Idaho Home Insurance Basics: What Every Homeowner Should Know

Homeownership in Idaho comes with real responsibilities, and one of the most important is protecting your investment with solid home insurance. At Matt Anderson Insurance, we’ve helped countless Idaho homeowners understand their coverage options and find policies that actually fit their needs.

This guide walks you through Idaho home insurance basics-from the different types of coverage available to the factors that shape your rates. By the end, you’ll know exactly what to look for when choosing a policy.

What Coverage Do You Actually Need

Dwelling Coverage Protects Your Home’s Structure

Dwelling coverage protects the structure itself-your walls, roof, foundation, built-in appliances, and permanent fixtures. This is non-negotiable if you have a mortgage, since lenders require it. The coverage amount should reflect your home’s replacement cost, not its market value. Many Idaho homeowners underestimate this figure. If your home would cost $350,000 to rebuild from scratch, that’s what your dwelling coverage should cover.

Replacement cost means rebuilding with materials of similar quality today, not what you paid for the house years ago. Construction material matters significantly here. A home built with wood frame construction typically costs less to rebuild than one with concrete or masonry, which can affect your premium. Age also plays a role. Homes built before 1978 may face higher rates due to outdated electrical systems or plumbing that insurance companies view as riskier.

Personal Property Coverage Protects Your Belongings

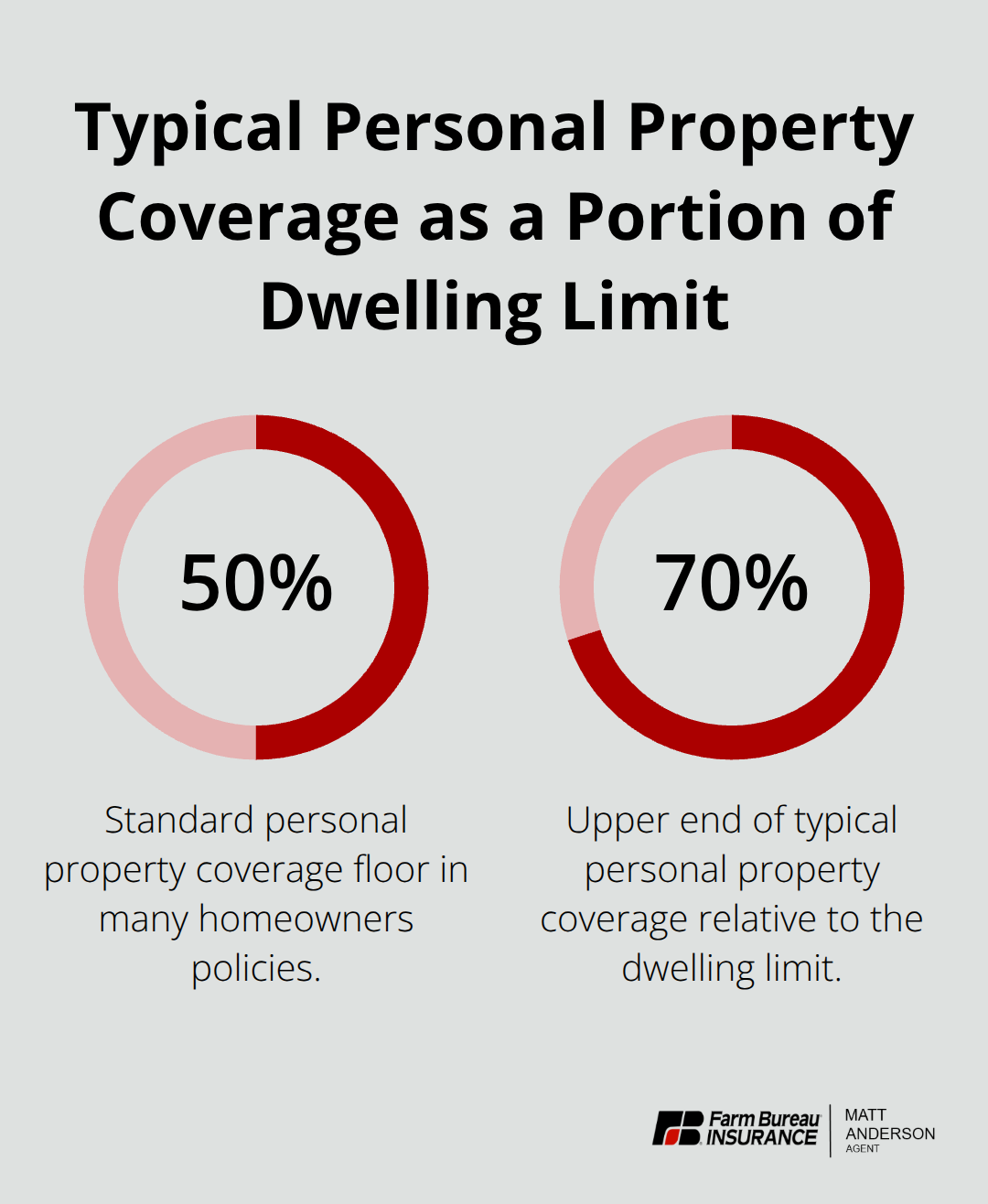

Personal property coverage is where most people get confused, and frankly, this is where inadequate coverage causes real financial pain after a loss. This coverage protects your belongings-furniture, electronics, clothing, kitchen items, everything inside your home. Standard policies typically cover personal property at 50 to 70 percent of your dwelling coverage limit, which sounds reasonable until your house actually burns down and you realize your TV, laptop, clothes, and kitchen aren’t covered fully.

High-value items like jewelry, art, or collectibles often have sub-limits, meaning they’re covered at a reduced amount unless you add a rider. You should document what you own now. Take photos or video of your belongings, note serial numbers for electronics, and keep receipts for expensive items. This inventory becomes invaluable when you file a claim.

Liability Coverage Protects You Against Legal Claims

Liability coverage protects you when someone is injured on your property or you accidentally damage someone else’s property. If a guest slips on your icy walkway in January and breaks their leg, your liability coverage pays their medical bills and any lawsuit damages up to your policy limit. Most policies include medical payments coverage as well, which covers guest injuries without requiring them to prove fault.

This protection is genuinely important in Idaho, where winter conditions create slip-and-fall hazards. Your liability limit should reflect your assets. If you have significant savings or own your home outright, a $300,000 liability limit may not be enough. Consider an umbrella policy for additional protection above your home policy limits-this extra layer of coverage shields you from catastrophic claims that exceed your standard home insurance limits.

What Shapes Your Idaho Home Insurance Premium

Your home’s age, size, and construction materials directly influence what you pay for insurance, and these factors matter more than most homeowners realize. A newer home built in 2015 with modern electrical systems and fire-resistant roofing costs less to insure than a 1970s home with outdated wiring and a standard asphalt roof. Insurance companies view older homes as higher risk because they cost more to repair and carry greater risk of electrical fires or plumbing failures. If your home was built before 1978, expect your premium to reflect that age premium. The size of your home also affects rates-a 3,000-square-foot house costs more to rebuild than a 1,500-square-foot one, so your dwelling coverage limit will be higher, which raises your premium. Construction materials matter significantly too. Homes built with wood frame construction typically have lower premiums than those with concrete or masonry, since wood costs less to rebuild. If your home has a metal roof instead of asphalt shingles, you may qualify for discounts because metal roofs resist hail and wind damage better.

Location and Weather Risk in Idaho

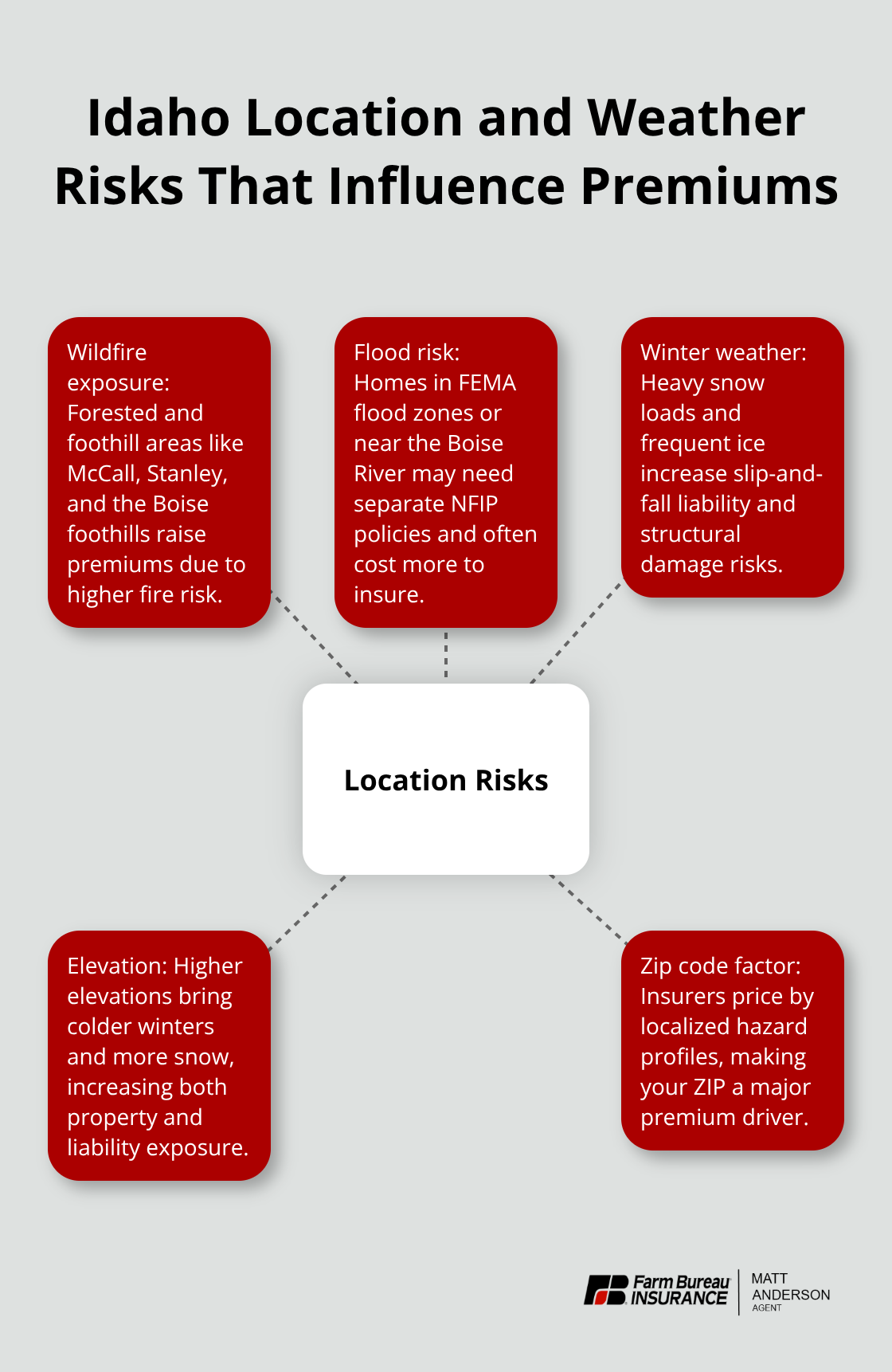

Your zip code ranks as one of the biggest premium drivers in Idaho, particularly if you live in a wildfire-prone area or near flood zones. Nearly all states saw climbing premiums, with Idaho reflecting rising wildfire risk in forested regions. If your home sits in rural areas near forests-places like McCall, Stanley, or the Boise foothills-your premium reflects that exposure. Flood risk varies dramatically across Idaho too.

A home in a FEMA flood zone near the Boise River or in areas with poor drainage costs significantly more to insure, and you’ll likely need a separate flood insurance policy through the National Flood Insurance Program since standard homeowners policies don’t cover flood damage. Winter weather exposure matters as well. Homes in areas with heavy snow loads or frequent ice storms face higher liability premiums because slip-and-fall claims spike during winter months. Elevation also plays a role-higher elevations mean colder winters and more snow, which increases both structural damage risk and liability exposure.

Idaho’s Current Insurance Affordability

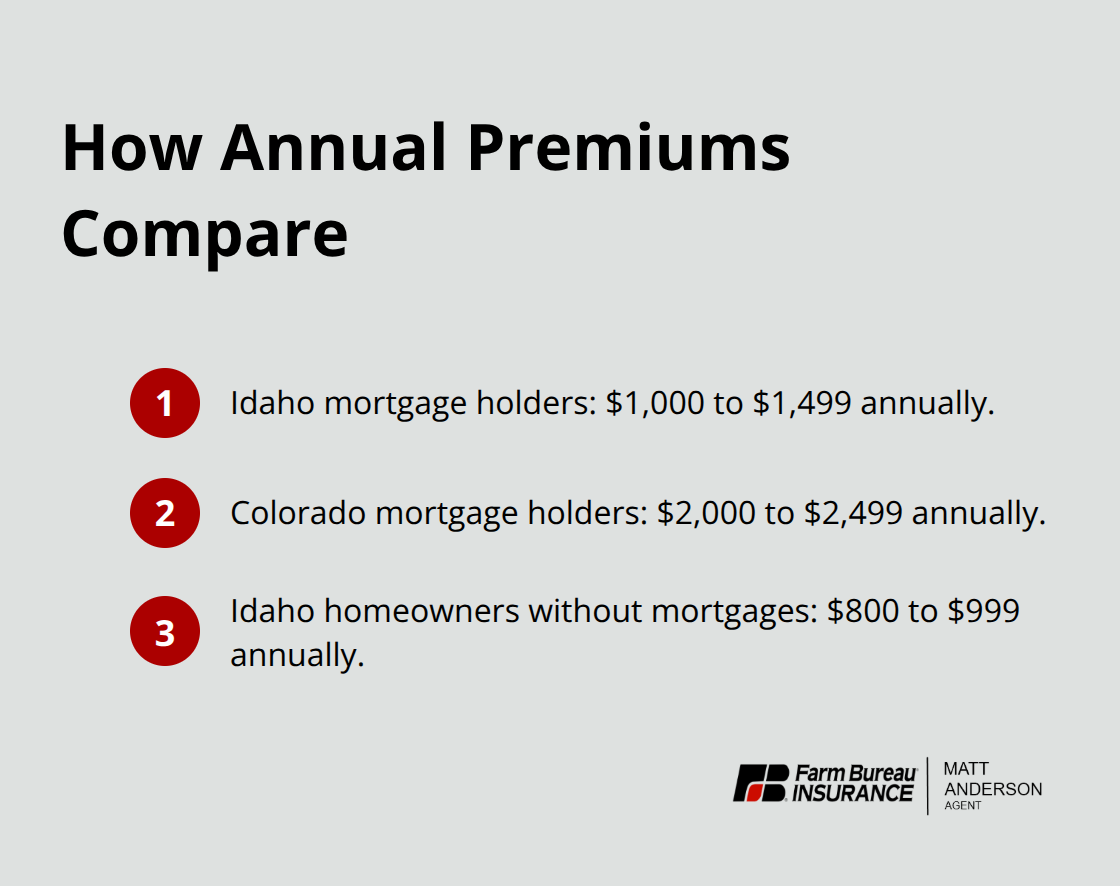

Idaho’s current advantage is that premiums remain among the lowest in the country, with mortgage holders typically paying $1,000 to $1,499 annually according to U.S. Census Bureau data, significantly lower than neighboring states like Colorado where mortgage holders pay $2,000 to $2,499. This affordability won’t last forever if wildfire and flood risks continue accelerating, so locking in competitive rates now makes financial sense. Homeowners without mortgages pay even less-typically $800 to $999 annually-though they still need coverage to protect their investment.

Claims History and Credit Score Impact

Your personal claims history and loyalty directly affect whether insurers will cover you and at what price. If you filed three homeowners claims in the past five years, expect higher premiums or possible policy denial from some insurers. Insurance companies view frequent claims as a signal that you’re statistically more likely to file again. Even one claim for water damage or theft can raise your premium 10 to 20 percent for three to five years. Your credit score influences your premium too, though many homeowners don’t realize this connection. Insurers use credit-based insurance scores to assess financial responsibility, and lower scores result in higher premiums. If your credit score is below 650, you could pay 30 to 40 percent more for the same coverage compared to someone with a score above 750.

Strategies to Lower Your Premium

If you have a poor claims history or low credit score, you have options. Shopping around matters enormously because different insurers weight these factors differently. Some companies are more forgiving of older claims or credit issues than others. Bundling your auto and home insurance can lower your overall premium by 15 to 25 percent, which helps offset rate increases from claims history. Improving your credit score through on-time payments and reducing debt takes time but will directly lower your insurance costs over the long term. These rate factors all work together, which means understanding how your home’s characteristics, location, and personal history affect your premium puts you in control when it’s time to choose the right policy.

How to Choose the Right Coverage Amount and Get Multiple Quotes

Calculate Your Home’s True Replacement Cost

Picking the correct dwelling coverage amount stops most Idaho homeowners from making expensive mistakes. Start with your home’s actual replacement cost, not its market value or what you paid for it years ago. If your house sold for $400,000 but would cost $450,000 to rebuild today with current labor and materials, that $450,000 is your target dwelling coverage limit. Construction costs in Idaho have climbed significantly, with average costs ranging from $115 to $460 per square foot depending on home type and finishes. Contact local builders or use online replacement cost estimators to get a realistic figure for your specific home size, materials, and local building codes.

Compare Quotes from Multiple Insurers

Once you know your replacement cost number, obtain quotes from at least three different insurers because premiums vary wildly for identical coverage. One company might charge $1,100 annually while another charges $1,400 for the same dwelling limit and personal property protection-that $300 difference adds up fast over years of payments. When comparing quotes, verify that each one covers the same dwelling amount, personal property limit, liability limit, and deductible so you’re actually comparing apples to apples. Some insurers are more aggressive on pricing for newer homes or homes with protective devices like security systems, so shopping around reveals which company values your specific situation.

Stack Discounts to Maximize Savings

Bundling your home and auto insurance typically saves 15 to 25 percent on your total premium, which makes this strategy worth serious consideration. If you currently have auto insurance elsewhere, moving both policies to one carrier usually triggers substantial discounts that individual policies won’t match. Beyond bundling, ask about discounts for protective devices like smoke detectors, security systems, or smart home technology that reduces loss risk. Some insurers offer loyalty discounts if you stay with them for multiple years, welcome discounts for new customers, or good payer discounts if you pay your premium in full rather than monthly installments. These discounts can stack, so a homeowner with a security system, bundled policies, and a clean payment history might receive 30 to 40 percent off the base premium.

Verify Coverage Matches Your Needs

Don’t accept the first quote you receive-the combination of choosing the right coverage amount, comparing multiple insurers, and stacking available discounts can easily save you $200 to $500 annually while protecting you if disaster strikes. At Matt Anderson Insurance, we help Idaho homeowners find these opportunities through our Farm Bureau affiliation, which means we offer comprehensive personal and commercial coverage under one roof. The effort you invest in this process directly translates to both lower costs and stronger protection for your Idaho home.

Final Thoughts

Idaho home insurance basics come down to three core decisions: selecting the right coverage amounts, understanding what drives your premium, and comparing quotes from multiple insurers. Dwelling coverage should match your home’s replacement cost, not its market value, while personal property coverage protects your belongings and liability protection shields you from catastrophic claims. Your home’s age, location, and claims history directly affect what you pay each month.

Calculate your home’s true replacement cost using local builder estimates or online tools, then obtain quotes from at least three different insurers to verify they cover identical limits and deductibles. Stack available discounts through bundling, protective devices, and loyalty programs to reduce your premium by hundreds of dollars annually. Idaho’s current affordability won’t last forever as wildfire and flood risks accelerate, so locking in competitive rates now protects your financial future.

We at Matt Anderson Insurance stand ready to help you navigate this process with quotes tailored to your Idaho home and situation. Contact us today to work with licensed agents who understand Idaho’s specific risks and coverage needs. Your investment in understanding these basics today pays dividends through lower premiums and stronger protection for years to come.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.