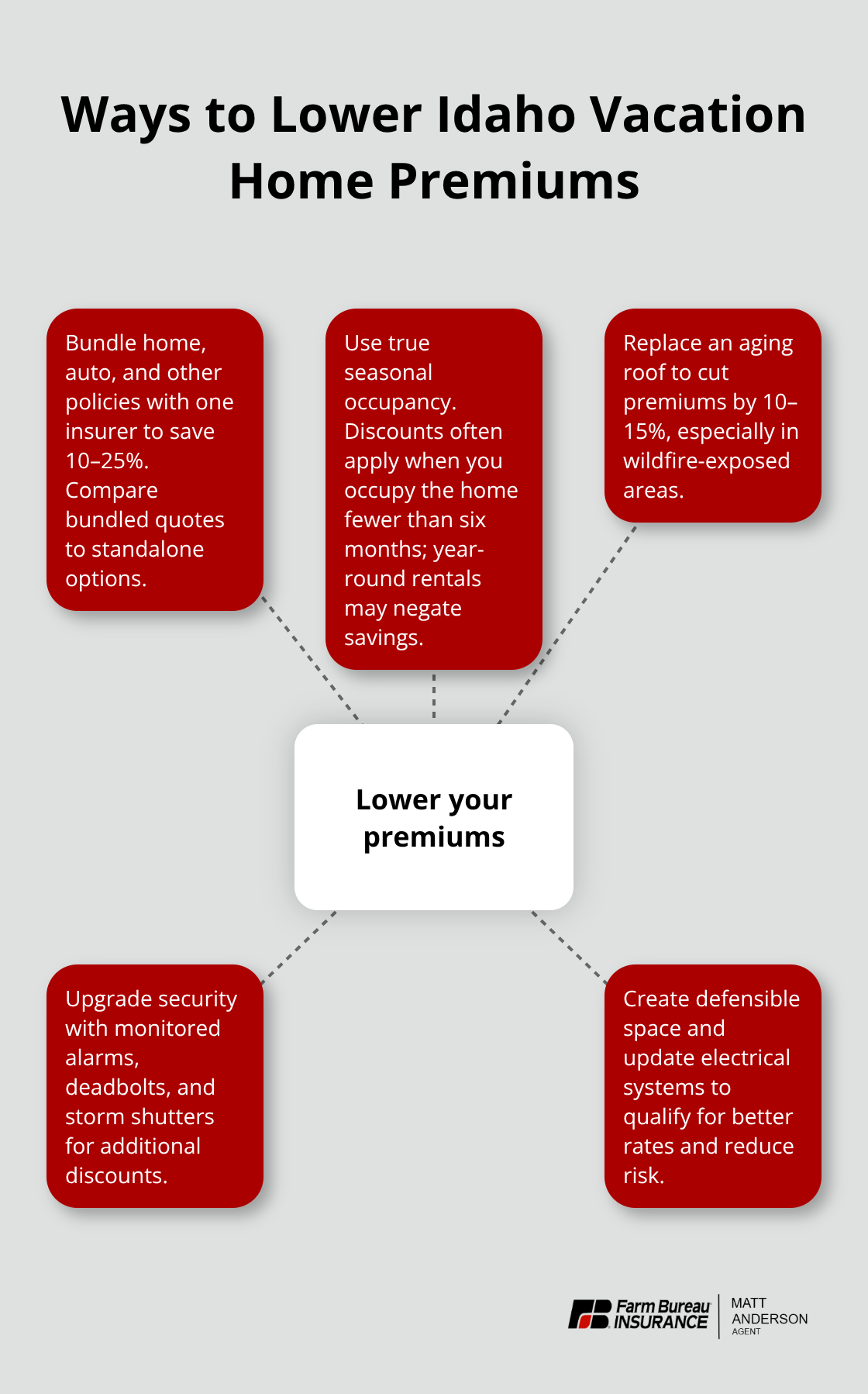

Bundling your vacation home policy with auto, home, or other coverage through one insurer typically saves 10 to 25 percent on your total premiums. This discount applies whether you insure your primary residence, your seasonal property, or both. The actual discount depends on which policies you combine and your insurer’s specific incentive structure, but most carriers reward customers who consolidate coverage rather than shopping policies separately. If you currently insure your primary home elsewhere, moving your vacation home coverage to that same insurer often qualifies you for a bundling discount on both policies. This strategy makes financial sense because the savings frequently exceed what you’d pay for a standalone vacation home policy at a different company. Start by requesting quotes that include bundled rates from your current homeowners insurer, then compare those against standalone vacation home quotes to see which approach saves more money.

How Seasonal Usage Patterns Affect Your Premium

Seasonal usage patterns directly affect what you pay because insurers charge lower premiums for properties you occupy only part of the year compared to full-time residences. Properties occupied fewer than six months typically qualify for seasonal discounts, though the exact threshold varies by insurer. However, this discount only applies if your property actually sits vacant during off-season months; if you rent it out year-round, the insurer may charge standard rates or higher.

Understanding your specific occupancy pattern helps you select the right policy tier and avoid overpaying for coverage that assumes year-round use.

Loss-Prevention Measures That Cut Premiums Substantially

Implementing specific loss-prevention measures cuts your premium substantially more than seasonal discounts alone. Installing a new roof can reduce premiums by 10 to 15 percent because it lowers fire risk, which matters enormously in Idaho’s wildfire zones. Adding deadbolts, upgrading to a monitored security system, or installing storm shutters all generate measurable discounts that compound when combined. Properties with updated electrical systems, fire extinguishers, and clear defensible space around the structure also qualify for better rates.

Prioritizing Home Improvements for Maximum Savings

Ask your agent specifically which improvements your property needs to qualify for the largest available discounts. Prioritize the upgrades with the fastest payback period against your annual premium savings (this approach ensures you recoup your investment quickly through lower premiums). Some improvements, like clearing vegetation within 30 feet of your home, cost little but yield significant discounts in high-wildfire areas. Others, like roof replacement, require substantial upfront investment but deliver long-term savings that justify the expense over several years.

Final Thoughts

Protecting your Idaho vacation home requires specialized coverage that accounts for part-time occupancy, guest liability, and the wildfire and natural disaster risks specific to your location. Standard homeowners policies simply won’t cover seasonal use, and forcing one to fit your situation leaves you exposed to significant financial loss when a claim occurs. Idaho vacation home insurance designed for your actual usage pattern protects your structure, belongings, liability exposure, and rental income far more effectively than hoping a generic policy will work.

Bundling your vacation home policy with auto or primary home coverage saves 10 to 25 percent on premiums, while loss-prevention measures like roof upgrades or defensible space clearing cut costs even further. Local Idaho agents understand which natural disaster risks apply to your specific location and can explain why premiums have risen 37 percent since 2022 without overselling coverage you don’t need. An agent familiar with your region helps you navigate options that actually fit your property rather than forcing you into a one-size-fits-all approach.

Contact Matt Anderson Insurance to discuss your seasonal property needs and see how we can build coverage that protects your investment while keeping your premiums reasonable. Getting a quote takes minutes and costs nothing, and our licensed agents handle the details so you understand exactly what your policy covers and why those limits matter for your property.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.