Idaho Short Rental Coverage: Essential Protections for Your Vacation Rental

Your vacation rental in Idaho generates income, but standard homeowners insurance won’t protect that business. Guest injuries, property damage, and lost rental income can quickly drain your profits without the right coverage.

At Matt Anderson Insurance, we see too many rental owners scrambling after a claim because they skipped Idaho short rental coverage. The right policy fills the gaps your homeowners insurance leaves wide open.

Why Your Homeowners Policy Leaves You Exposed

Standard homeowners insurance treats your property as a residence, not a business. The moment you start accepting nightly bookings on Airbnb or VRBO, you’ve crossed into hospitality-and your homeowners policy no longer covers you. Your insurer can deny claims if they discover you’re running a rental operation under a homeowners policy.

Rental income itself receives zero protection under standard homeowners coverage. If a pipe bursts and forces cancellations for two weeks, your homeowners policy won’t reimburse the lost bookings. That gap alone justifies specialized coverage.

General liability insurance for Idaho short-term rentals typically costs $400–$1,200 annually, while loss of rental income coverage runs $150–$600 per year. These premiums are far cheaper than absorbing a month of cancelled reservations or defending a guest injury lawsuit out of pocket.

Guest Liability Exposure Climbs Fast

Every guest who steps through your door creates liability exposure your homeowners policy ignores. A guest slips on your deck and breaks an ankle. Another guest’s child wanders into an unsecured hot tub. A third guest’s dog bites another visitor. These scenarios happen regularly at Idaho vacation rentals, especially in high-traffic areas like Boise, Coeur d’Alene, and Sun Valley where seasonal spikes bring constant turnover.

Your homeowners liability typically maxes out at $300,000–$500,000, but that limit applies to your personal use only. Once guests arrive, standard coverage becomes unreliable. Specialized short-term rental policies provide commercial general liability starting at $1 million, covering incidents both on and off your property. Liquor liability-often excluded from homeowners policies-comes included with proper rental coverage, protecting you if a guest consumes alcohol and causes harm.

Property Damage Claims from Guests

Guests damage furnishings, break appliances, stain carpets, and leave the place trashed. Standard homeowners coverage has strict exclusions for guest-caused damage and often caps replacement value. Dedicated rental policies use new-for-old replacement cost, meaning you recover full value to restore your property without depreciation deductions. Property entrustment coverage, a feature rarely found in standard policies, protects against guest theft and vandalism-gaps that leave many Idaho hosts unprotected. This coverage matters most at high-turnover properties where guest screening becomes harder to control.

Revenue Protection Closes the Income Gap

Loss of rental income coverage protects your actual losses from covered claims with no time limits and up to your policy limit. If a kitchen fire forces a two-month closure during peak summer season, you recover the full rental revenue you would have earned-not a penny less. Contents and furnishings coverage typically costs $250–$1,500 annually and protects your investment in beds, appliances, smart devices, and outdoor equipment.

The right short-term rental policy transforms how you handle risk. Your next step involves understanding exactly what coverage limits fit your property’s value and occupancy patterns.

What Your Rental Coverage Actually Protects

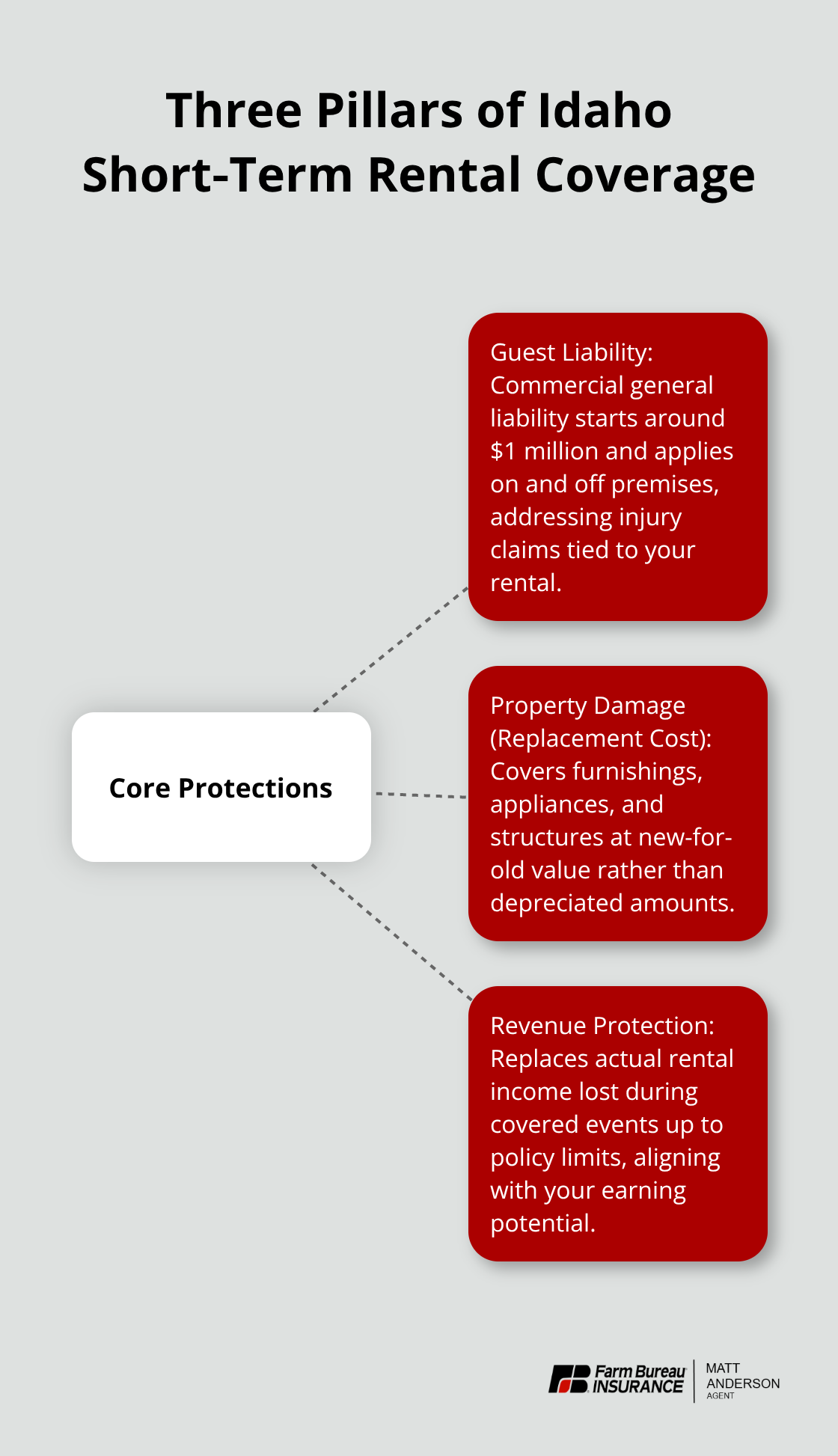

Guest Liability Protection Starts at $1 Million

Idaho vacation rental policies cover three distinct exposure areas that standard homeowners insurance ignores entirely. Guest liability protection shields you when someone gets hurt on your property or because of something that happens at your rental. Commercial general liability on dedicated short-term rental policies starts at $1 million and applies to incidents both on and off your premises-far exceeding the typical homeowners limit. This matters significantly in Idaho’s high-traffic rental zones. A guest fractures a wrist falling down poorly lit stairs in Boise, or a visitor’s child requires emergency care after accessing a hot tub in Sun Valley-these claims exceed standard homeowners coverage instantly.

Liquor liability comes included with proper rental policies, protecting you if a guest drinks alcohol at your property and injures themselves or someone else. Your homeowners policy excludes this exposure entirely. Bodily injury coverage also handles medical payments when guests need immediate treatment, reducing the likelihood they pursue a lawsuit.

Property Damage Coverage Uses Replacement Cost

Property damage coverage under rental policies uses replacement cost rather than depreciation, meaning you recover full value to restore your rental to working condition. When a guest damages furnishings, breaks appliances, or causes structural damage, your policy reimburses the cost to replace items new-not deducted for age or wear. Contents and furnishings coverage typically costs $250–$1,500 annually and protects beds, kitchen equipment, smart home devices, outdoor amenities like kayaks or bicycles, and hot tubs.

Property entrustment coverage, included in comprehensive rental policies, covers theft and vandalism by guests-a gap that leaves most Idaho hosts exposed. This protection proves essential at properties with high guest turnover, where screening becomes harder to control.

Revenue Protection Replaces Lost Income

Loss of rental income coverage replaces actual revenue lost during covered events with no time limits and up to your policy limit. If a winter storm damages your roof in McCall and forces a three-month closure during peak season, you recover the full rental income you would have earned during repairs. This coverage typically costs $150–$600 annually and functions as genuine income protection, not a cap on reimbursement.

Bed bug and flea protection covers both liability and extermination costs plus lost revenue from cancellations-a real exposure at properties with high guest turnover. Squatters protection handles situations where guests refuse to leave or exceed the 30-day threshold, providing legal support and revenue protection while you navigate eviction.

Choosing the Right Limits for Your Property

These three pillars-guest liability, property damage with replacement cost, and revenue protection-form the backbone of legitimate short-term rental insurance in Idaho. Your property’s nightly rate, occupancy patterns, and location determine which coverage limits actually fit your situation. A high-end Sun Valley cabin commands different protection than a modest Boise townhouse, and seasonal properties face different risks than year-round rentals.

Understanding your specific exposure helps you avoid both underinsurance and unnecessary premium costs.

Matching Coverage to Your Rental’s Real Income and Risk

Calculate Your Actual Revenue to Set Liability Limits

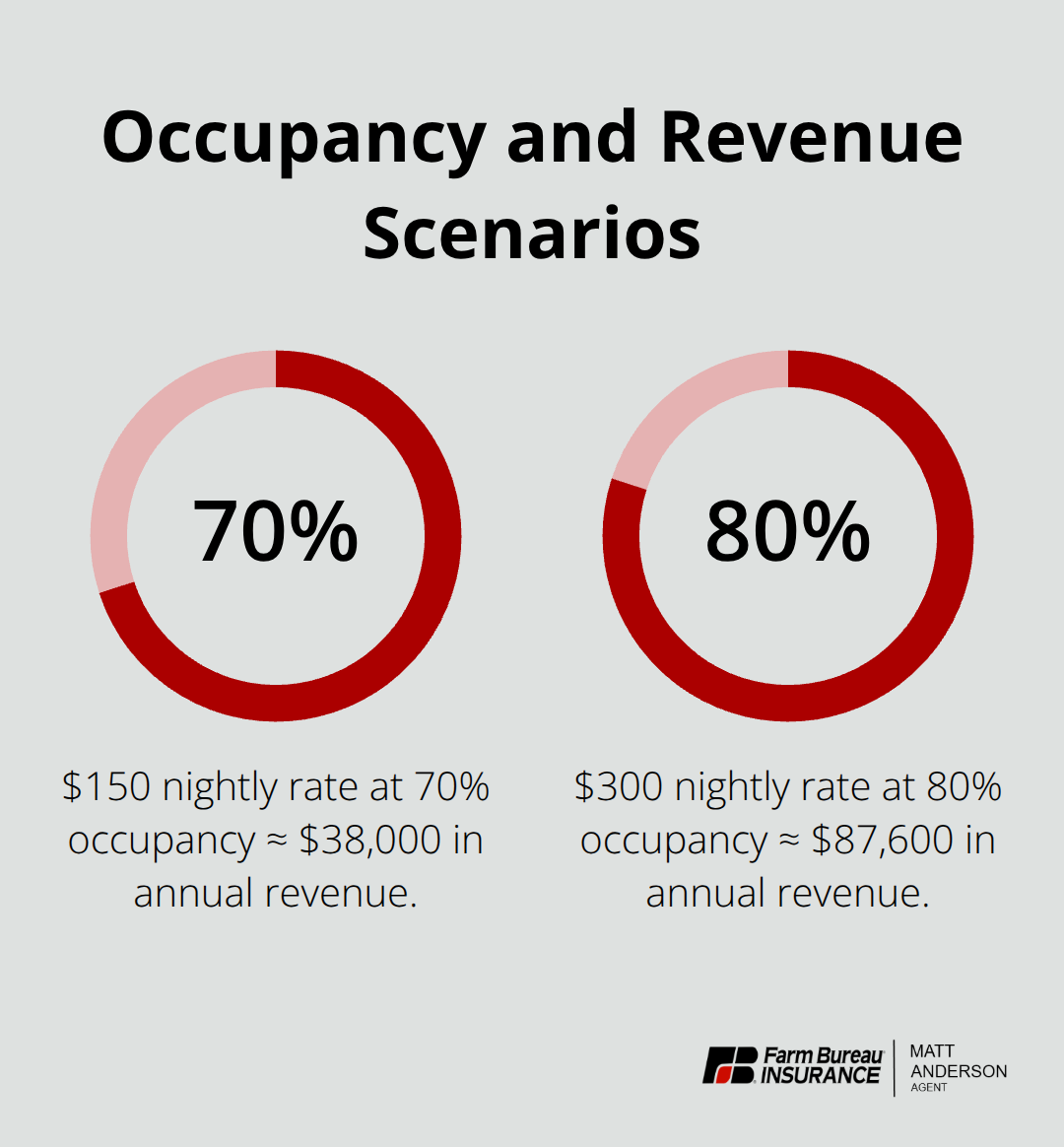

Start with your actual nightly rate and occupancy patterns, not guesses about what you might earn. A property that rents at $150 per night with 70 percent annual occupancy produces roughly $38,000 in annual revenue, while a $300 nightly rate at 80 percent occupancy produces $87,600. These numbers matter because your liability limits and revenue protection must reflect what you stand to lose.

General liability at $1 million covers most Idaho rentals adequately, but properties in high-traffic zones like Sun Valley or Boise with multiple amenities benefit from umbrella liability coverage, which typically costs $200–$700 annually and raises your total limit above the base policy.

Account for Location-Based Premium Factors

Location drives pricing significantly. Waterfront properties near Lake Coeur d’Alene or Payette Lake face higher premiums due to increased water-related liability, while northern Idaho properties in snow zones like McCall and Ketchum see premium increases tied to winter damage exposure and higher replacement values for structures built to withstand heavy snow loads. Your revenue protection limit should match your realistic peak-season monthly earnings, not your best-case scenario. If your property generates $6,000 monthly during summer but only $2,000 during winter, loss of rental income coverage protects that gap when covered events force closures.

Inventory Your Contents and Furnishings

Contents and furnishings coverage protects your actual investment in beds, kitchen equipment, smart home devices, outdoor gear, and hot tubs. Inventory these items and add replacement costs to justify your coverage level. Bundling short-term rental coverage with auto, home, or umbrella policies through a single agent typically yields 10–25 percent savings on premiums while simplifying claims and renewals.

Review and Adjust Coverage Annually

We recommend reviewing your policy annually as occupancy rates shift and property improvements increase replacement value. Seasonal properties need particular attention: if you close during winter, discuss coverage adjustments with your agent rather than paying for protection during months when your rental sits empty. Mortgage lenders often require commercial-use endorsements on financed properties, so verify your lender’s requirements before purchasing coverage to avoid claim denials later.

Document Your Property and Booking Activity

Document your property thoroughly with photos of furnishings, appliances, and amenities, then maintain a booking spreadsheet showing occupancy and nightly rates. This data proves your actual rental income to insurers and supports loss-of-revenue claims if damage occurs.

Final Thoughts

Your Idaho short rental coverage only works if it matches your actual property and business. Working with an agent who understands Idaho’s rental market makes this process straightforward-local agents know how Boise’s year-round demand differs from McCall’s seasonal peaks, how waterfront properties near Lake Coeur d’Alene face different risks than mountain cabins, and which coverage gaps matter most in your specific area. They can explain why a property in Sun Valley needs higher limits than one in a smaller town, and how winter weather exposure in northern Idaho affects your premium and protection needs.

Your policy requires adjustment as your occupancy rates climb or you add amenities like hot tubs and fire pits. Annual reviews catch these changes before they create gaps in protection, and if you upgrade appliances or furnishings, your contents coverage should reflect the new replacement value. Seasonal properties especially benefit from annual reviews, since closing during winter months might allow coverage adjustments that reduce unnecessary premiums.

Documentation protects you when claims happen-photograph your furnishings, appliances, and outdoor equipment before guests arrive, and keep booking records showing occupancy rates and nightly rates since insurers verify this data during underwriting and claims. Contact us to review your Idaho short rental coverage and ensure your protection actually fits your property and business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.