Homeowners Insurance Bundling Idaho: Discounts For Bundled Coverage

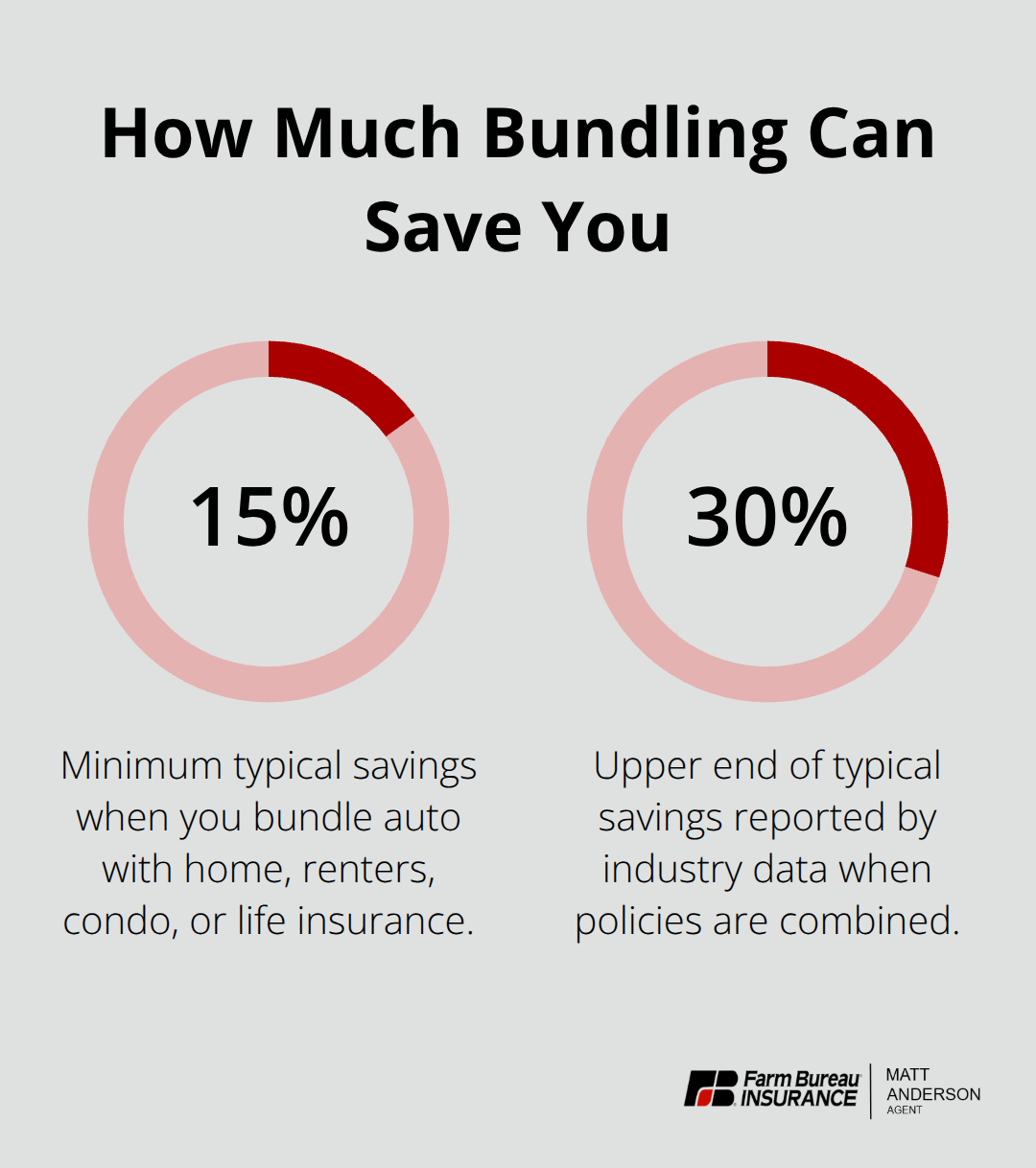

Bundling your homeowners and auto insurance in Idaho can cut your premiums significantly. Most insurers offer discounts between 15% and 25% when you combine policies, and we at Matt Anderson Insurance see these savings add up fast for families across the state.

The key is knowing which combinations work best for your situation and how to maximize every available discount. This guide walks you through real savings examples, popular bundle options, and why working with a local agency makes the difference.

How Much Can You Actually Save by Bundling

Bundling works because insurers reward customer loyalty with discounts that stack on top of your base premium. When you combine homeowners and auto coverage with the same carrier, you typically save with a bundling discount, though the actual dollar amount depends entirely on your location, home value, and driving history. In Idaho specifically, bundling saves homeowners roughly 17% overall according to rate data, but this varies significantly by ZIP code and insurer.

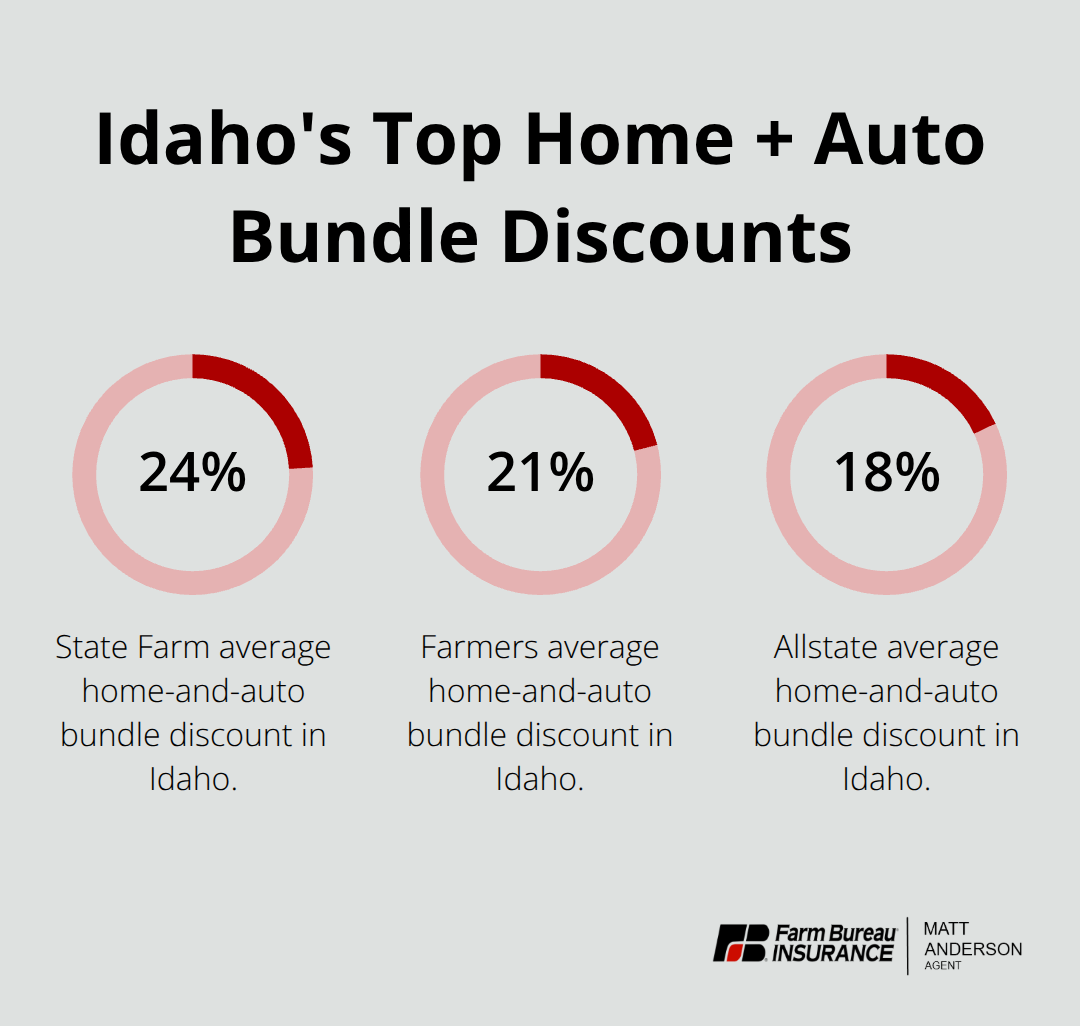

State Farm, Farmers, and Allstate Lead Idaho Discounts

State Farm offers the largest Idaho home-and-auto bundle discount on average at about 24%, cutting a typical combined premium from $2,748 to $2,084 annually. Farmers yields an average bundle discount of around 21%, lowering a typical combined rate from $3,867 to about $3,073.

Allstate shows an average bundle discount of 18% in Idaho, reducing the pre-discount $5,221 to $4,256. Idaho Farm Bureau provides an average of 10% bundle discount but includes benefits like a single renewal date and the same claims team, which simplifies management even if the percentage is lower.

The critical point here is that you should compare final combined annual premiums after discounts, not just the discount percentage itself, because base rates differ dramatically between carriers. A higher percentage from one insurer may not beat a lower percentage from another when you look at what you actually pay.

Your ZIP Code Determines a Significant Portion of Your Premium

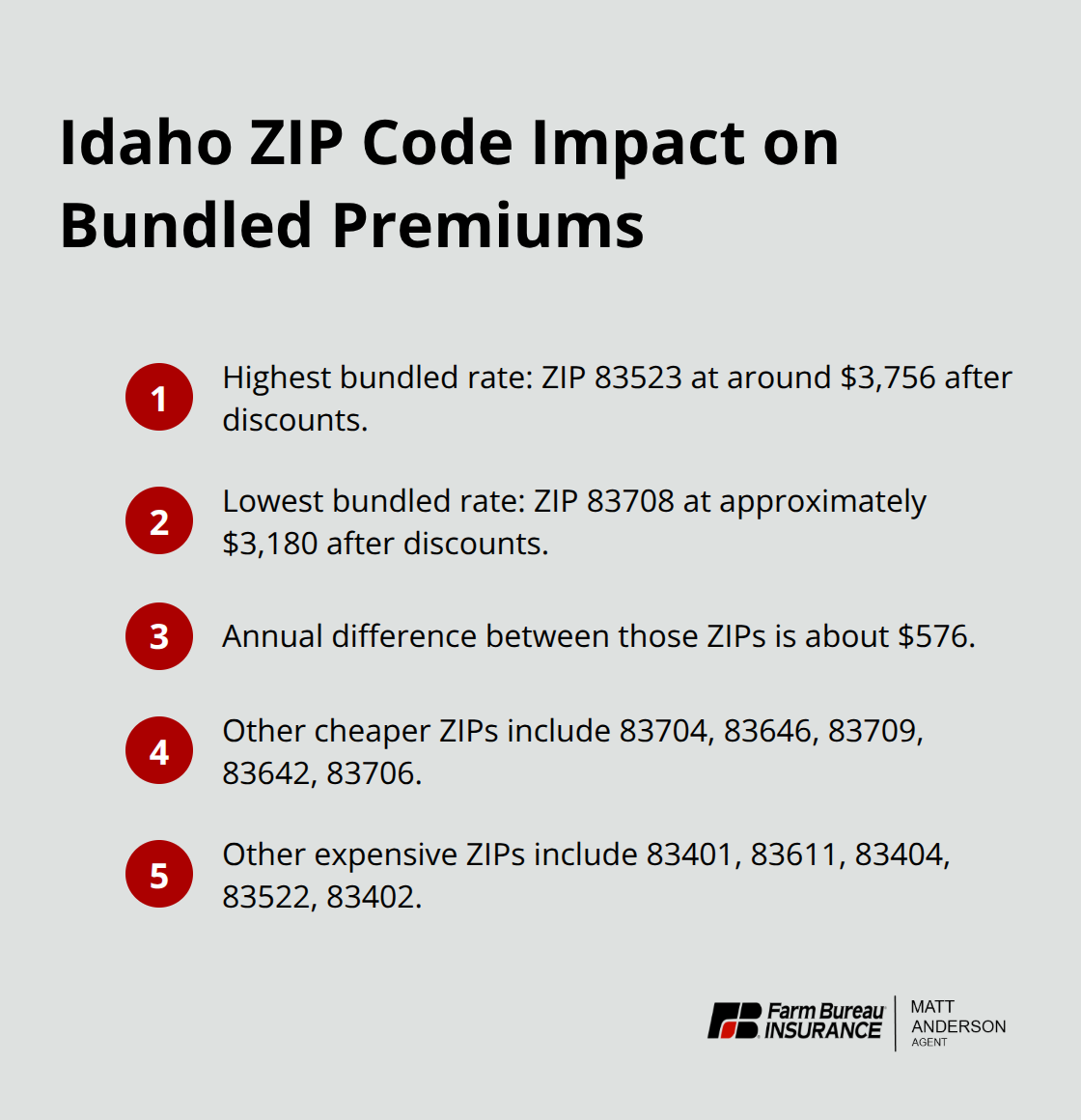

Where you live in Idaho determines a significant portion of your premium before any discount applies. ZIP code 83523 carries the highest bundled rates in the state at around $3,756 after discounts, while ZIP code 83708 is the cheapest at approximately $3,180. This $576 annual difference reflects local risk factors (weather exposure, crime rates, distance to fire hydrants, fire department quality, and rebuilding costs).

If you move within Idaho, you must compare bundle rates for your new ZIP code before finalizing your move, since location can shift your savings dramatically. The cheapest Idaho ZIPs for bundled coverage include 83708, 83704, 83646, 83709, 83642, 83706, 83716, 83712, 83725, and 83702. The most expensive include 83523, 83401, 83611, 83404, 83522, 83402, 83406, 83217, 83467, and 83245. These differences mean that bundling savings depend on where your property sits, not just on which insurer you choose.

Real Numbers Show Why Bundling Wins Over Separate Policies

A homeowner paying $1,510 annually for homeowners coverage plus $1,200 for auto insurance pays $2,710 separately. With a 17% bundling discount applied to the combined premium, that same coverage drops to approximately $2,249, saving $461 per year or about $3,827 over a decade. If you qualify for a carrier offering a 24% discount like State Farm, your savings increase substantially.

The gap widens further when you factor in loyalty discounts, claim-free discounts for years without claims, or discounts for safety features like home security systems and upgraded electrical systems. The reality is that a lower discount percentage from one carrier sometimes beats a higher percentage from another due to different base rates. Shopping around with a local agent who can run quotes across multiple carriers is essential to find your best rate.

What Happens When You Add More Coverage

Most Idaho families stop at home and auto bundling, but you can stack additional savings when you add umbrella coverage or other policies to your bundle. Each additional policy you add to your existing bundle typically qualifies for multi-policy discounts that compound your overall savings. The more you consolidate with a single carrier, the more negotiating power you gain to tailor coverage to your specific needs and risk profile.

Which Bundle Options Work Best for Idaho Families

Home and auto insurance bundles remain the most practical choice for Idaho families because they address your two largest insurance expenses simultaneously. State Farm, Farmers, and Allstate dominate this market in Idaho with competitive discounts, but the real advantage comes from consolidating your renewal dates, claims processes, and billing into a single carrier. When you bundle home and auto, you simplify your annual insurance management significantly-one renewal notice instead of two, one customer service number for questions, and one claims team if something happens. Bundling home and auto translates to real dollars that add up year after year, especially when you factor in loyalty discounts that many carriers apply after you stay bundled for multiple years.

Adding Umbrella Coverage Multiplies Your Savings

Umbrella insurance protects your personal assets if a liability claim exceeds your home or auto policy limits, and bundling it with your existing home and auto coverage qualifies you for additional multi-policy discounts that most Idaho families overlook. A homeowner with a $1 million umbrella policy bundled with home and auto might save 5% to 10% on the umbrella premium alone, plus potentially higher discounts on the underlying policies. This coverage costs roughly $150 to $300 annually for $1 million in protection but becomes significantly cheaper when bundled. Idaho families with substantial assets, second properties, or regular social gatherings should strongly consider umbrella coverage-the extra layer of liability protection justifies the cost, and bundling makes it affordable.

Farm and Commercial Coverage for Rural Idaho Properties

Rural Idaho properties with farm operations or rental income need specialized bundles that standard home and auto policies do not cover. Farm and commercial bundles combine personal coverage with business protection, addressing equipment, livestock, farm structures, and liability exposure unique to agricultural operations. A farm bundling package might include homeowners coverage, farm auto, equipment coverage, and commercial liability in one consolidated policy, delivering discounts that standalone policies cannot match. Rental properties similarly benefit from bundled commercial coverage paired with your personal policies-you consolidate management and gain discounts while protecting both your primary residence and income-producing assets with a single carrier.

How Local Agencies Identify Your Best Bundle Options

Local Idaho agencies compare multiple carriers to identify which bundle combinations save you the most money based on your specific situation. An independent agent reviews your home value, driving history, farm operations (if applicable), and asset level to recommend the right coverage options and carrier. This personalized approach reveals discounts you might miss if you shop with a single large insurer, since different carriers excel at different bundle combinations. The agent handles all the paperwork, coordinates your policies, and serves as your single point of contact when you need to make changes or file a claim-a significant advantage over managing multiple carriers on your own.

How to Maximize Your Idaho Bundle Savings

Annual Reviews Reveal Hidden Discounts

You must review your coverage each year before renewal if you want to keep your bundling discount competitive. Most Idaho homeowners set their policies and forget them, missing out on additional discounts that emerge as your life changes or as carriers adjust their offerings. When you review your bundle annually, you identify new discounts for safety features you’ve added (security systems, upgraded electrical wiring, new roofs with impact-resistant materials), claim-free years that qualify for loyalty reductions, or changes in your home value that affect coverage levels. Carriers like State Farm, Farmers, and Allstate regularly introduce new discount categories, and a quick annual conversation with your agent reveals which ones apply to your specific situation.

Your agent identifies these opportunities during your renewal conversation, ensuring you capture every discount available to your situation.

Loyalty Discounts Compound Over Time

Multi-policy loyalty discounts compound your savings significantly when you stay bundled with the same carrier for multiple years. Most carriers reward customers who maintain continuous bundled coverage with the same provider with additional percentage reductions on top of your base bundling discount. A homeowner receiving an initial 18% bundling discount from Allstate might earn an additional 5% loyalty discount after five years of continuous bundled coverage, effectively lowering their total discount to approximately 23%.

Some carriers also offer claim-free discounts that apply when you haven’t filed a homeowners or auto claim for three to five years, adding another layer of savings for responsible homeowners. The strategy here is straightforward: stay bundled with a single carrier long enough to accumulate loyalty benefits, since switching carriers resets these discounts to zero.

Local Agents Manage Your Bundle Strategically

A local Idaho agency gives you access to carriers offering competitive loyalty programs while ensuring your coverage stays aligned with your actual needs. Your agent reviews your bundle annually, confirms you’re receiving every discount you qualify for, and coordinates all policy changes without the administrative burden of managing multiple carriers yourself. This ongoing relationship transforms bundling from a one-time discount into a dynamic savings strategy that grows stronger each year you maintain your coverage.

Final Thoughts

Homeowners insurance bundling in Idaho works best when you have an agent who understands your state’s specific risks and coordinates coverage across multiple carriers on your behalf. Idaho faces winter hazards like frozen pipes and ice dams, summer risks including thunderstorms and hail, and wildfire exposure in certain regions-each factor affects your premium and coverage needs differently depending on where you live. A local agent knows which carriers offer the strongest coverage for these risks, which discounts apply to your specific situation, and how your ZIP code influences your final rate.

When you bundle with a local agency, you receive streamlined claims support across all your policies. Instead of contacting separate carriers when something happens, you work with one team that coordinates your homeowners claim, auto claim, or umbrella claim through a single process. This coordination matters when you face a major loss-your agent ensures nothing falls through the cracks and that all your policies work together to cover your damages completely.

The real advantage of working with a local Idaho agency is having one point of contact for every insurance question you encounter. Whether you need to adjust your coverage limits, add a new vehicle, report a claim, or explore additional discounts, you reach out to the same person who knows your complete insurance picture. Contact Matt Anderson Insurance to review your homeowners insurance bundling Idaho options and discover how much you can save by consolidating your coverage with a local agency that understands your state.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.