Idaho Vacation Rental Coverage: Insurance For Hosts And Properties

Renting out your Idaho property can generate steady income, but standard homeowners insurance won’t protect you. Your guests, their belongings, and liability risks require specialized coverage that most policies simply don’t include.

At Matt Anderson Insurance, we’ve seen too many vacation rental hosts face unexpected gaps in their protection. Idaho vacation rental coverage is designed specifically for short-term rentals-and it’s the difference between a profitable venture and a financial disaster.

Why Your Standard Homeowners Policy Falls Short

Standard homeowners insurance explicitly excludes business activity, and renting your property to guests crosses that line. Your policy was written for owner-occupied homes where you live year-round. The moment you list on Airbnb or Vrbo, you fundamentally change how your property operates-and your insurer won’t cover losses tied to that rental activity. A guest slip-and-fall on an icy deck, theft of their belongings, or damage they cause to your kitchen won’t be covered. Your insurer can even deny claims if they discover you operate a short-term rental without disclosure. This isn’t a gray area; it’s a direct violation of your policy terms.

The liability gap that catches hosts off guard

Liability exposure from short-term rentals differs categorically from owning a vacant property or renting long-term. You invite strangers into your home multiple times per month, each with their own risk profile. A guest injures themselves on your property and sues for medical bills and lost wages. Another guest’s friend gets hurt using your hot tub or kayaks you provide. Standard homeowners policies cap guest medical payments at $1,000 to $5,000-nowhere near adequate if someone requires hospitalization. Short-term rental insurance covers commercial general liability starting at $1 million, protecting you against the actual costs of guest injuries and third-party claims. Without this coverage, a single incident can wipe out your rental income for years.

Property damage and theft accelerate with constant turnover

Long-term tenants stay for months or years, so damage accumulates slowly and patterns emerge. Short-term guests come and go weekly or daily, creating rapid-fire exposure to theft, vandalism, and deliberate damage. A guest steals your artwork, damages appliances, or punches a hole in drywall before checkout. Standard homeowners policies don’t cover theft or damage caused by guests because those policies assume you live there and control access. Short-term rental insurance includes property entrustment coverage-protection against guest theft and malicious damage that standard policies explicitly exclude. You also receive replacement cost coverage with no depreciation, meaning your belongings and building receive full value protection, not reduced for age. This matters when a guest damages a five-year-old refrigerator; you receive replacement cost, not depreciated value.

Income loss from cancellations leaves owners vulnerable

When a covered incident makes your property unrentable, your income stops immediately. A fire, water damage, or bed bug infestation forces you to cancel bookings and lose revenue while repairs happen. Standard homeowners policies don’t reimburse lost rental income because they don’t recognize your property as a business asset. Short-term rental insurance includes business revenue protection that reimburses actual loss sustained if a covered claim prevents you from renting. This coverage bridges the gap between when damage occurs and when you can welcome guests again. Without it, you absorb months of lost bookings while your property sits idle.

What Your Vacation Rental Coverage Actually Protects

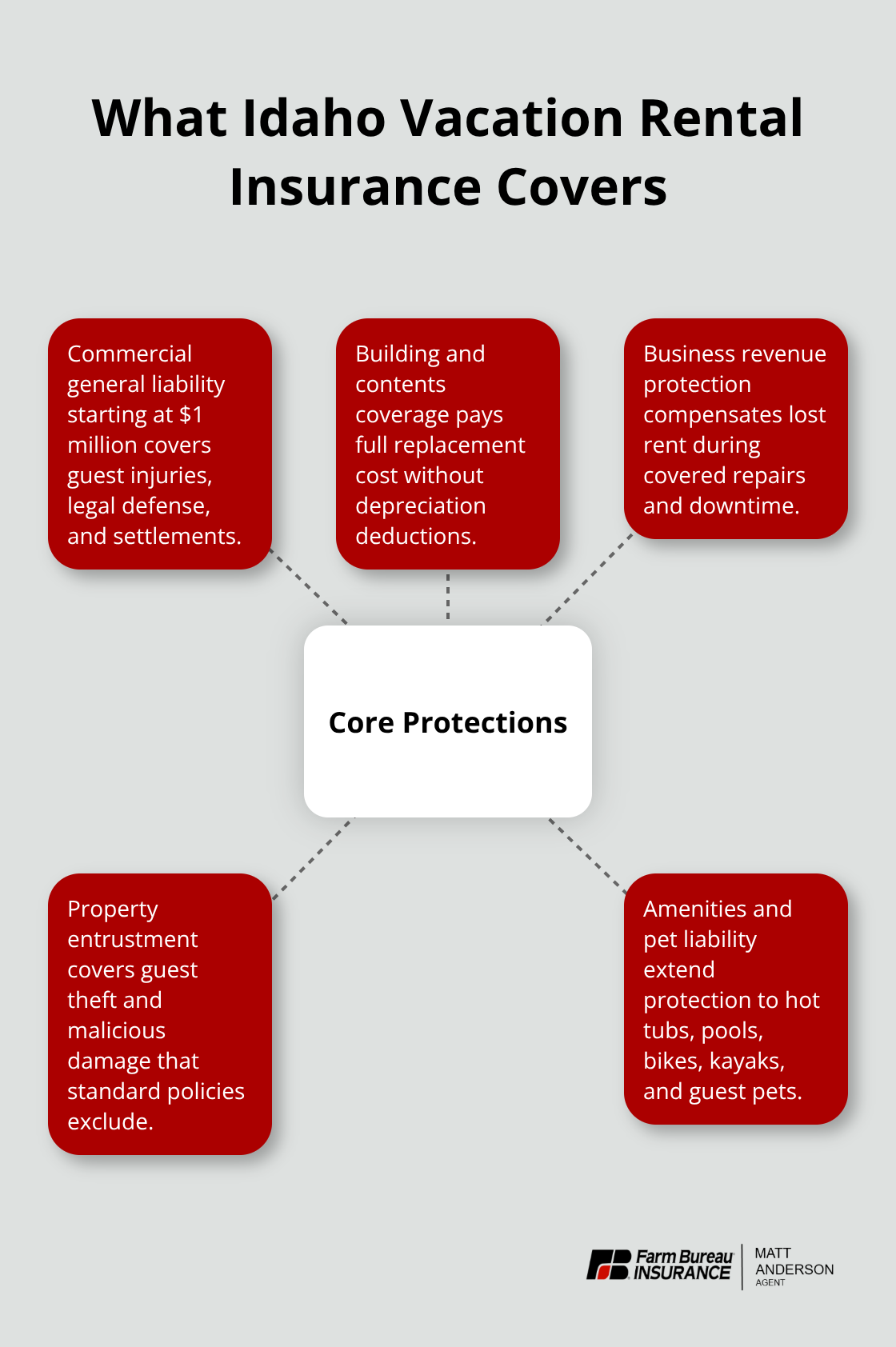

Commercial Liability Protection for Guest Injuries

Idaho vacation rental insurance covers three distinct areas that standard homeowners policies treat as exclusions. First, commercial general liability protection starts at $1 million and shields you when a guest or their visitor gets injured on your property or by amenities you provide. A guest slips on your deck and breaks their leg, or their friend drowns in your hot tub-your liability coverage pays their medical bills, lost wages, and legal fees up to your chosen limit. Standard homeowners policies cap guest medical payments at $1,000 to $5,000, leaving you personally liable for the remainder. With $1 million in commercial liability, you’re protected against the actual costs of hospitalization, surgery, and litigation that a single serious injury can trigger.

Building and Contents Protection With Full Replacement Value

Second, your coverage includes building and contents protection with replacement cost, meaning your property and belongings receive full value without depreciation deductions. If a guest damages your kitchen cabinets, appliances, or furniture, you receive what it costs to replace them today, not their reduced value after years of use. Property entrustment coverage specifically protects against theft and vandalism by guests-the exact scenario standard policies exclude.

A guest steals your artwork, electronics, or outdoor equipment and your coverage reimburses the loss.

Business Revenue Protection During Property Downtime

Third, business revenue protection during property downtime compensates you for rental revenue lost when a covered event like fire or water damage makes your property uninhabitable during repairs. Unlike standard policies that ignore rental income entirely, this protection bridges the gap between when damage occurs and when you reopen to guests.

Specialized Coverage for Unique Short-Term Rental Risks

Beyond these core protections, Idaho vacation rental insurance addresses exposures that catch hosts off guard. Liquor liability coverage protects you if a guest gets drunk at your property and causes injury or property damage afterward-a risk standard homeowners policies explicitly exclude. Bed bug and flea protection covers both extermination costs and lost revenue from booking cancellations due to pest infestations, a growing concern for Idaho hosts. Amenities coverage extends liability protection to equipment guests use off-premises (like bikes, kayaks, and paddleboards you provide) plus hot tubs and pools on your property. Pet and animal liability is included with no breed restrictions, protecting you if a guest’s dog bites someone or if your pet injures a visitor. Squatter protection provides legal support and lost revenue compensation if a guest refuses to leave after their booking ends-a rare but devastating scenario that standard policies don’t address.

These additions exist because short-term rental risks differ fundamentally from homeownership or long-term tenancy. Your property transforms into a commercial operation the moment you accept guests, and your insurance must reflect that shift. The coverage gaps that plague unprepared hosts stem from this mismatch between how standard policies work and how vacation rentals actually operate. Understanding what protection you need is only half the battle-selecting the right limits and options for your specific property requires careful assessment of your guest volume, property type, and local Idaho risks.

Selecting Coverage That Matches Your Idaho Rental Operation

Your property’s risk profile determines which coverage limits you actually need, and most hosts either overinsure or leave dangerous gaps. Start by counting your annual guest nights and tracking property incidents over the past year. A mountain cabin in McCall that hosts 40 weekends annually faces different exposure than a Boise condo rented 300 nights per year to international tourists. High-turnover properties with frequent guests justify higher liability limits because each booking introduces new people into your space. Idaho hosts renting near ski resorts or lake communities see seasonal spikes that concentrate risk into winter and summer months, requiring coverage that reflects peak occupancy periods.

Assess Your Property’s Specific Risk Factors

Document whether guests bring pets, how many people typically occupy your property, and what amenities you provide. A hot tub or swimming pool dramatically increases liability exposure compared to a basic cabin. If you offer equipment like kayaks, mountain bikes, or jet skis, your liability extends to injuries occurring off-premises while guests use those items. Insurance carriers weight these factors heavily when calculating your premium and determining appropriate limits. A $1 million liability limit works for most Idaho hosts, but properties with pools, multiple amenities, or high guest volume should consider $2 million coverage.

Match Building Coverage to Replacement Cost

Building coverage should equal your property’s replacement cost, not its market value-a critical distinction that catches many hosts off guard. Market value includes land; replacement cost covers only the structure and contents. Get a contractor’s estimate for what it would cost to rebuild your property from scratch, then match that figure in your policy. Contents coverage should account for furnishings, appliances, linens, and equipment you provide to guests. Many Idaho hosts underestimate contents value because they forget about kitchen equipment, outdoor furniture, and seasonal décor.

Calculate Loss of Income Protection Accurately

Loss of income protection should reflect your average monthly rental revenue. Calculate your typical booking rate and nightly rate, then multiply by 30 days. This becomes your monthly protection amount. Some carriers cap business revenue coverage at 12 months; verify whether your policy includes this limit before purchasing.

Compare Deductibles and Premium Costs

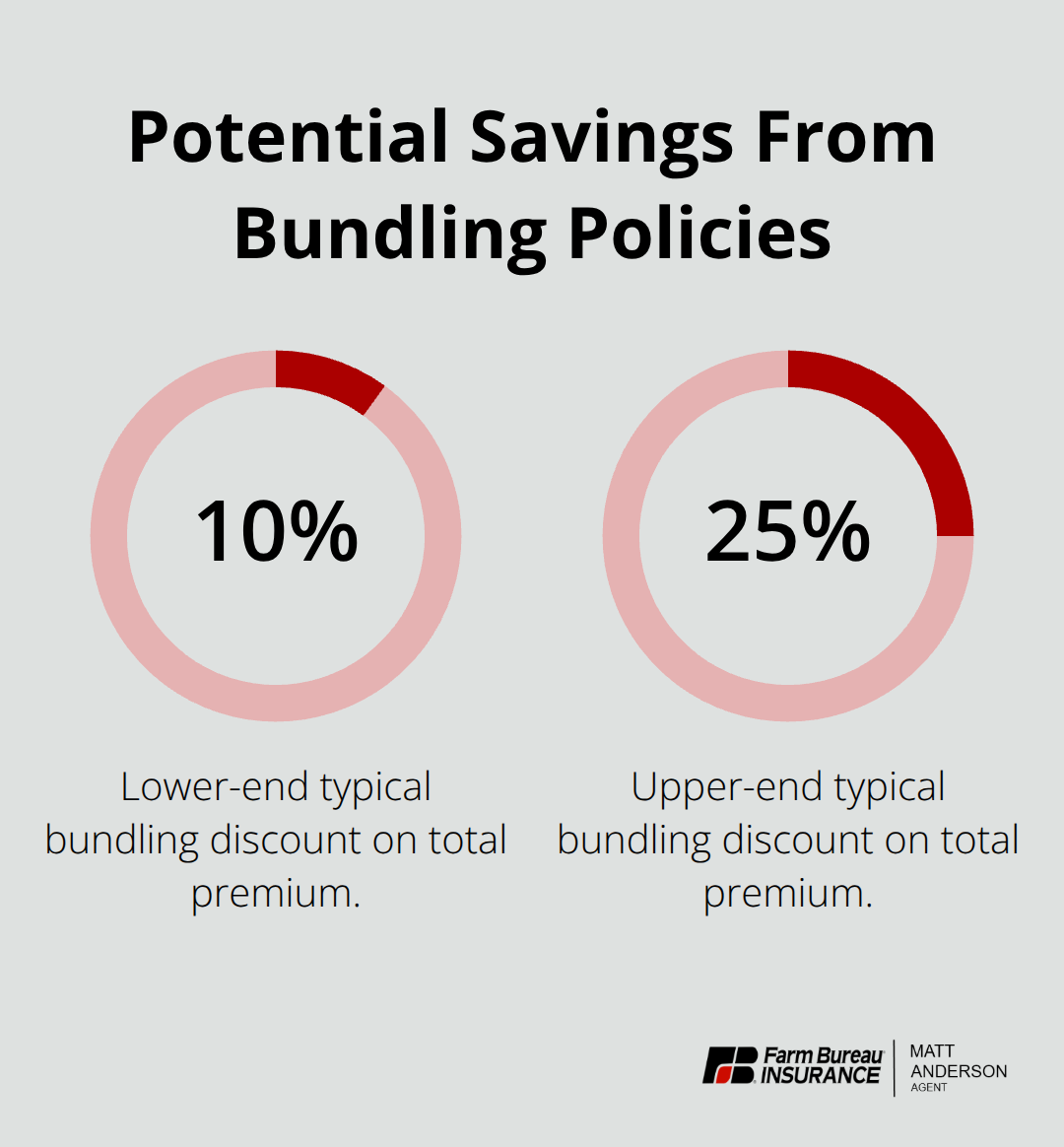

Deductibles require understanding how they affect your actual out-of-pocket costs versus premium savings. A $500 deductible costs less monthly than a $1,000 deductible, but you pay $500 from your pocket for every claim. Idaho hosts filing claims for guest damage or theft often face multiple incidents per year, making high deductibles expensive in practice. Most short-term rental hosts benefit from $500 to $750 deductibles that balance reasonable monthly premiums with manageable claim costs. Bundling your vacation rental coverage with auto, home, or other policies typically generates 10-25% savings on your total premium, though discounts vary by carrier and coverage type.

Request quotes from multiple carriers rather than accepting the first offer, since short-term rental insurance pricing varies significantly based on how each company rates property type, location, guest volume, and claims history. An independent agency can quote carriers that a captive agent cannot access, potentially saving you hundreds annually. Ask specifically about occupancy discounts if your property sits vacant during off-season months-some carriers reduce premiums when you’re not actively renting. Review your coverage annually as your guest volume changes, property improvements increase replacement value, or you add amenities like hot tubs. A policy purchased when you rented 100 nights per year may inadequately protect you after you increase to 250 nights. Idaho’s short-term rental market continues expanding, particularly in North Idaho mountain communities, and rates may shift as carriers adjust their underwriting.

Final Thoughts

Your Idaho vacation rental coverage requires active maintenance as your business evolves. Review your policy annually, especially if you’ve increased guest bookings, added amenities like hot tubs or fire pits, or upgraded your property. What protected you adequately at 100 annual guest nights may leave gaps when you reach 250 nights, and carriers often adjust rates based on claims history and market conditions.

Document your property’s condition before each guest arrives through photos and videos of the building, contents, and amenities. Time-stamped photos establish what condition your property was in, protecting you against false damage claims and strengthening legitimate claims when incidents occur. Many hosts use simple smartphone photos stored in cloud storage, making this process quick and free.

At Matt Anderson Insurance, we specialize in protecting Idaho hosts with comprehensive short-term rental coverage tailored to your property type, guest volume, and local risks. Our licensed agents understand Idaho’s unique rental landscape and can bundle your vacation rental coverage with auto and home policies for significant savings. Contact us to review your current protection and ensure your Idaho vacation rental coverage matches your actual business needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.