Contractor Liability Insurance Idaho: Guarding Your Business From Claims

One accident on a job site can cost your business thousands of dollars in medical bills, legal fees, and settlements. Contractor liability insurance in Idaho protects you from these financial disasters.

At Matt Anderson Insurance, we’ve seen too many contractors operate without proper coverage and face devastating consequences. The right policy stands between your business and bankruptcy.

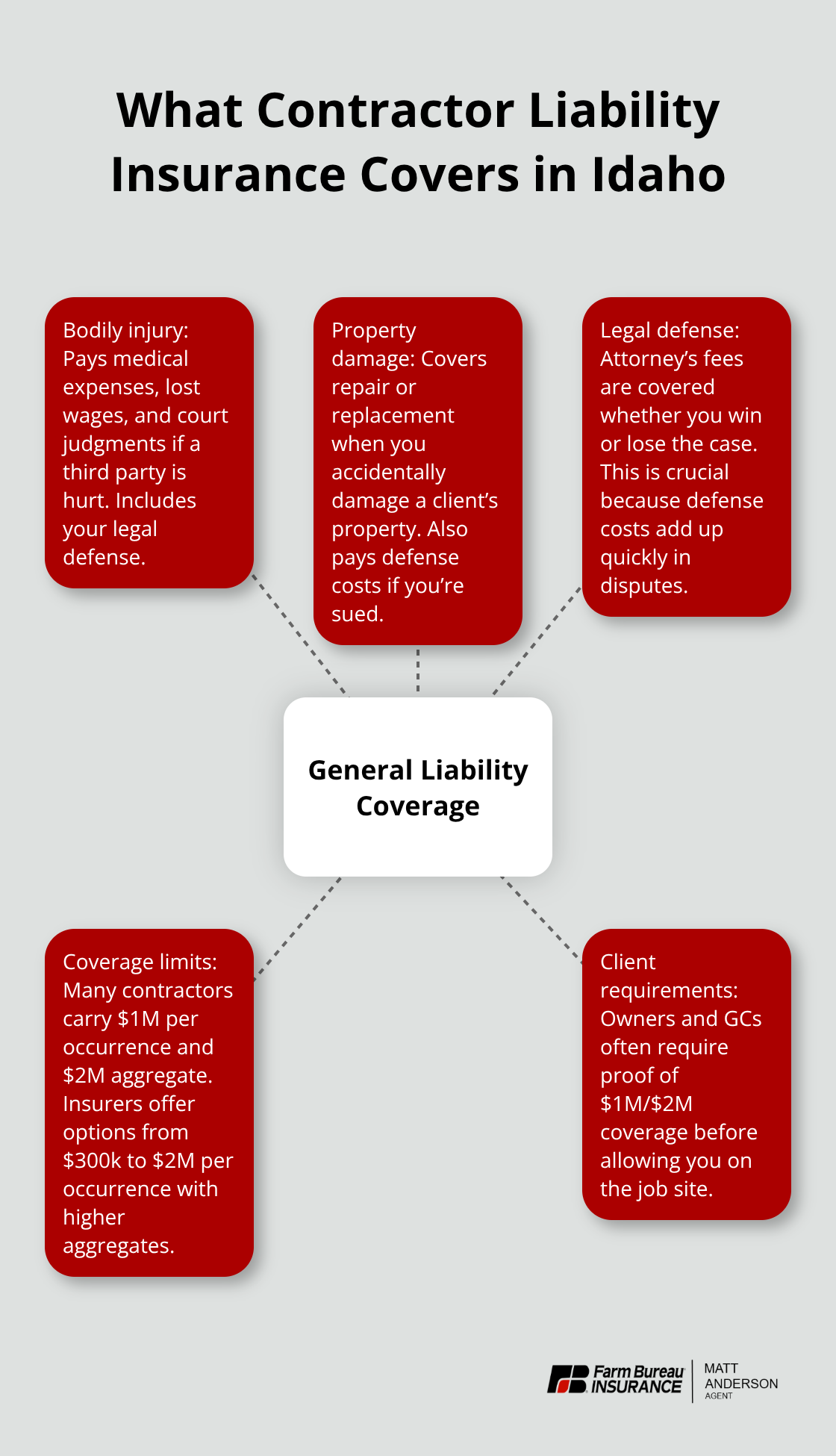

What Contractor Liability Insurance Actually Covers

Contractor liability insurance protects you when someone gets hurt or property gets damaged because of your work. General liability policies in Idaho typically cover bodily injury claims when a third party is injured on your job site or by your work, property damage claims when you accidentally damage a client’s building or belongings, and the legal defense costs if someone sues you. The Hartford, which MoneyGeek identified as the best general liability insurer in Idaho with rates starting around $77 per month, offers coverage limits ranging from $300,000 to $2 million per occurrence, with aggregate limits up to $4 million. Most Idaho contractors carry policies with $1 million per occurrence and $2 million aggregate limits because clients and contract requirements demand it.

When Bodily Injury Coverage Kicks In

Someone slips on your wet concrete pour and breaks their arm. Your worker gets hit by a falling tool at a client’s property. A homeowner’s child suffers injury from equipment you left unattended. These scenarios trigger bodily injury coverage, which pays for medical expenses, lost wages, and court judgments if the injured party sues. The policy also covers your legal defense, which means the insurer pays your attorney’s fees regardless of whether you win or lose the case. This distinction matters because legal defense costs can add up quickly in construction disputes. Idaho law requires contractors to register with the Idaho Contractors Board and carry general liability insurance of at least $300,000 single limit, but this minimum is dangerously low for most jobs.

Property Damage Claims and What They Include

You accidentally damage a client’s roof while working on their home. Your equipment punctures their water line during excavation. You knock over an expensive piece of furniture during installation. Property damage coverage pays for repairs or replacement of the damaged property, plus the cost to defend yourself if the property owner sues. ERGO NEXT, another top Idaho provider according to MoneyGeek, offers up to $2 million per occurrence with strong coverage for contractor-related risks. The difference between $300,000 and $1 million coverage becomes critical when you damage expensive residential or commercial property. A single mistake on a high-value project can wipe out your annual profit without adequate limits.

Why Legal Defense Costs Matter

Construction disputes often lead to lawsuits, and your attorney’s fees add up fast. Your insurer covers these defense costs as part of your policy (whether you’re found liable or not). This protection prevents you from paying thousands out of pocket while your case moves through the court system. Many contractors underestimate how quickly legal bills accumulate-depositions, expert witnesses, and court appearances consume time and money. Without this coverage built into your policy, you face a choice between paying for defense yourself or risking an undefended judgment against your business.

Coverage Limits That Match Your Risk

Idaho contractors operate across residential, commercial, and industrial projects, each carrying different exposure levels. A $300,000 limit might cover a small residential repair job, but it leaves you exposed on larger projects. Most clients now require $1 million per occurrence and $2 million aggregate as a condition of contract, making these limits the practical standard in the market. Your specific risk depends on the scope of work you perform, the value of projects you handle, and the types of properties you work on. The next section explains how to assess your actual exposure and select limits that protect your business without overpaying for unnecessary coverage.

Why Idaho Contractors Actually Need This Coverage

Idaho law doesn’t require general liability insurance for all contractors, but the state does require registration with the Idaho Contractors Board for any construction project valued over $2,000. That registration demands proof of general liability insurance of at least $300,000 single limit. This minimum requirement exists because the state recognizes that construction work creates real financial exposure for property owners and injured parties. However, that $300,000 floor is inadequate for most real-world situations. In fiscal year 2025, the Idaho Department of Professional and Licensing received 485 contractor complaints-the highest among all boards and commissions-signaling that registration alone doesn’t protect clients or contractors from financial disaster.

What Happens When You Skip Coverage

Without proper liability coverage, you face penalties ranging up to $1,000 in fines or six months in jail if you operate without current registration. More practically, practicing without valid coverage prevents you from obtaining building permits and forfeits your lien rights on projects, which means you lose your legal claim to payment if disputes arise. A single serious injury or property damage claim can exceed $100,000 in medical bills, legal fees, and settlements. Your personal assets-your home, savings, vehicles-become vulnerable if you lack adequate insurance and face a judgment that exceeds your business’s financial reserves.

Client Expectations Set the Real Standard

Most property owners, developers, and general contractors now require proof of $1 million per occurrence and $2 million aggregate liability coverage before they’ll sign a contract or allow you on their job site. This expectation has become the practical standard across Idaho’s construction market, and contractors who carry only the state minimum find themselves unable to bid on larger residential and commercial projects. The North Idaho Building Contractors Association has reported a dramatic uptick in contractor complaints in recent years, which has intensified scrutiny on contractor qualifications and financial protection.

How Insurance Affects Your Competitive Position

Clients increasingly request certificates of insurance listing them as additional insured parties, which means they need documented proof that you carry adequate coverage. Without this documentation readily available, you lose contract opportunities to competitors who can provide it instantly. Insurance also demonstrates to potential clients that you operate professionally and take your legal obligations seriously, which builds trust and justifies higher pricing for quality work. Contractors who invest in proper coverage position themselves as the safer choice in a market where clients have legitimate concerns about hiring uninsured or underinsured workers.

The next section walks you through the process of selecting the right coverage limits and deductibles for your specific business model.

Selecting Coverage Limits That Match Your Actual Work

Choosing the right liability coverage starts with understanding what you actually do on job sites and what financial exposure that work creates. A residential kitchen remodel carries different risk than commercial foundation work or industrial equipment installation. The state minimum of $300,000 single limit satisfies legal registration requirements, but it falls dangerously short of what clients demand and what real claims cost. Most Idaho contractors operate with $1 million per occurrence and $2 million aggregate because that’s what general contractors, property managers, and developers now require before signing contracts. The difference between these limits matters enormously-a single serious injury claim can reach $150,000 to $500,000 in medical expenses and legal costs, which means the state minimum leaves you personally liable for the excess.

Match Coverage to Your Project Value

Your project value drives coverage decisions directly. If you handle jobs consistently under $50,000, you might operate with $500,000 limits and still meet most client requirements. If you bid on projects exceeding $500,000 or work on commercial properties, $1 million per occurrence becomes the practical floor. ERGO NEXT and The Hartford both offer flexible limit combinations that let you match coverage to your actual risk profile rather than overpaying for unnecessary limits. The Hartford provides coverage limits from $300,000 to $2 million per occurrence, with aggregate limits up to $4 million, giving you options across different project scales.

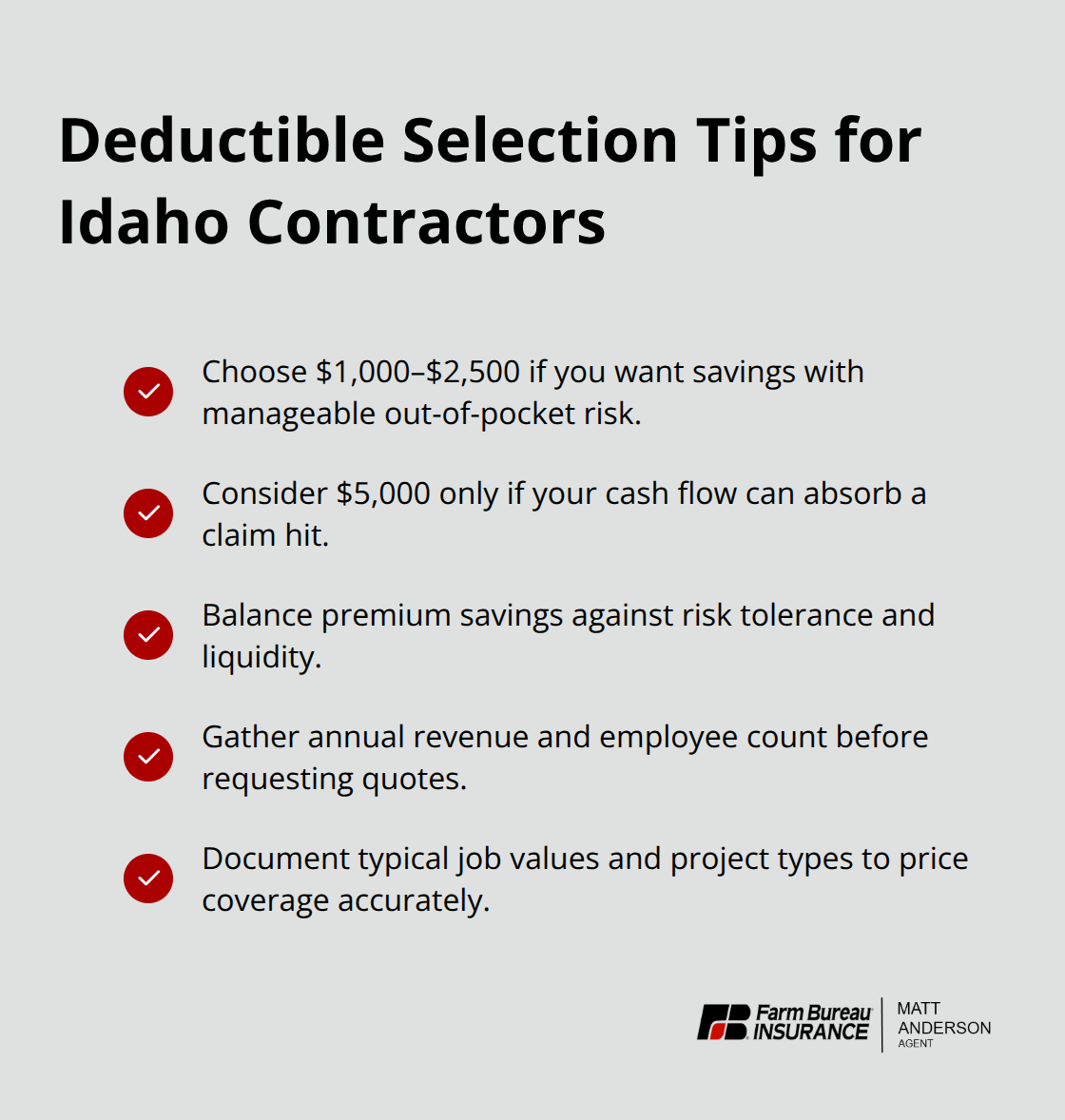

Select Deductibles That Protect Your Cash Flow

Deductibles operate as your out-of-pocket cost before insurance kicks in, and selecting the right deductible saves money without exposing you to catastrophic loss. Most Idaho contractors choose $1,000 or $2,500 deductibles because these levels reduce premiums meaningfully while remaining manageable if a claim occurs. A $5,000 deductible might save 15 to 20 percent on annual premiums, but only if you can absorb that cost without financial strain when a claim happens. The best approach involves gathering specific details about your business before requesting quotes-your annual revenue, number of employees, business classification, and the types of projects you typically handle.

Compare Quotes From Multiple Idaho Insurers

Identical coverage from different Idaho insurers can vary significantly, which means comparing quotes from at least three licensed providers makes financial sense before purchasing. When comparing quotes, verify whether defense costs are included inside your policy limits or paid separately by the insurer, because this distinction affects how much coverage actually remains available for settlement or judgment. This comparison process takes time but protects your bottom line significantly.

Review Coverage Annually and After Major Changes

You should review your coverage annually and especially after hiring employees, expanding into new service areas, or moving into different Idaho counties where local requirements might differ. A local Idaho insurance agent who understands construction risk can identify endorsements specific to your trade-such as contractual liability coverage or products completed operations coverage-that protect against gaps in your standard policy. These endorsements address real exposures that standard policies often exclude, making them worth the additional cost for most contractors.

Final Thoughts

Contractor liability insurance in Idaho protects your business from financial ruin when accidents happen on job sites. The state minimum of $300,000 satisfies registration requirements, but real-world claims and client expectations demand $1 million per occurrence and $2 million aggregate limits. Without adequate coverage, you face personal liability, lost lien rights, and inability to bid on projects that require proof of insurance.

Your next step involves gathering basic business information-annual revenue, employee count, project types, and typical job values-then requesting quotes from at least three Idaho-licensed insurers. Compare not just price but also whether defense costs are included inside your limits or paid separately, and verify that endorsements match your specific trade risks. The 485 contractor complaints filed with Idaho’s Department of Professional and Licensing in fiscal year 2025 demonstrate that registration alone doesn’t protect you or your clients from costly disputes.

We at Matt Anderson Insurance understand Idaho’s construction environment and the real exposures contractors face daily. Contact us today for a quote on contractor liability insurance in Idaho that protects your business without overpaying for unnecessary coverage. Our team can help you select coverage limits that match your actual risk and identify cost-saving endorsements specific to your trade.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.