Idaho Contractor General Liability: Essential Coverage For Construction Work

One accident on a job site can cost your business thousands of dollars. Without proper coverage, you’re personally liable for injuries and property damage claims.

At Matt Anderson Insurance, we help Idaho contractors protect themselves with general liability coverage. This protection isn’t optional-most clients and lenders require it before you start work.

What General Liability Coverage Actually Covers

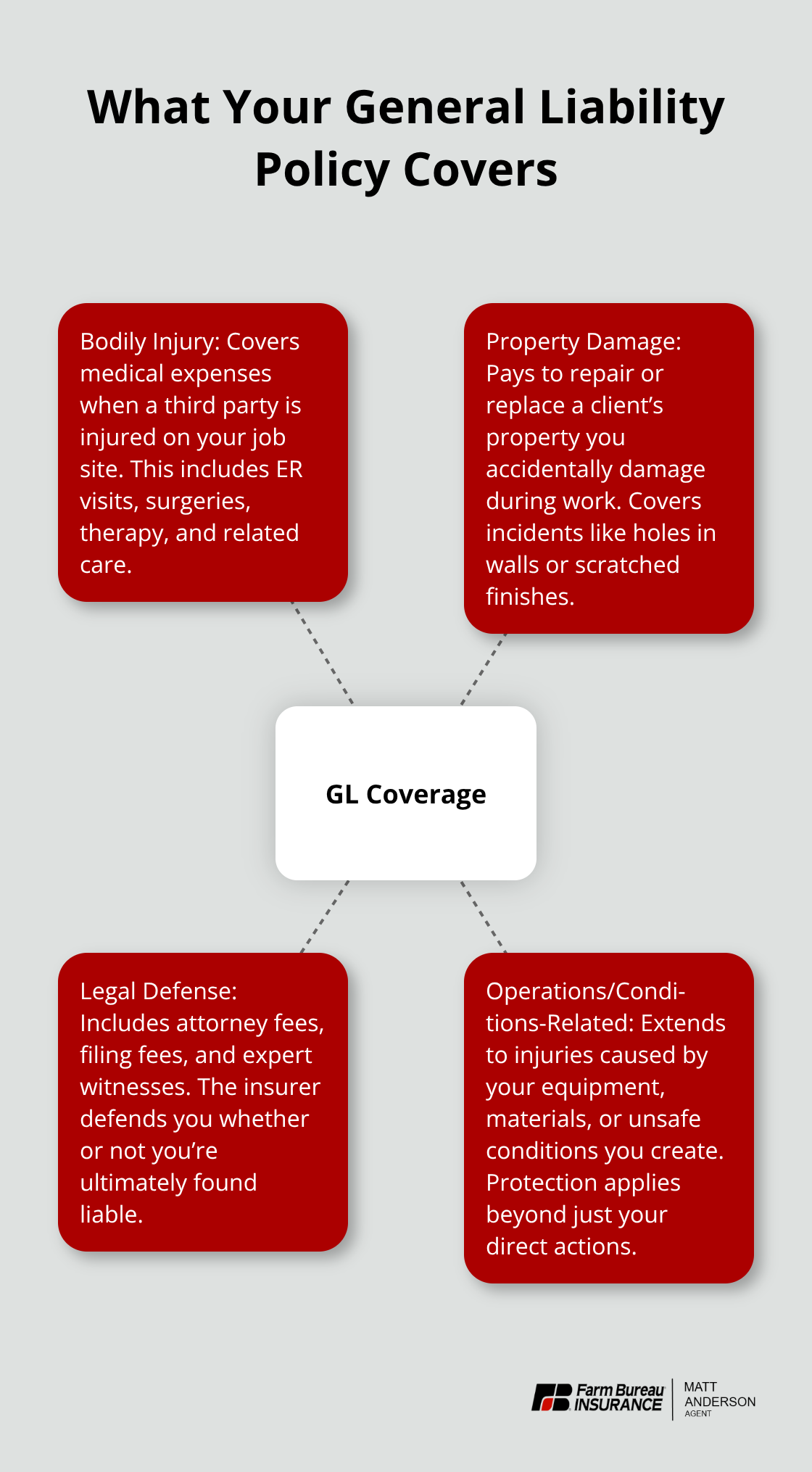

General liability insurance protects you when someone gets hurt on your job site or you accidentally damage a client’s property. If a homeowner trips over your equipment and breaks their arm, or your crew accidentally puts a hole in their wall, your general liability policy covers the medical bills, repair costs, and legal fees that follow. The Idaho Contractors Board requires a minimum of $300,000 in coverage to register, but that baseline is inadequate for real-world construction work. Most Idaho contractors now carry $1,000,000 per occurrence with $2,000,000 aggregate because clients and contract requirements demand it.

A single injury claim or property damage lawsuit can easily exceed $300,000-a fall from a ladder, a back injury from lifting, or structural damage during renovation can push costs well beyond six figures when you factor in medical treatment, lost wages, and legal defense.

Medical Bills and Injury Claims

Your general liability policy pays for emergency room visits, surgeries, physical therapy, and ongoing medical care when someone is injured at your job site. It also covers lost wages if an injured party cannot work during recovery. The policy covers not just your direct actions but also injuries caused by your equipment, materials, or unsafe conditions you created. Legal defense costs are included as part of the policy, meaning your insurer pays for attorneys, court filing fees, and expert witnesses whether or not you’re ultimately found liable. This protection matters because serious injuries generate substantial medical and legal expenses before any settlement or judgment is issued.

Property Damage You’re Responsible For

If your crew damages a client’s property-a roof, flooring, plumbing, electrical system, or personal belongings-your general liability policy covers the repair or replacement costs. This includes damage caused by negligence, accidents, or mistakes during the construction process. The policy also protects you if materials you bring to the job site cause damage, such as paint spilling on hardwood floors or tools scratching finished surfaces. Without this coverage, you’re personally responsible for paying out of pocket, which can wipe out your profit margin on a project or force you into debt. A kitchen renovation can become a significant loss if your crew damages cabinets, appliances, or countertops and you lack insurance to cover it.

Why the $300,000 Minimum Falls Short

Idaho law sets a $300,000 single-limit minimum, but this amount rarely matches what modern construction projects actually demand. Clients now commonly require $1,000,000 per occurrence and $2,000,000 aggregate before they sign contracts or permit site access. The difference between a $300,000 limit and $1,000,000 per occurrence can be decisive on high-value projects, as a single injury or property damage claim can exceed a six-figure amount. When you bid on residential or commercial work, inadequate coverage signals risk to potential clients and can cost you jobs. Carrying limits that align with industry expectations positions you as a safer, more professional contractor and supports competitive bids.

Why Your Business Needs General Liability Coverage Now

Idaho’s Contractors Board requires a minimum of $300,000 in general liability coverage to register for projects exceeding $2,000, but registration alone won’t protect you from financial ruin. Without adequate coverage, a single job site accident drains your personal bank account, forces you to sell assets, and destroys your ability to bid on future work. More importantly, clients won’t hire you without proof of coverage. Modern contract requirements in Idaho construction demand $1,000,000 per occurrence and $2,000,000 aggregate before homeowners or commercial property owners sign agreements or grant site access. If you carry only the $300,000 minimum, you face a competitive disadvantage-potential clients view that as a red flag that you cut corners on protection. General liability coverage isn’t just a regulatory checkbox; it’s the foundation that separates contractors who win bids from those who stay small and struggle to land quality projects. A serious injury claim or property damage lawsuit can result in substantial costs when medical expenses, legal defense, and settlements combine. Your personal homestead, savings, and future income sit at stake without proper limits.

Registration Proves You Exist-Insurance Protects You

Idaho registration proves you meet baseline requirements, but your general liability policy actually covers claims. Many contractors mistakenly think registration protects them-it doesn’t. You can be fully registered and still lose everything in a lawsuit if your coverage limits are too low or nonexistent. The state requires you to show proof of $300,000 in general liability at registration, but that’s a legal floor, not a practical ceiling. Clients, lenders, and surety bond companies expect $1,000,000 per occurrence as the industry standard. If you apply for a construction loan or bonding, lenders ask for certificates of insurance naming them as additional insured, and they reject anything below $1,000,000 per occurrence. This isn’t negotiable on projects valued above $500,000.

Why Certificates of Insurance Matter Now

When you bid on work, providing a current certificate of insurance is now table stakes-many contractors lose bids simply because they can’t produce the required proof within 24 hours. Digital certificates from most insurers are available within hours of purchase, so delays cost you opportunities. Clients require certificates naming them as additional insured before they permit your crew on site or sign contracts. Without this documentation ready, you can’t move forward on a project, even if your coverage is solid. The certificate proves your limits, your policy dates, and your insurer’s contact information-all details that clients verify before work starts. Having certificates prepared and accessible means you respond to requests immediately and demonstrate professionalism that wins contracts.

What Happens When Coverage Falls Short

A $300,000 limit sounds substantial until a serious claim arrives. Medical costs for a spinal injury, multiple surgeries, and years of physical therapy easily exceed $300,000. Add legal defense costs, expert witness fees, and court settlements, and your coverage evaporates fast. Once your policy limit is exhausted, your personal assets become the target. Clients also won’t work with contractors whose coverage doesn’t match project scope-a $500,000 renovation project demands $1,000,000 in coverage, not $300,000. Inadequate limits signal to potential clients that you operate on a shoestring budget and can’t handle their work professionally. This perception costs you bids on larger, more profitable projects. The contractors who consistently win quality work carry limits that match industry expectations and client demands.

How to Choose the Right Coverage Limits

Start with your actual project values, not the legal minimum. If you regularly bid work under $50,000, a $500,000 per occurrence limit may technically work, but you’ll lose jobs the moment a client asks for $1,000,000 coverage. The practical reality in Idaho construction is that clients now demand $1,000,000 per occurrence and $2,000,000 aggregate before they sign contracts or allow your crew on site. This expectation isn’t negotiable on residential renovations, commercial builds, or any project over $500,000. You should align your limits to the high end of your typical project value, not the low end. If your average job runs $150,000 to $300,000, carrying $1,000,000 per occurrence positions you to win bids without constant coverage objections. Higher limits also signal professionalism to potential clients and make you competitive for larger work that generates better margins. Many Idaho contractors who stuck with the $300,000 minimum have discovered they can’t bid on projects valued above $250,000 because clients won’t accept that coverage.

What Top Insurers Offer in Idaho

The Hartford offers general liability limits from $300,000 up to $2,000,000 per occurrence, with aggregate limits up to twice the per-occurrence amount. ERGO NEXT provides similar flexibility with per-occurrence limits up to $2,000,000 and $4,000,000 aggregate, plus contractor-focused endorsements like completed operations coverage that close gaps in standard policies. Both carriers give you the range you need to match your actual business risk.

Coverage Costs Less Than You Lose in Missed Bids

The Hartford’s rates for Idaho contractors start around $77 per month for basic coverage, while Simply Business, Nationwide, and Progressive average $91 to $95 per month depending on your trade and claims history. If you’re currently operating with the minimum $300,000 limit and losing bids because of it, the extra $30 to $40 monthly for $1,000,000 coverage pays for itself the moment you land one additional project that requires higher limits. A single $150,000 job that you win because you carry adequate coverage generates far more profit than the annual insurance cost.

Deductibles also influence your premium; choosing a $1,000 deductible versus a $5,000 deductible can reduce your monthly cost by 15 to 20 percent, but only if you can comfortably cover that deductible from operating cash when a claim arrives. Most contractors should avoid stretching for the lowest premium if it forces them to choose a deductible they can’t actually afford to pay. When you request quotes from at least three Idaho-licensed insurers, ask whether defense costs are included within your policy limits or paid separately. This distinction matters because legal defense on a serious injury claim can consume $50,000 or more in attorney fees, expert witnesses, and court costs before any settlement is reached. If defense costs eat into your policy limit, a $1,000,000 limit effectively becomes $900,000 or less for actual claim settlement. Insurers that pay defense costs outside the policy limit protect your full coverage amount for actual damages.

Endorsements Close Gaps That Cost You Jobs

Standard general liability policies exclude professional errors, so if you offer design services or structural advice, you need professional liability or errors and omissions coverage on top of your general liability. Contractual liability coverage should be added to your policy so that you’re protected when you sign client agreements that require you to hold them harmless from their own negligence. Products and completed operations endorsements protect you after project completion when faulty workmanship causes injury or property damage months or even years later. Without this endorsement, your coverage ends when you leave the job site, leaving you exposed on warranty claims and post-completion defects. The Hartford and ERGO NEXT both offer these endorsements, but you must request them explicitly because they don’t come standard. Many contractors discover too late that their policy has gaps exactly when a claim arrives and the insurer denies coverage because the incident falls outside their basic policy language.

Getting Certificates Ready for Client Requests

Requesting certificates of insurance naming clients as additional insured is standard practice, and most Idaho insurers provide digital certificates within hours of purchase. This documentation proves your coverage to clients and keeps you moving forward on bids without delays. Review your coverage annually and immediately after major business changes like hiring additional crew, expanding into new services, or moving to a different county, because your risk profile shifts and your coverage should shift with it.

Final Thoughts

General liability coverage separates contractors who win bids from those who struggle to land quality work. Idaho contractor general liability insurance protects your business from financial devastation after a single job site accident, but only if your limits match what clients actually demand. The $300,000 minimum required for registration is a legal floor, not a practical ceiling-clients now expect $1,000,000 per occurrence and $2,000,000 aggregate before they sign contracts or grant site access.

Start by gathering your basic business information: annual revenue, number of employees, types of construction work, and your typical project values. Request quotes from at least three Idaho-licensed insurers and compare their per-occurrence limits, aggregate limits, deductible options, and whether defense costs are paid outside your policy limit. Ask about endorsements like contractual liability and completed operations coverage that close gaps in standard policies, since The Hartford, ERGO NEXT, and Nationwide all serve Idaho contractors with flexible limits and competitive rates starting around $77 to $98 per month.

Once you select coverage, obtain digital certificates of insurance immediately and keep them accessible for client requests. Certificates naming clients as additional insured are now table stakes on most projects, and delays in providing them cost you opportunities. Contact Matt Anderson Insurance today to discuss your general liability needs and get quotes that position your business for growth and financial security.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.