Idaho Home Insurance Discounts: How Much Can You Save?

Idaho homeowners typically leave money on the table when it comes to their insurance premiums. Most policies qualify for multiple discounts that can significantly reduce what you pay each month.

At Matt Anderson Insurance, we’ve helped countless Idaho residents find substantial savings by understanding which discounts apply to their specific situation. This guide walks you through the discounts available and shows you exactly how to claim them.

What Discounts Actually Reduce Your Idaho Home Insurance Bill

Idaho homeowners can cut their premiums significantly through discounts, but most people only know about bundling. Insurers offer far more savings opportunities than most realize. Discounts can reduce your premiums, and when you combine multiple discounts, the total savings compound. The key is understanding which discounts you actually qualify for and which ones matter most for your situation.

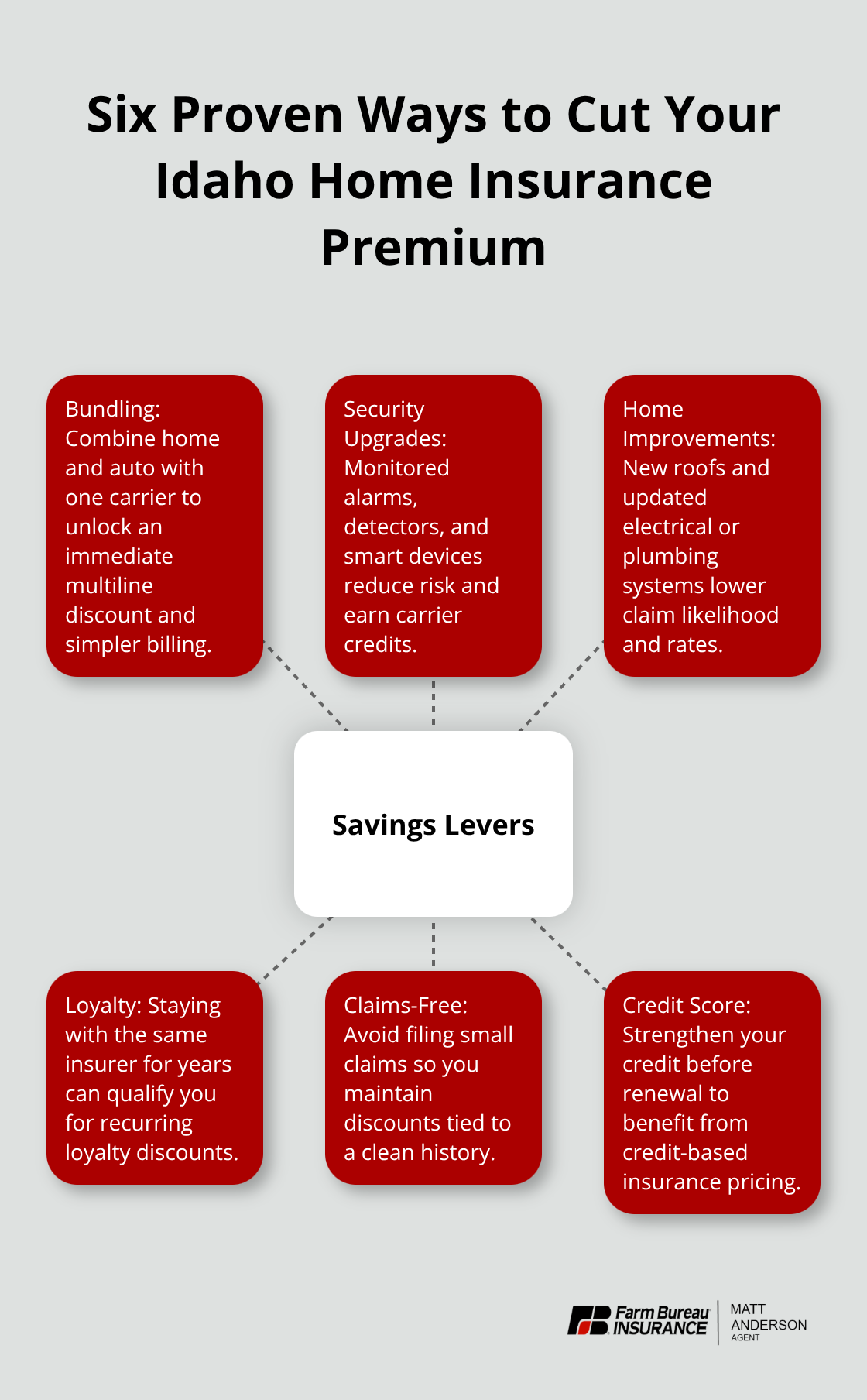

Bundling Delivers the Biggest Savings

Bundling home and auto policies stands out as the single most valuable move you can make. If you pay for home and auto separately, you overpay. This strategy simplifies your billing and renewals by consolidating policies with one carrier, which also makes managing your coverage easier.

Security Devices and Smart Home Technology

Beyond bundling, security devices make a real difference. Monitored alarm systems, fire detectors, and smoke alarms reduce your premium according to industry standards. Smart home technology like water leak detectors and remote video surveillance also qualifies for discounts. A deadbolt lock or reinforced doors trigger additional savings. These aren’t theoretical reductions-they reflect actual risk reduction that insurers reward with lower rates.

Home Improvements That Pay Back

New roofs and upgraded electrical or plumbing systems lower your premiums because they reduce the likelihood of costly claims. A new roof, especially with impact-resistant materials, delivers measurable savings by cutting storm damage risk. Upgrading your electrical system to modern standards reduces fire risk and qualifies for discounts. Modern plumbing systems prevent water damage claims that can cost thousands. Roof age matters significantly; if your roof approaches the end of its lifespan, replacement cuts your rates going forward. Storm shutters or reinforced windows also reduce risk and lower your rates.

Discounts Most Homeowners Miss

Loyalty discounts apply if you stay with the same insurer for several years, yet many customers never ask about them. Claims-free discounts reward you for not filing claims over a set period. New home construction discounts apply if your home was recently built or substantially renovated. If you’ve recently made improvements, contact your agent and ask about rate reductions. Your credit score influences your rate in Idaho, so improving your credit score lowers premiums at renewal.

The discounts available to you depend on your specific home, location, and personal profile. Understanding which ones apply to your situation requires a closer look at your current coverage and what protections you actually need.

How Bundling and Claims History Shape Your Savings

Bundling Delivers Immediate Savings

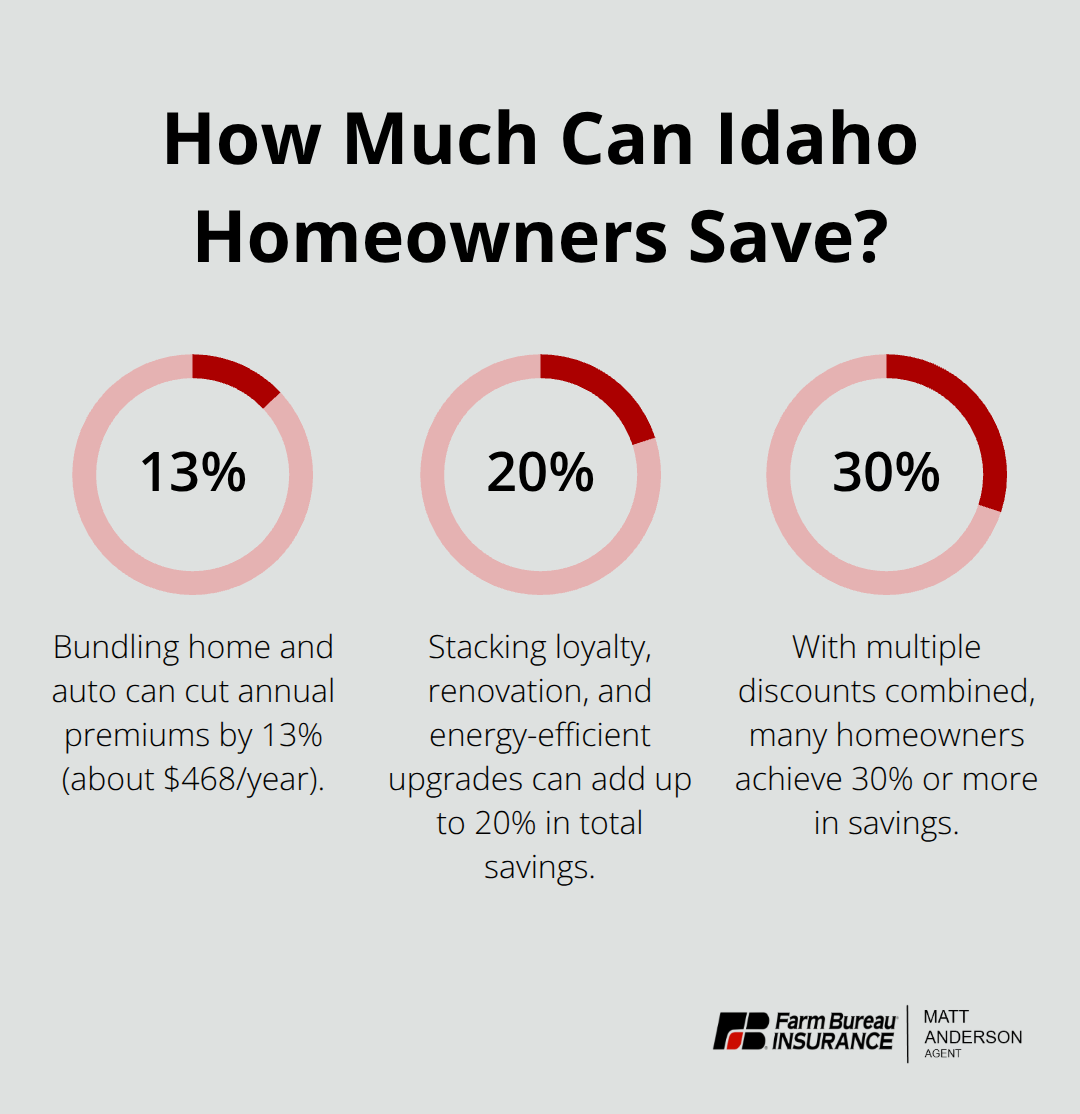

Combining your auto and home insurance with one carrier cuts your annual premiums by 13 percent, saving about $468 per year compared to purchasing separate policies. If you pay separate policies to different insurers, you lose hundreds each year. Insurers reward bundling because they manage your entire relationship, so they reduce rates substantially in exchange for your loyalty. Beyond the premium reduction, consolidating policies simplifies your life. You get one renewal date, one agent to contact, and one bill to track instead of juggling multiple carriers and payment schedules. This efficiency matters when you need to file a claim or update your coverage. Many Idaho homeowners see reductions of 300 to 950 dollars annually depending on their specific coverage and location.

Small Claims Cost More Than You Think

Your claims history directly impacts what you pay going forward, and this is where many homeowners make costly mistakes. Filing small claims for minor damage increases your premiums significantly, sometimes more than the claim payout itself. If your roof sustains wind damage costing 800 dollars and your deductible is 1000 dollars, filing a claim makes no financial sense and will raise your rates at renewal. Instead, pay out of pocket for minor incidents and reserve claims for major losses that truly warrant insurance intervention.

Building a Claims-Free Record

Homeowners who maintain a claims-free record for three to five years qualify for specific discounts that compound your savings. These discounts reward your restraint and demonstrate to insurers that you manage risk responsibly. The longer you go without filing a claim, the more valuable your discount becomes at renewal time.

Credit Score Matters More Than Most Realize

Your credit score in Idaho directly influences your rates through credit-based insurance scoring, so paying bills on time and reducing credit card balances at renewal time can lower your premiums without changing your coverage. These behavioral factors cost nothing to address but deliver measurable financial rewards when you stay disciplined about your finances. Improving your credit before renewal gives you leverage to negotiate better rates with your current insurer or shop for better quotes elsewhere.

Discounts You’re Probably Overlooking

Loyalty Rewards for Long-Term Customers

Most Idaho homeowners focus on bundling and miss three substantial discounts that can shave hundreds off annual premiums. Loyalty matters more than you think, and insurers actively reward customers who stay with them for years. If you’ve held your policy for three or more years without switching carriers, ask your agent directly whether you qualify for a loyalty discount. Some insurers apply this automatically, but many require you to request it at renewal. The discount typically ranges from ten to eighteen percent depending on your carrier and how long you’ve been a customer. This is free money you leave on the table if you don’t ask.

New Construction and Renovation Discounts

If your home was built or substantially renovated within the past five years, you qualify for a new construction discount that recognizes lower rebuild costs and modern building standards. Newer homes have updated electrical systems, plumbing, and roofing materials that reduce fire and water damage risk significantly. Homes built in 2015 or later typically qualify for these discounts automatically, but if you recently completed major renovations like a new roof, rewired electrical system, or upgraded plumbing, contact your agent and request a rate review. Renovation discounts can meaningfully lower your premiums when major systems are updated, so the investment in home improvements pays back through insurance savings.

Energy-Efficient Upgrades and Green Home Features

Energy-efficient upgrades and green home features represent the third major discount category that homeowners consistently overlook. Installing a modern HVAC system, upgrading to energy-efficient windows, or adding insulation doesn’t just reduce your utility bills-it also qualifies for insurance discounts because these improvements reduce overall home risk and rebuilding costs. Smart thermostats, LED lighting upgrades, and water heaters with modern safety features all signal to insurers that you maintain your home responsibly. If you’ve made any energy-related improvements in the past year, your agent needs to know. These upgrades often go undocumented during the initial application, which means you miss the discount at every renewal. Ask your agent to conduct a full review of your home’s current condition and any improvements you’ve made since you purchased the policy. The combination of loyalty recognition, new construction or renovation discounts, and energy-efficient upgrades can easily add up to twenty or thirty percent in total savings (money that compounds year after year if you maintain your coverage with the same carrier).

Final Thoughts

Idaho homeowners typically save between $300 and $950 annually by combining multiple discounts, yet most people claim only one or two. The real savings potential emerges when you stack bundling, security upgrades, claims discipline, and loyalty recognition together. A homeowner who bundles auto and home insurance, maintains a claims-free record, installs monitored security, and qualifies for loyalty discounts can reduce their annual premium by 30 percent or more.

Review your current policy and identify which discounts you already receive and which ones you’ve missed. Contact your agent and ask specifically about loyalty discounts, new construction or renovation credits, and energy-efficient upgrades you’ve made since purchasing your policy. Many homeowners discover they qualify for Idaho home insurance discounts they never claimed simply by asking, and if you haven’t bundled your auto and home insurance, that single move delivers immediate savings without changing your coverage.

We at Matt Anderson Insurance help Idaho families and businesses identify every discount available to them. Our licensed agents understand the specific discounts that apply in Idaho and work to maximize your savings while protecting what matters most. Reach out to Matt Anderson Insurance today to review your coverage and discover how much you can actually save.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.