Idaho Contractor Insurance Costs: What It Really Takes to Protect Your Trade

Idaho contractor insurance costs vary wildly depending on your trade, revenue, and safety record. Most contractors underestimate what they actually need to pay for proper coverage.

We at Matt Anderson Insurance work with Idaho contractors every day who are shocked to learn how much their premiums could drop with the right strategy. This guide breaks down exactly what drives your costs and how to cut them without cutting corners.

What Drives Your Contractor Insurance Costs

Your Trade Determines Your Base Price

Your trade determines your insurance cost more than anything else. A roofer in Boise pays dramatically more than a finish carpenter doing similar-sized projects because roofing carries inherent risk that insurance companies price accordingly. According to the National Council on Compensation Insurance and Idaho Department of Insurance data as of 2026, general contractors pay $1,000–$2,600 annually for general liability, while roofers pay $1,600–$4,100 for the same coverage. HVAC technicians land at $800–$2,000, electricians at $750–$1,900, and plumbers at $800–$2,100.

Workers’ compensation rates per $100 of payroll tell the same story. Roofers face $7.00–$11.00, general contractors $4.00–$6.00, and electricians the lowest at $2.50–$3.50. This means a roofer with five employees and $150,000 annual payroll pays roughly $875–$1,375 monthly for workers’ comp alone, while an electrician with identical payroll spends $312–$438. Your classification code at registration determines which rate table applies, so verify the Idaho Contractors Board assigned your correct trade type when you register for projects over $2,000.

Business Size and Payroll Push Costs Higher

Your payroll size drives the second layer of cost. Solo operators typically pay $33–$62 monthly for general liability, while contractors with 2–5 employees jump to $62–$158 monthly, and those with 6–15 employees reach $158–$417 monthly. Larger crews mean higher total payroll, which multiplies your workers’ comp exposure across more workers and more hours on job sites.

Claims History and Safety Records Shape Your Rate

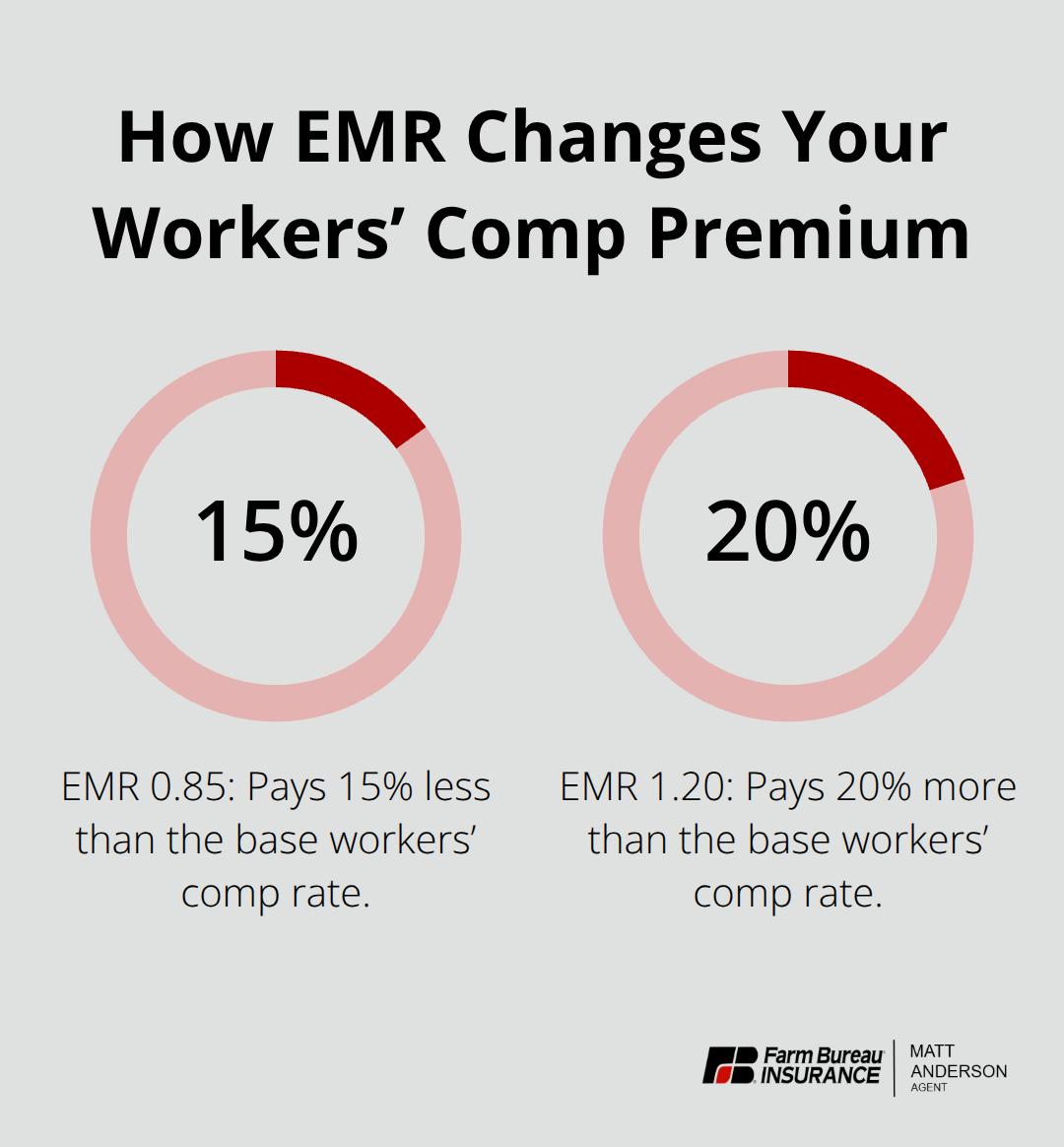

The Experience Modification Rate, or EMR, is the insurance industry’s way of adjusting your workers’ compensation premium based on your actual claims history. An EMR of 0.85 reduces your base rate by 15 percent, while an EMR of 1.20 increases it by 20 percent-meaning a clean safety record saves thousands annually on a mid-sized crew. Contractors with prior claims don’t automatically lose coverage, but carriers limit options and raise premiums significantly. One serious claim can keep your EMR elevated for three to five years, making safety investments pay immediate financial returns.

Smart Shopping Cuts Real Money

Quotes from multiple carriers at renewal matter because rates shift annually and stale pricing costs money. Bundling general liability, workers’ comp, commercial auto, and tools coverage with a single carrier typically yields 10–20 percent in multi-policy discounts, which adds up to real savings on a $3,000–$8,000 annual insurance bill. These three cost drivers-trade, payroll, and safety record-set your baseline, but how you shop and structure your policies determines whether you pay full price or find meaningful savings.

How to Cut Your Contractor Premiums Without Sacrificing Protection

Bundle Policies to Unlock Immediate Savings

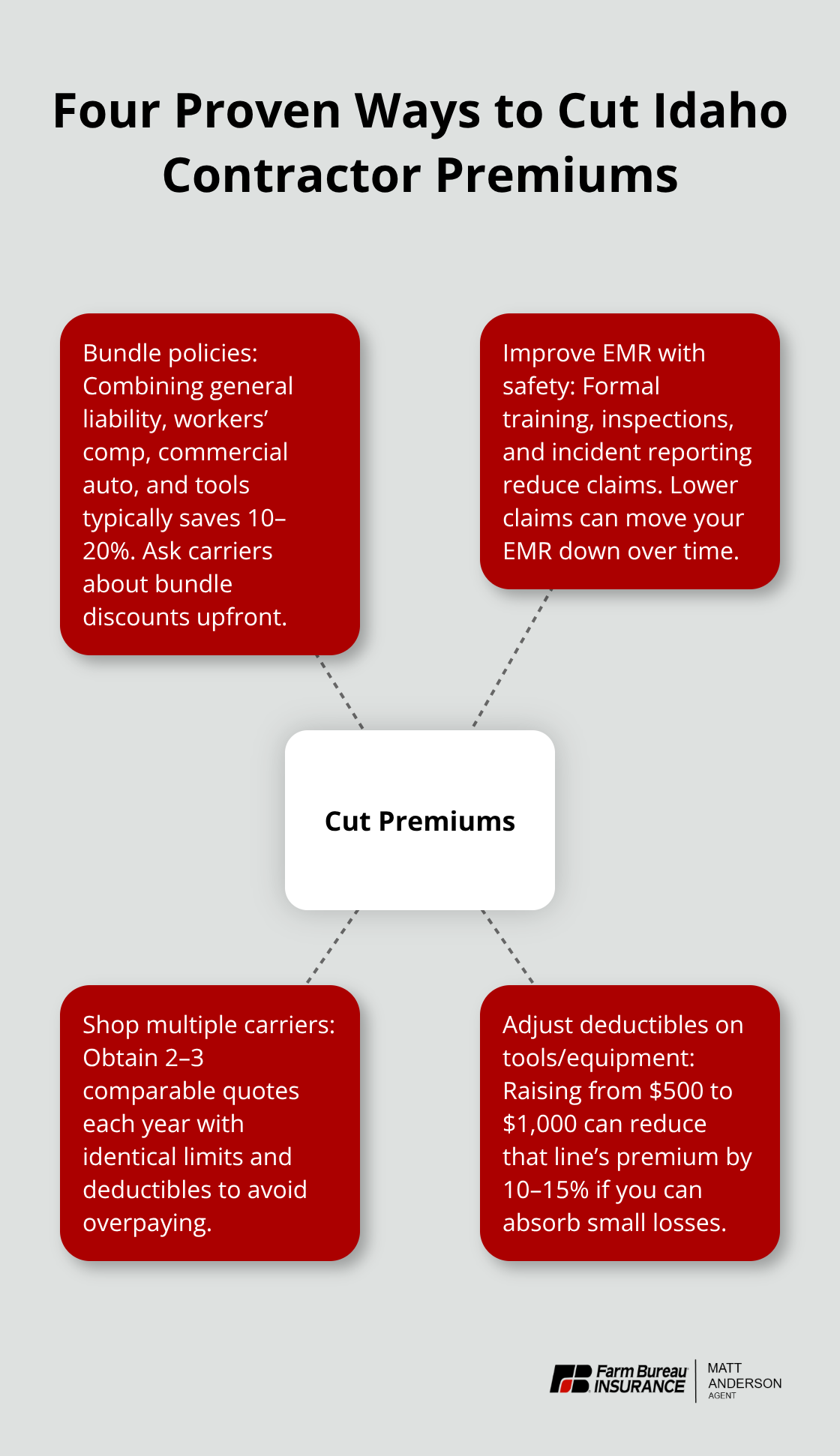

Bundling policies with one carrier is the fastest way to lower your bill, and the numbers are concrete. According to the National Council on Compensation Insurance and Idaho Department of Insurance data, contractors who combine general liability, workers’ compensation, commercial auto, and tools coverage with a single insurer typically save 10–20 percent on their total annual premium. For a contractor paying $5,000 annually across multiple policies, that discount translates to $500–$1,000 back in your pocket every year. The discount works because insurers reduce their acquisition and administrative costs when they write multiple lines for one customer. When you shop at renewal, ask carriers upfront what bundle discounts apply before comparing final quotes, since some agencies highlight bundled pricing only after you ask.

Lower Your EMR Through Documented Safety Programs

Your safety record directly controls your workers’ compensation cost through your Experience Modification Rate, and improving it delivers faster savings than almost any other strategy. A contractor with five employees and a 0.85 EMR pays 15 percent less than the base rate, while one with a 1.20 EMR pays 20 percent more. Over a year on a $600 monthly workers’ comp premium, that gap equals $1,800 in annual cost difference.

Documented safety programs-OSHA training, job site inspections, incident reporting systems-reduce claims frequency and push your EMR down over time. The Idaho Industrial Commission and your insurance carrier both track these metrics, so investing in formal safety training for your crew and maintaining written safety procedures directly lowers your insurance cost and improves your bid eligibility for commercial and government projects. One serious claim can elevate your EMR for three to five years, making prevention far cheaper than paying claims.

Shop Multiple Carriers Every Year

Renew your quotes every year, not just when your policy expires. Rates shift annually based on market conditions and your updated claims history, and contractors who shop only at expiration often overpay by hundreds of dollars. Obtain 2–3 quotes from different carriers and compare them side by side, specifying identical coverage limits and deductibles so the quotes are truly comparable. When comparing, ask each carrier to calculate what your premium would be with a higher deductible on lower-risk lines like tools and equipment coverage.

Raising your deductible from $500 to $1,000 on equipment coverage can reduce that line’s premium by 10–15 percent if you can absorb small losses out of pocket.

Adjust Deductibles on Lower-Risk Coverage

Strategic deductible placement saves money without exposing your business to unmanageable risk. Tools and equipment coverage, for instance, protects against theft and damage at job sites-losses you can often predict and budget for. Commercial auto coverage, by contrast, carries unpredictable liability exposure that warrants a lower deductible. Idaho contractor insurance costs remain below average nationally, but that advantage disappears if you accept the first quote you receive. Shop aggressively at renewal and you’ll find real savings that compound year after year.

The coverage types you select matter just as much as the price you pay for them. Not all contractors need identical protection, and selecting the right mix prevents both gaps in coverage and wasted premium dollars.

Coverage Types Every Idaho Contractor Must Have

General Liability: Your First Line of Defense

General liability covers third-party bodily injury and property damage claims-the contractor who accidentally damages a homeowner’s deck or causes an injury on a job site. Idaho law doesn’t mandate general liability for registration, but contractors must have insurance as part of the registration process. This isn’t a suggestion; it’s the entry price to operate legally. General liability premiums range from $400–$750 annually for solo operators to $1,000–$2,600 for general contractors managing larger crews and multiple projects. The coverage must include products and completed operations protection to address claims that arise after project completion, which matters because defects or injuries tied to your finished work can surface months later.

Workers’ Compensation: Mandatory Protection for Your Crew

Workers’ compensation is mandatory in Idaho for any business with employees, and the Idaho Industrial Commission administers the program through private insurers, the State Insurance Fund, or approved self-insurance arrangements. The cost depends entirely on your payroll, your trade classification, and your Experience Modification Rate. A general contractor with five employees and $150,000 annual payroll pays $500–$750 monthly, while an electrician with identical payroll and headcount pays $312–$438 monthly because electrical work carries lower injury frequency than general contracting. These figures come from the National Council on Compensation Insurance and Idaho Department of Insurance data as of 2026. The rate per $100 of payroll is your multiplier-general contractors face $4.00–$6.00, electricians $2.50–$3.50, and roofers the highest at $7.00–$11.00. Verify your classification code when you register because misclassification can cause significant overcharges at audit time.

Tools and Equipment Coverage: Protecting Your Assets

Tools and equipment coverage protects your hand tools, power equipment, and job site gear from theft, fire, and vandalism-losses that happen regularly and drain cash flow when you replace stolen equipment mid-project. Coverage typically costs $250–$1,000 annually depending on your equipment value and deductible choice, and raising your deductible from $500 to $1,000 cuts the premium by 10–15 percent if your cash reserves can absorb small losses. When you bundle general liability with other policies, your total premium drops 10–20 percent, so the actual cost per line becomes far lower than shopping coverage types separately.

Final Thoughts

Idaho contractor insurance costs reflect your trade, payroll, and safety decisions-factors that you can influence through smart planning and active management. Your baseline premium depends on whether you’re a roofer or electrician, but your actual cost depends on whether you bundle policies, maintain a clean safety record, and shop multiple carriers annually. A contractor who implements these three strategies pays substantially less than one who accepts the first quote and spreads coverage across different insurers.

Getting actual quotes tailored to your specific situation reveals your true Idaho contractor insurance costs far better than industry averages. Your safety investments, bundling options, and deductible choices create real savings that generic estimates miss entirely. We at Matt Anderson Insurance work with Idaho contractors to structure policies that meet your protection needs while maximizing discounts and keeping you compliant with state registration requirements.

Contact Matt Anderson Insurance today to get a quote and see what your actual costs look like with the right strategy in place.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.