Idaho Professional Contractor Insurance: Protecting Your Business And Clients

Running a contracting business in Idaho means managing real risks every day. One accident on a job site or a client injury can quickly turn into a lawsuit that threatens everything you’ve built.

At Matt Anderson Insurance, we help Idaho contractors understand why professional contractor insurance isn’t optional-it’s essential. This coverage protects your business, your team, and your clients from the financial damage that comes when things go wrong.

What Your Contractor Insurance Actually Covers

General liability insurance forms the foundation of contractor protection, and Idaho law requires it. This coverage pays for medical bills, legal defense costs, and settlements when someone gets injured on your job site or when your work damages client property. Idaho law requires general liability insurance as mandated by the Idaho Contractors Board, but that bare minimum leaves you exposed on real projects. The Hartford offers rates starting around $77 per month with limits ranging from $300,000 to $2 million per occurrence. Most Idaho contractors carry $1 million per occurrence and $2 million aggregate because client contracts and project requirements commonly demand those higher limits. Bodily injury coverage handles medical costs and lost wages when someone gets hurt, while property damage coverage repairs or replaces client property damaged by your work. Both components include defense costs if a lawsuit arises, protecting your cash flow when claims happen.

Tools and Equipment Need Their Own Protection

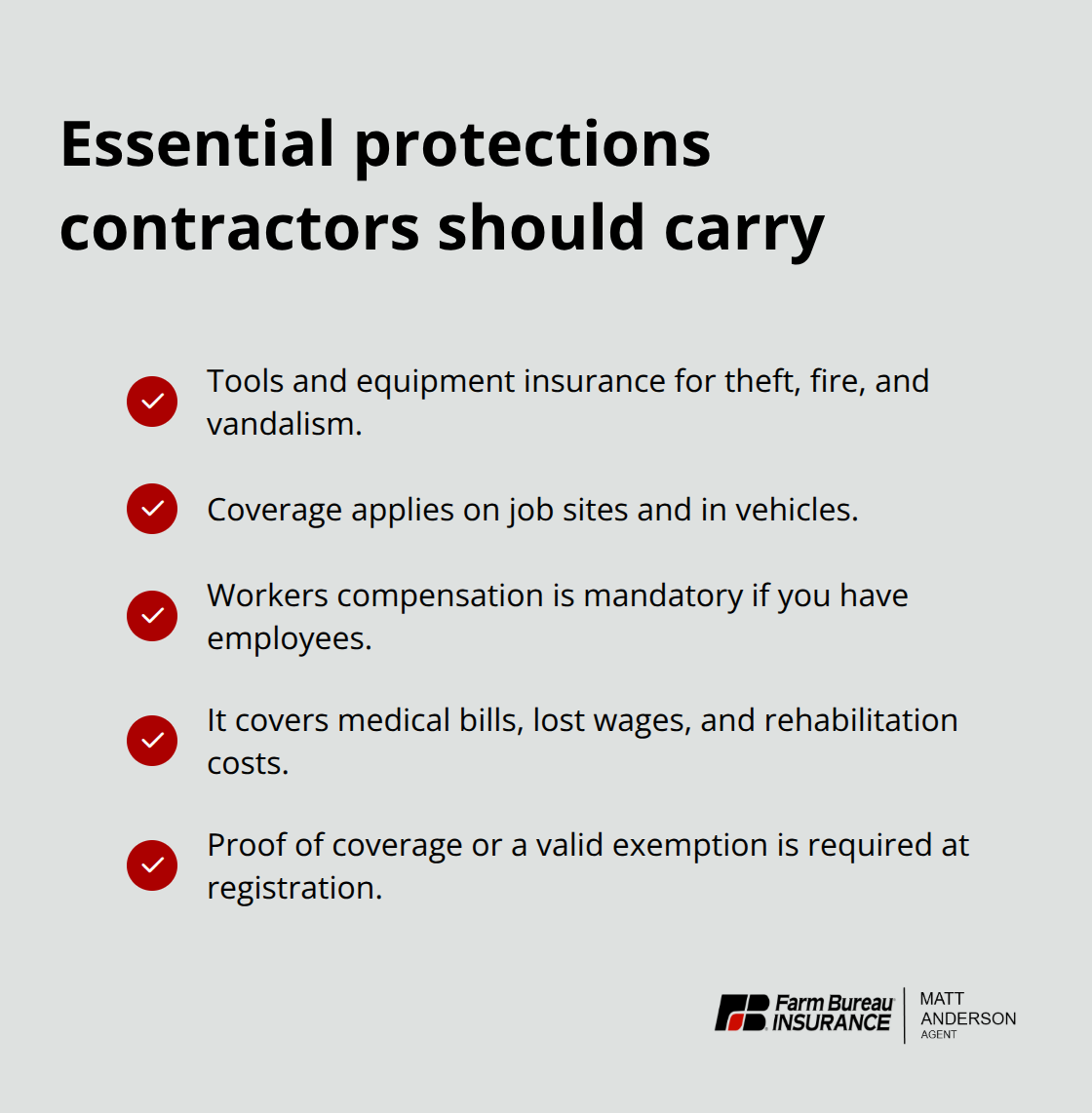

Tools, equipment, and job site materials represent significant financial assets that standard liability policies do not cover. Tools and equipment insurance protects against theft, fire, vandalism, and other losses on the job site or in your vehicle. A single theft can wipe out weeks of profit, especially for specialty trades, which makes this coverage highly recommended. Workers compensation is mandatory in Idaho if you have employees, and it covers medical expenses, lost wages, and rehabilitation costs when a worker gets injured on the job.

You must provide proof of coverage or a valid exemption when you register with the Idaho Contractors Board.

Commercial Auto and Property Coverage

Commercial auto insurance is essential since Idaho minimum requirements are $25,000 bodily injury per person, $50,000 per accident, and $15,000 property damage (though contractors typically carry higher limits). Your vehicles face unique risks on job sites and during transport between locations. Commercial property insurance also protects owned or leased business property from damage or vandalism, which matters when you maintain a shop, office, or storage facility.

Adjusting Coverage as Your Business Grows

When you work on multiple job sites across different counties or expand your service area, your coverage needs change. You should review your policies annually to verify that your endorsements still match your actual risk and that defense costs are structured to maximize your protection. This assessment becomes especially important before you bid on larger projects or hire additional team members.

Why Your Idaho Contractor Registration Requires Real Insurance

The Legal Mandate Behind Coverage Requirements

Idaho law makes this straightforward: if you register as a contractor with the Idaho Contractors Board for projects over $2,000, you must carry general liability insurance with a minimum of $300,000 single limit. The state treats this requirement as a legal mandate tied directly to your ability to operate and collect payment. Without proof of coverage when you register, the Board will not approve your application.

Operating without registration blocks your access to building permits, eliminates your lien rights on unpaid jobs, and exposes you to a misdemeanor charge carrying up to $1,000 in fines or six months in jail under Idaho Code. In fiscal year 2025, the Idaho Department of Professional and Licensing reported 485 contractor complaints, many involving uninsured or underinsured contractors who left clients and subcontractors facing financial loss.

Why the Minimum Coverage Falls Short

The $300,000 minimum Idaho requires proves inadequate for real-world projects, and clients recognize this gap. General contractors and property owners now demand that you name them as additional insured on a certificate of insurance before they sign a contract or cut a check. Most Idaho contractors carry $1 million per occurrence and $2 million aggregate specifically because client contracts and project requirements commonly demand those higher limits. A single accident on a job site can cost thousands in medical bills, legal fees, and settlements-far exceeding the bare minimum. When you bid on projects over $500,000, clients require at least $1 million per occurrence, and larger commercial work routinely calls for $2 million or higher.

Documentation That Wins Contracts

Clients also require proof that your workers compensation coverage remains active and that your general liability policy includes products and completed operations coverage. Without these protections in place and documented, you lose bids, delay project starts, and signal to clients that you lack experience or financial stability. Carrying adequate coverage backed by an Idaho-licensed insurer positions you as a professional and removes obstacles to winning work. The right coverage demonstrates that you take client protection seriously and that you can handle the financial consequences when accidents happen.

Moving Forward With Confidence

Understanding your registration requirements and carrying coverage that exceeds the minimum sets you apart in Idaho’s construction market. The next step involves selecting the right coverage limits and deductibles for your specific trade and project types-a decision that depends on your annual revenue, the size of jobs you typically handle, and the risks unique to your work.

How to Match Coverage Limits to Your Actual Project Risk

Starting with your annual revenue and typical job values gives you a concrete foundation for coverage decisions. If you handle residential remodels under $50,000, a $300,000 limit satisfies legal requirements, but the moment clients demand certificates of insurance naming them as additional insured, you’ll find that bare minimum insufficient. Most Idaho contractors working on projects between $50,000 and $500,000 operate effectively with $1 million per occurrence and $2 million aggregate-the same limits that client contracts and project requirements commonly demand.

Scaling Coverage to Project Size

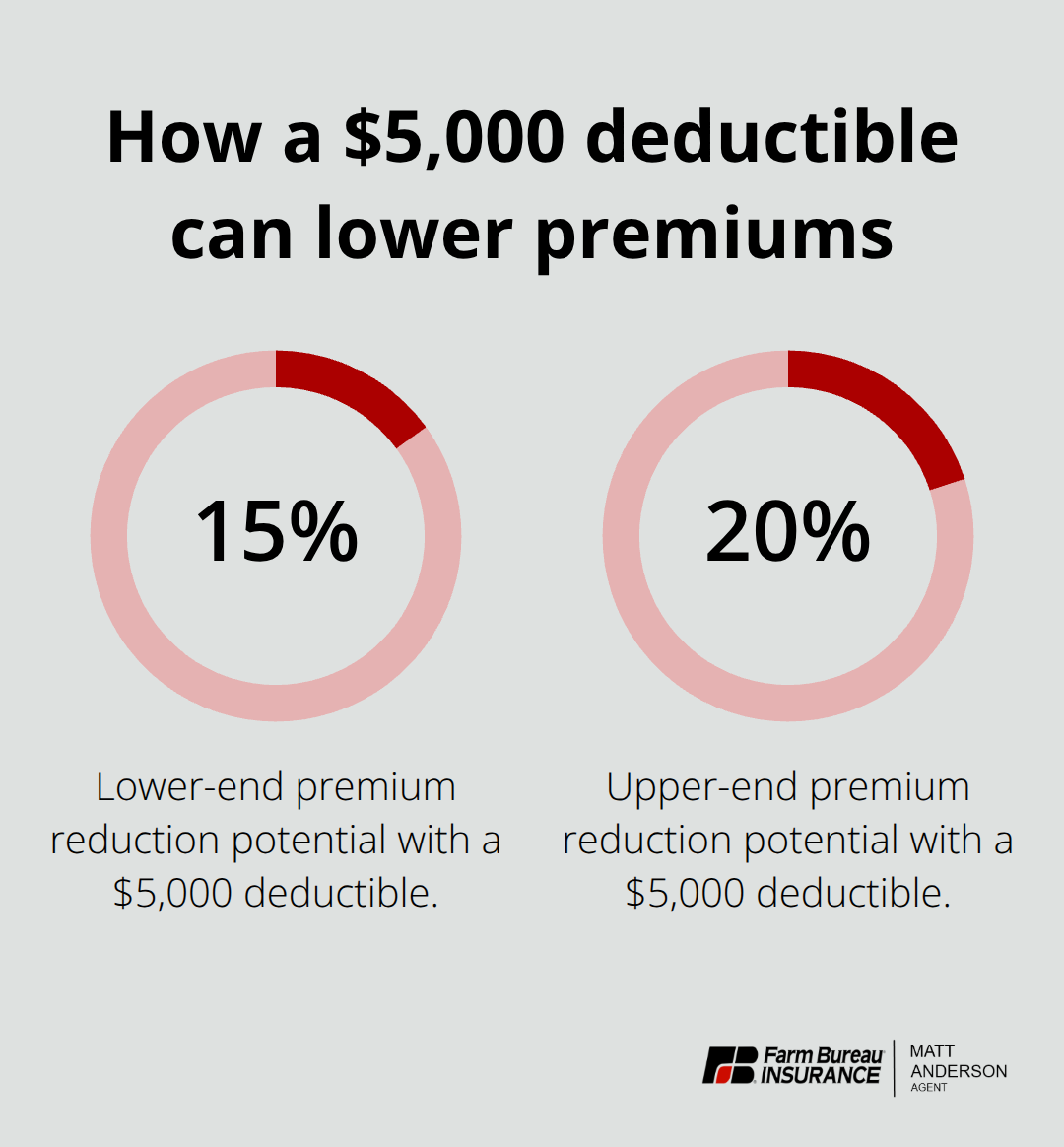

For commercial work or projects exceeding $500,000, clients routinely require at least $1 million per occurrence and often push toward $2 million or higher. The Hartford offers flexible combinations from $300,000 to $2 million per occurrence with aggregate options up to $4 million, allowing you to match your limits to the projects you actually bid. Your deductible choice affects cash flow more than many contractors realize: common Idaho deductibles run $1,000 or $2,500, but selecting a $5,000 deductible can cut premiums by roughly 15 to 20 percent if your business can absorb that cost when a claim occurs.

Understanding Defense Costs and Settlement Funds

Some policies include defense costs inside the coverage limit, while others pay defense costs separately-a critical distinction that determines how much remains available for settlements. Before committing to any quote, compare offers from at least three Idaho-licensed insurers to understand price differences, whether limits align with your project mix, and how each handles defense costs versus settlement funds.

Specialty Trades and Endorsement Gaps

Contractors performing electrical, plumbing, HVAC, or fire sprinkler work may hold licenses from the Division of Occupational and Professional Licenses (DOPL) that exempt them from contractor registration when operating within their scope, but general liability insurance requirements do not disappear. Endorsements such as contractual liability coverage or products-completed operations fill gaps that standard policies leave exposed and often prove worth the additional cost on real job sites.

Adjusting Coverage as Your Business Evolves

When you work across multiple counties or expand service areas, your coverage needs shift, making annual policy reviews essential to verify that coverage limits align with current project values and contractual requirements. Larger projects or new employee hires warrant immediate coverage assessment before you bid or start work, since underestimating risk exposes your business to claims exceeding your limits. We at Matt Anderson Insurance help Idaho contractors evaluate these endorsements and adjust coverage as operations evolve, ensuring protection grows alongside your business rather than lagging behind it.

Final Thoughts

Professional contractor insurance in Idaho protects more than just your business-it protects your clients, your team, and your financial future. The state requires a minimum of $300,000 in general liability coverage to register with the Idaho Contractors Board, but that baseline leaves you exposed on real projects where clients demand $1 million per occurrence and higher limits. One accident costs thousands in medical bills, legal fees, and settlements, making adequate coverage non-negotiable.

Start with an honest assessment of your annual revenue, the typical size of projects you bid, and the specific risks your trade faces. Compare quotes from at least three Idaho-licensed insurers to understand how defense costs are structured, whether limits align with your project mix, and what endorsements fill gaps in standard policies. Your deductible choice matters too-a $5,000 deductible reduces premiums by 15 to 20 percent, but only if your business can absorb that cost when a claim occurs.

Idaho professional contractor insurance extends beyond general liability to include workers compensation (mandatory if you have employees), tools and equipment coverage (which protects against theft and job site losses), and commercial auto insurance (which covers the unique risks your vehicles face during transport and on-site work). As your business grows across multiple counties or takes on larger projects, annual policy reviews keep your coverage aligned with your actual risk. Contact Matt Anderson Insurance today to discuss how comprehensive contractor coverage gives you the confidence to bid bigger projects and operate without financial worry.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.