Idaho Homeowners Insurance Policy: What It Covers And How To Choose

Homeowners in Idaho face unique insurance decisions based on where they live and what they own. An Idaho homeowners insurance policy protects your home, belongings, and finances from unexpected losses-but only if you understand what’s actually covered.

We at Matt Anderson Insurance help homeowners navigate these choices every day. This guide breaks down your coverage options and shows you how to pick the right protection for your situation.

What Your Idaho Homeowners Policy Actually Covers

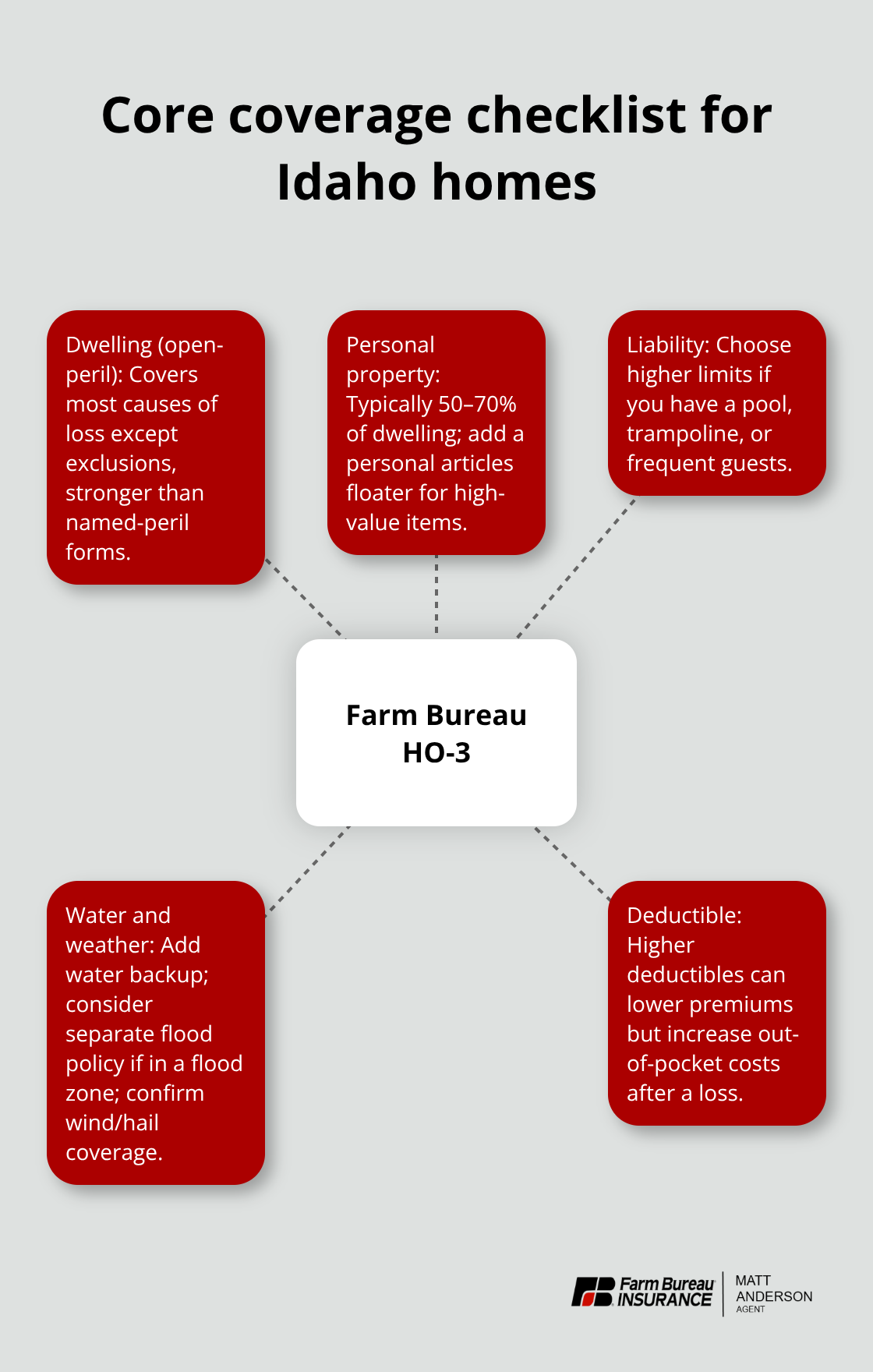

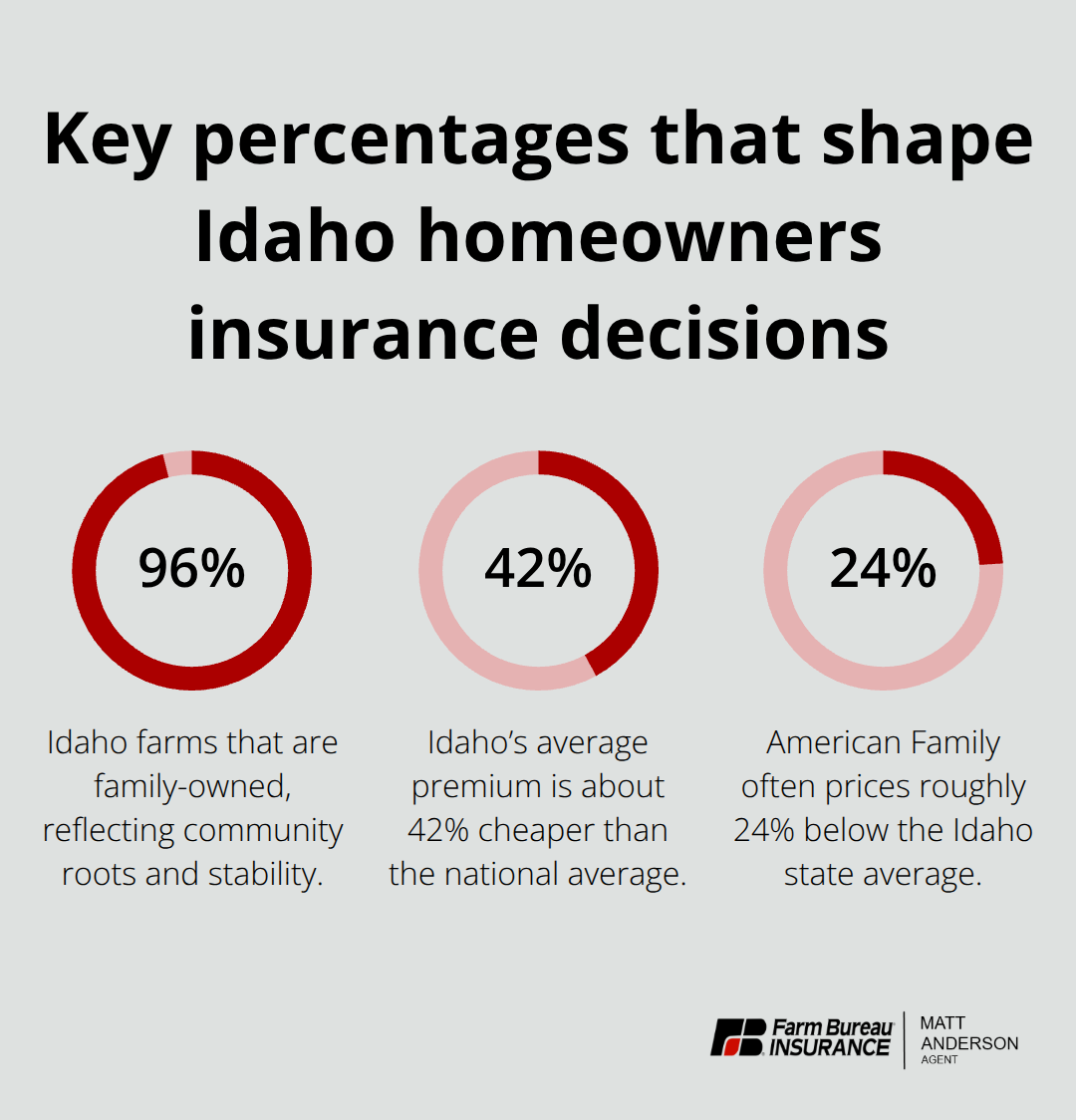

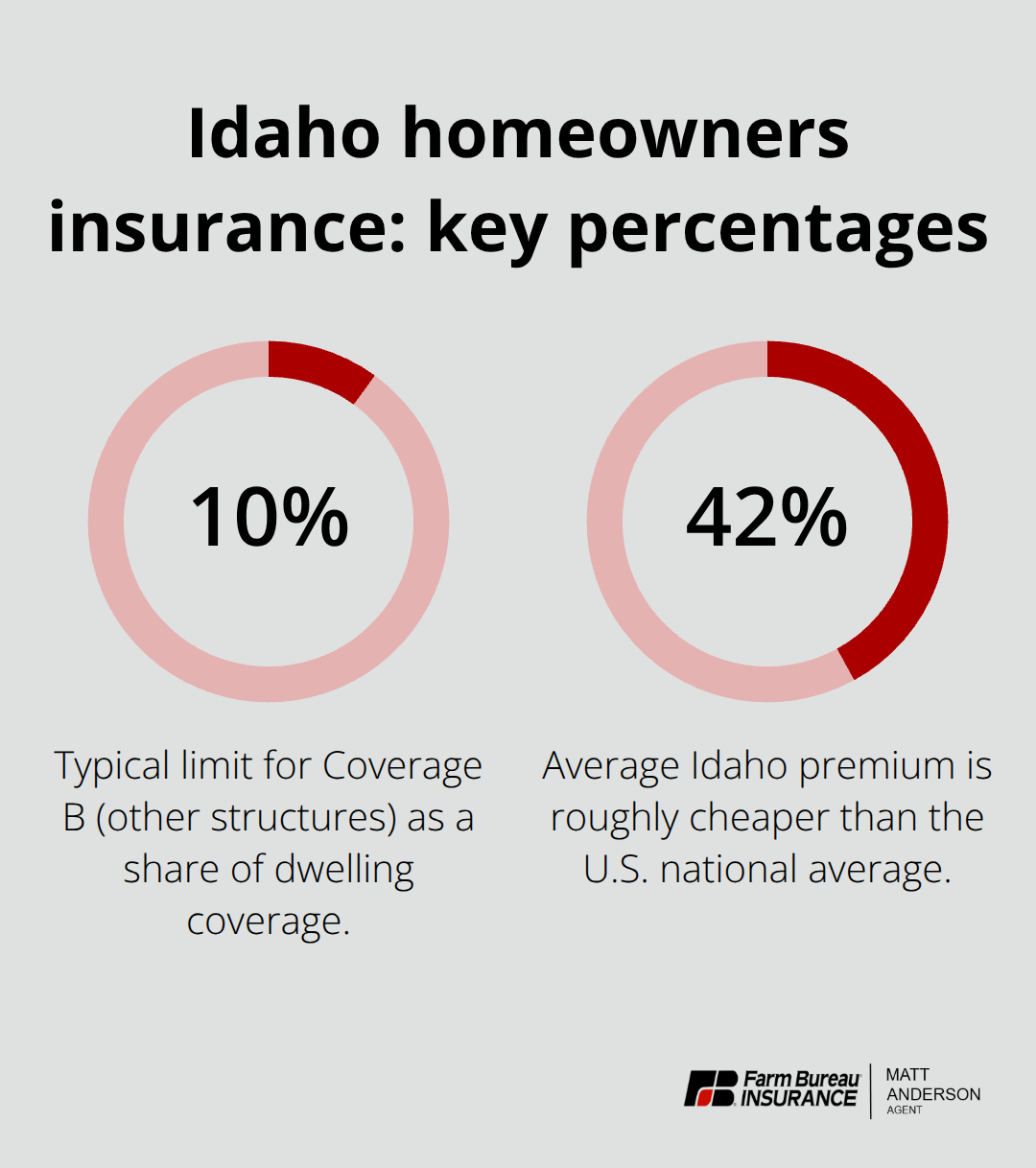

An Idaho homeowners policy covers six distinct areas, and understanding each one matters when you decide how much protection you need. Coverage A handles your dwelling itself-the structure, walls, roof, built-in appliances, and permanent fixtures. If a fire, wind, or hail damages your home, Coverage A pays to repair or rebuild it. Coverage B extends to detached structures like sheds, garages, or fences that aren’t connected to your house. Most policies limit this to 10% of your dwelling coverage, so if your Coverage A is $300,000, you typically get $30,000 for other structures. The average Idaho home costs about $1,409 per year to insure for a $300,000 dwelling, which is roughly 42% cheaper than the national average of $2,424. This lower cost reflects Idaho’s relatively moderate disaster risk compared to other states.

Personal Property Needs Real Attention

Coverage C protects your belongings-furniture, clothing, electronics, and personal items inside your home. Here’s where many homeowners make mistakes: standard policies pay actual cash value, meaning your five-year-old television worth $800 might only be worth $200 when it’s damaged. Replacement cost coverage pays what you’d actually spend to replace it new, and that option costs more in premium but protects your wallet far better. Scheduled personal property endorsements let you specifically insure high-value items like jewelry, art, or collectibles that exceed standard limits. Coverage D covers your living expenses if your home becomes uninhabitable after a covered loss-hotel bills, meals, and temporary housing costs. Coverage E is personal liability protection, covering legal costs and damages if you accidentally injure someone or damage their property. Coverage F covers medical payments to others on your property, regardless of fault. These liability coverages matter more than people realize; a single serious accident on your property could cost $50,000 or more in medical and legal expenses.

Critical Gaps in Standard Coverage

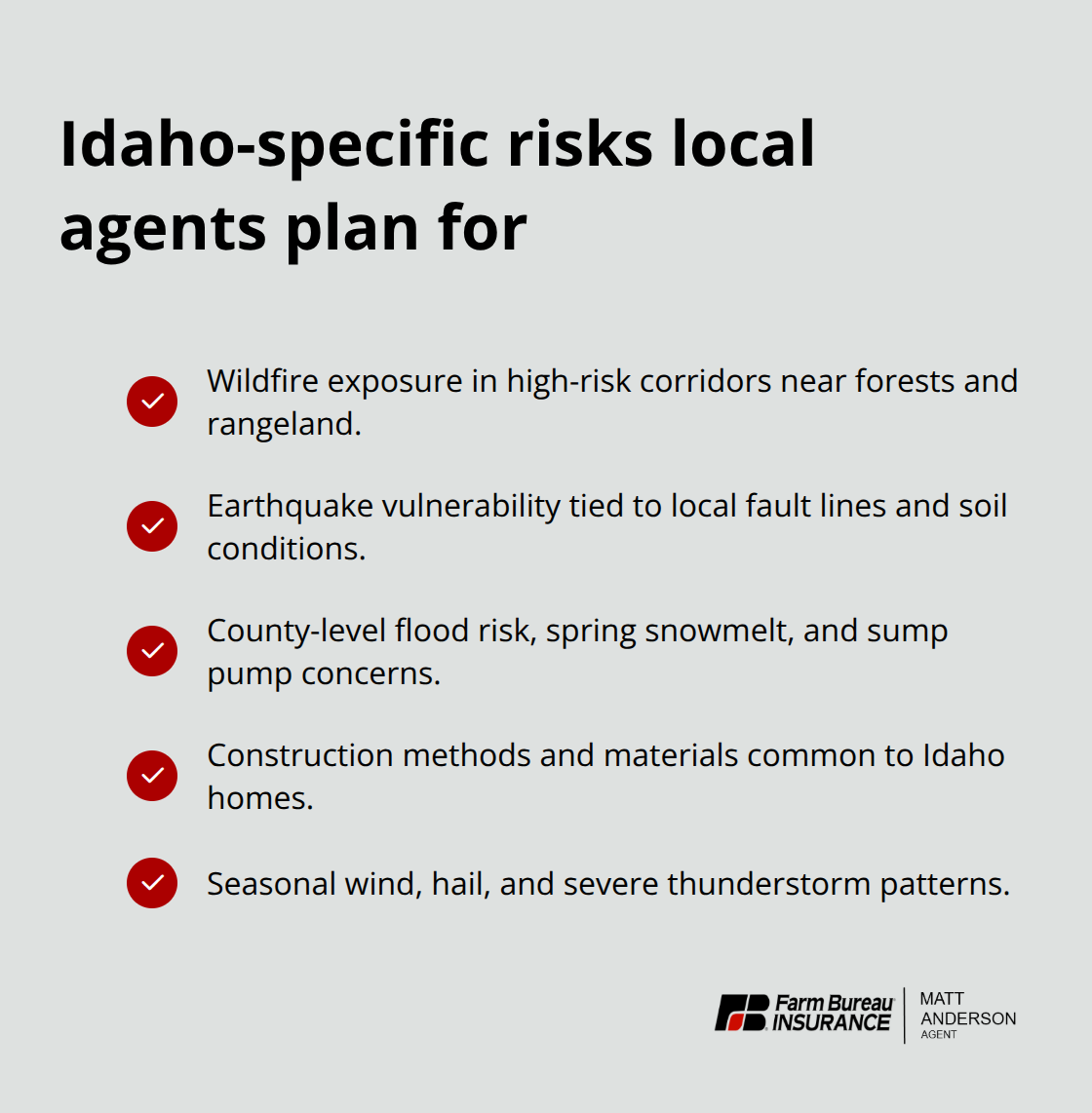

Standard Idaho policies explicitly exclude flood damage and earthquakes. Flood insurance through the National Flood Insurance Program costs extra, and with Idaho residents living in 100-year floodplains and many Idaho counties at flood risk, this gap affects thousands of homeowners. Idaho ranks 5th nationally for earthquake risk, so an earthquake endorsement deserves serious consideration if you own property here. Water backup and sump pump overflow coverage isn’t included in basic policies either, yet heavy spring snowmelt and basement water intrusion represent common Idaho claim drivers. Wildfire coverage is included for fire damage, but verify your policy details if you live in a high-risk area.

How to Close Your Coverage Gaps

The smart approach involves reviewing your specific property’s risks with an agent, then adding endorsements that match your actual exposure rather than assuming standard coverage handles everything. Your location, home age, and proximity to flood zones or wildfire areas all determine which additional protections make sense for you. An agent can identify which gaps pose real threats to your situation and which endorsements deliver the most value.

Factors That Affect Your Idaho Homeowners Insurance Rates

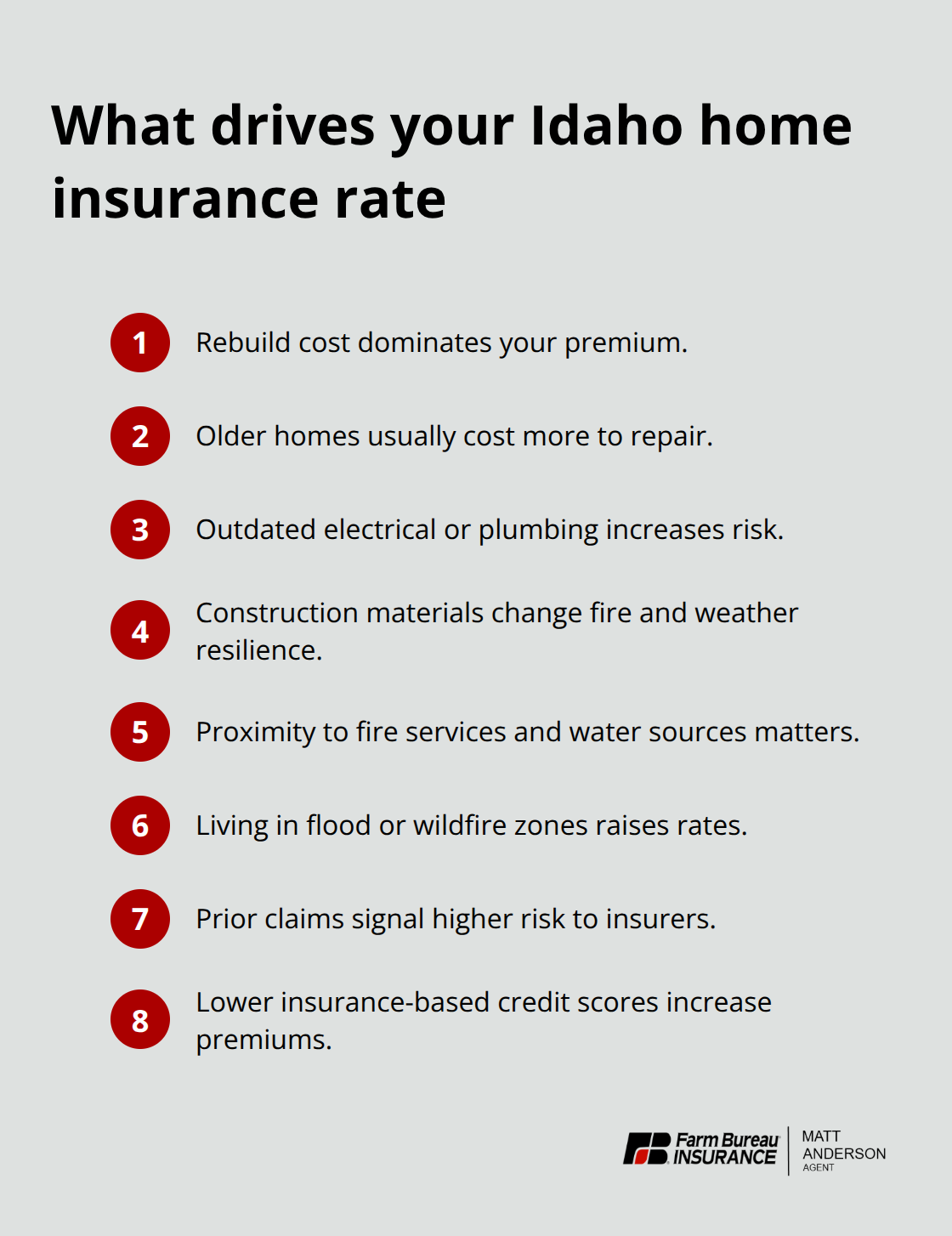

Your Idaho homeowners insurance premium isn’t random-it’s built on specific factors that insurers measure and weigh against their claims data. The cost to rebuild your home from the ground up drives your rate more than any other single factor. If your home costs $300,000 to reconstruct, you’ll pay more than someone insuring a $200,000 home, even in the same neighborhood. Home age matters significantly because older homes typically cost more to repair when damage occurs, and outdated electrical or plumbing systems increase risk. A 1970s home with original wiring will cost more to insure than a 2015 home with modern infrastructure.

Construction materials directly impact your premium too-a brick home with a metal roof costs less to insure than a wood-frame home with a composition shingle roof, since brick and metal resist fire and weather better. These rates reflect how different insurers evaluate construction and home characteristics.

Where You Live Changes Everything

Your location in Idaho creates dramatic rate differences that many homeowners overlook. Proximity to fire departments, distance to water sources for firefighting, and population density all influence your rate. Living in a flood-prone area or wildfire zone pushes your premium higher because insurers know the statistical risk in those locations.

Your Claims History and Credit Score Matter More Than You Think

Your claims history and credit score round out the personal factors affecting your rate. Insurers view people with prior claims as higher-risk, so your rate rises if you filed claims in the past few years. Insurance-based credit scoring reflects how insurers believe financial responsibility correlates with claim risk-people who manage finances carefully tend to file fewer claims. A poor credit score can increase your premium by hundreds of dollars annually, sometimes more than the impact of your home’s age or size.

Discounts That Actually Reduce Your Premium

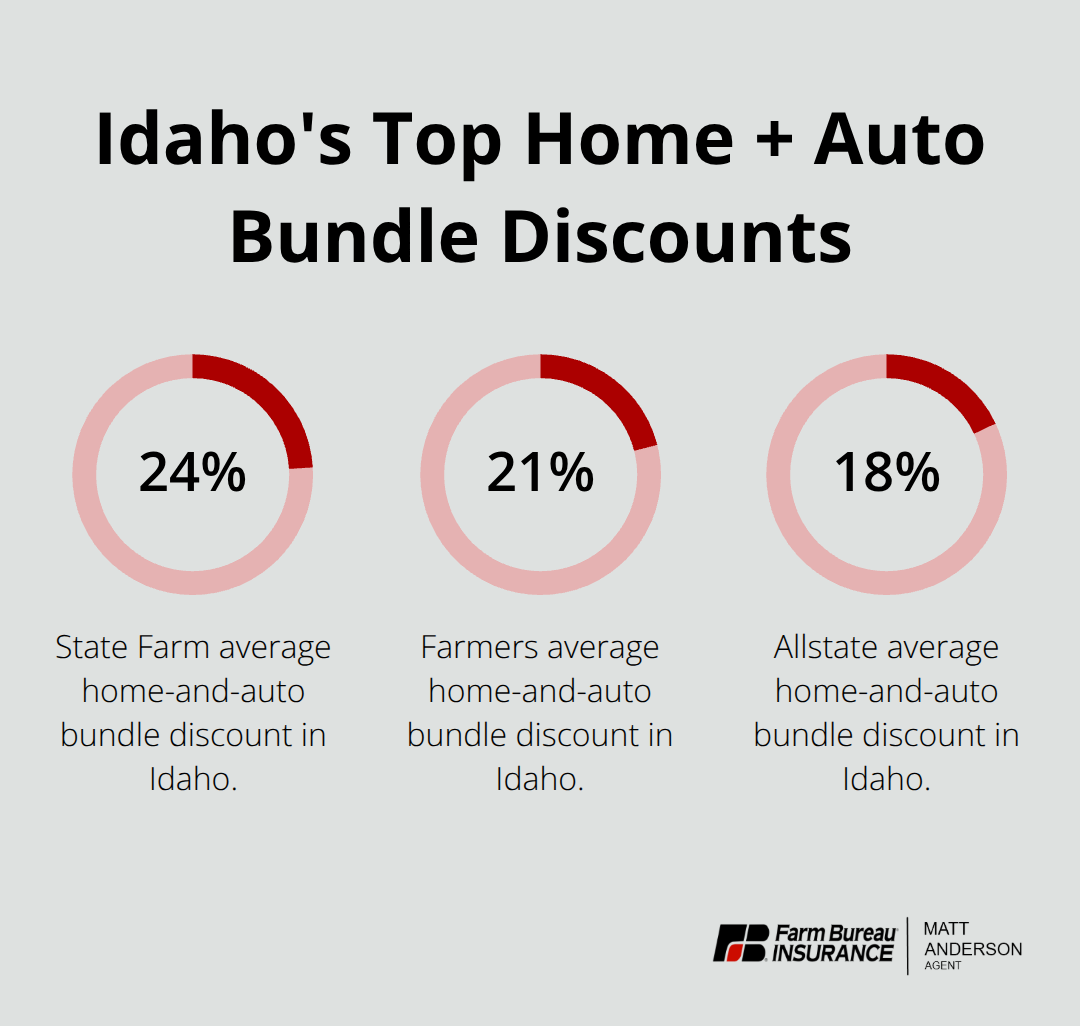

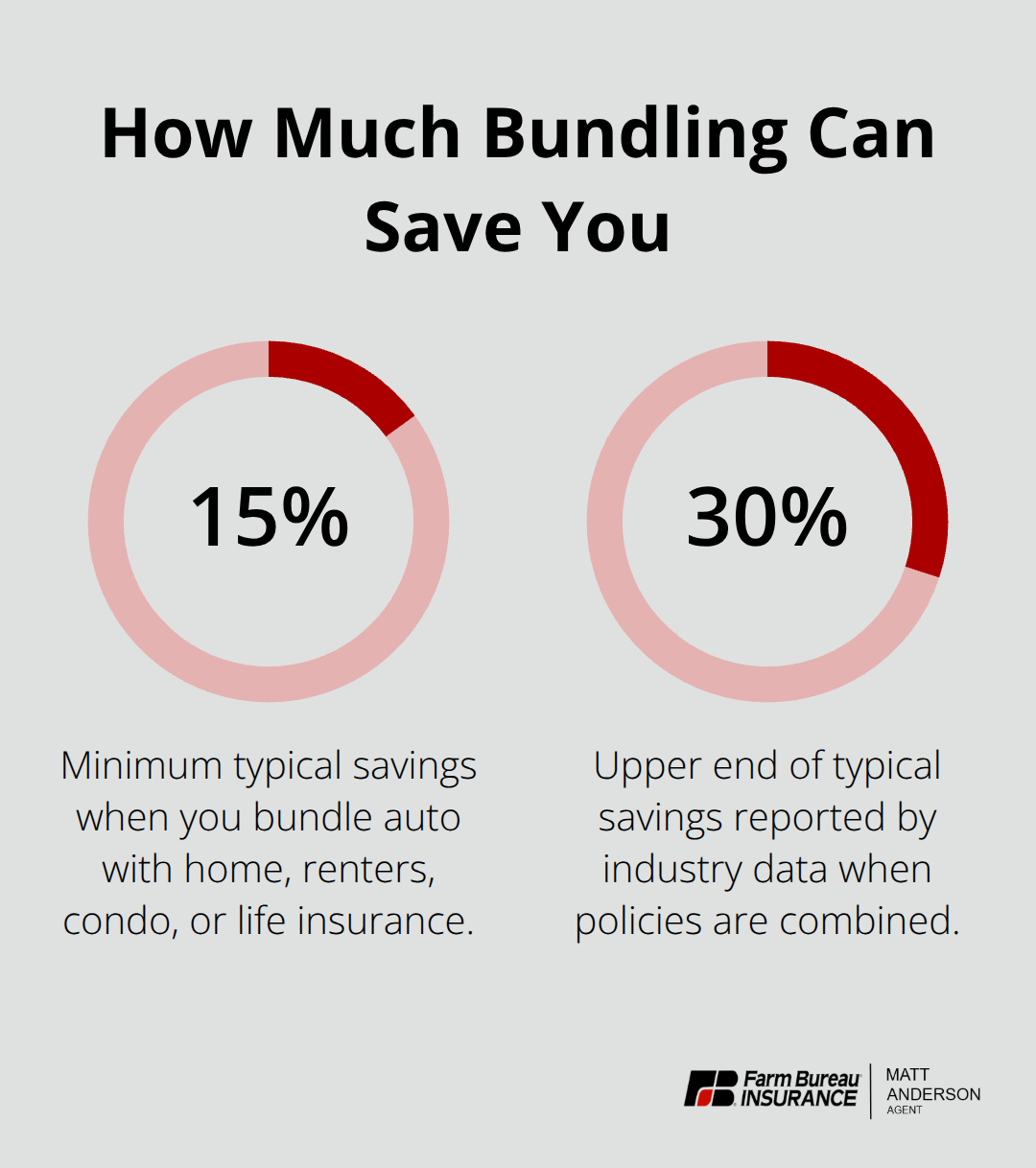

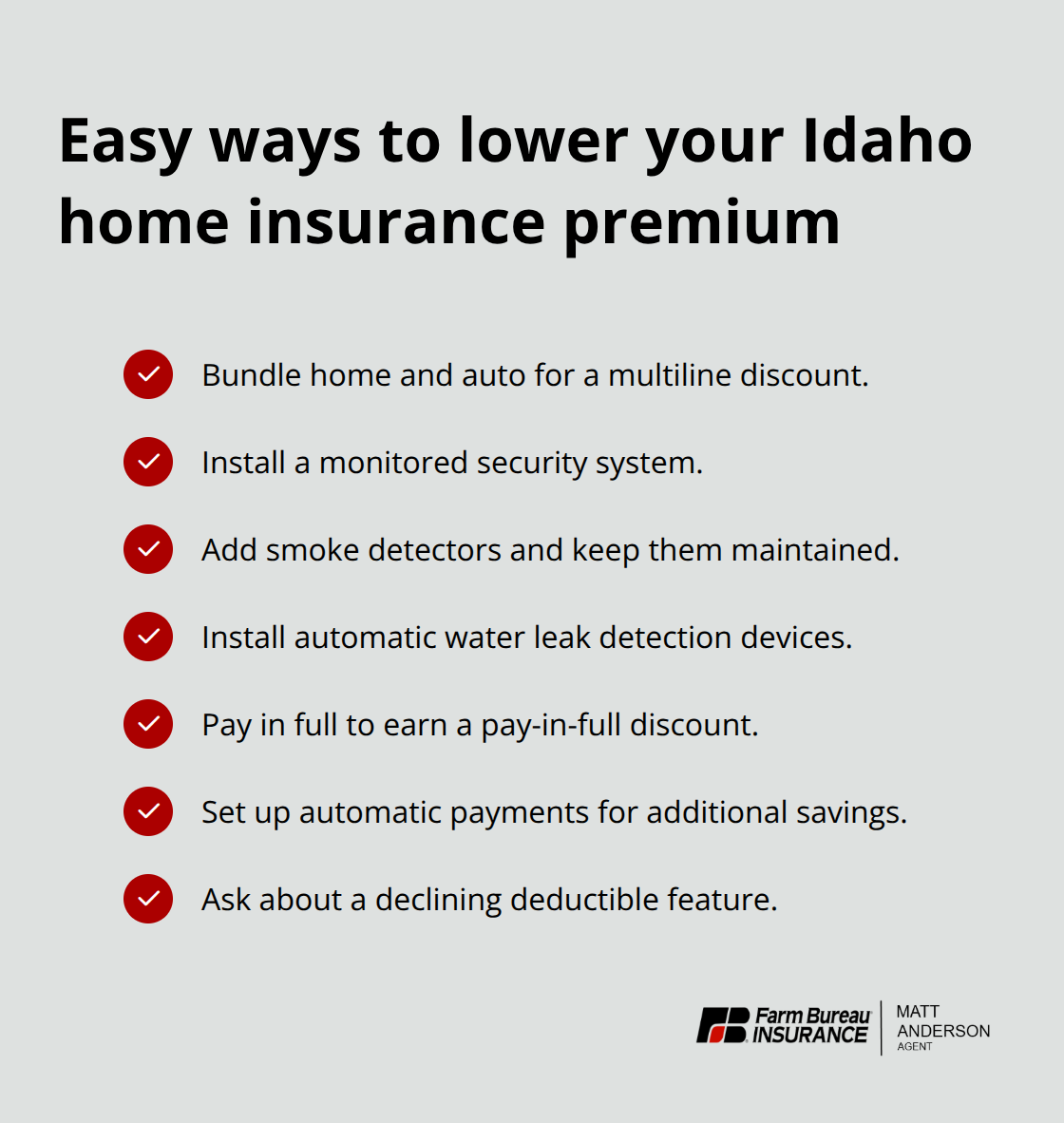

Bundling your home and auto policies with the same insurer typically yields multiline discounts, which substantially offsets the base premium. Installing security systems, smoke detectors, and automatic water leak detection devices can reduce your premium further because these features lower your insurer’s risk exposure. Paying your premium in full upfront or setting up automatic payments also qualifies you for additional savings with most carriers.

How These Factors Work Together

Understanding these rate drivers helps you make smarter decisions about coverage and deductibles. You can’t change your home’s age or location, but you can control your claims history going forward, improve your credit score, and install protective devices that lower your risk profile. The next step involves assessing what coverage levels actually protect your situation and comparing quotes from multiple insurers to find the best combination of price and protection.

How to Choose the Right Coverage and Price for Your Idaho Home

Start by calculating what it would actually cost to rebuild your home from scratch, not what you paid for it years ago. Construction costs in Idaho have risen significantly, and rebuilding expenses often exceed original purchase prices. To calculate your home’s replacement cost value, you’ll need to know its square footage, age, construction materials, foundation type and home features. Add 15% to account for inflation and unforeseen structural issues discovered during reconstruction. This figure becomes your dwelling coverage amount, and it’s the single most important decision you’ll make. Underinsuring by even $50,000 could leave you personally responsible for that gap after a major loss.

Once you know your rebuild cost, add your other structure coverage (typically 10% of dwelling), then estimate your personal property value by walking through your home and photographing items. Document electronics, furniture, artwork, and jewelry separately because high-value items need scheduled endorsements rather than relying on standard coverage limits. Your loss of use coverage should equal roughly three months of your current living expenses, which protects you if your home becomes uninhabitable.

Compare Quotes from Multiple Carriers

Contact at least three different insurers and request quotes using identical coverage amounts across all quotes, not the minimums they suggest. This comparison method reveals which carriers price your specific situation competitively and which ones don’t. You’ll notice dramatic rate differences-sometimes $300 to $500 annually between carriers for the same coverage on the same home.

Ask each insurer about bundling discounts because combining home and auto policies typically saves 15% to 20% on your total premium. Don’t accept the first quote-competition works in your favor.

Evaluate Your Deductible Options

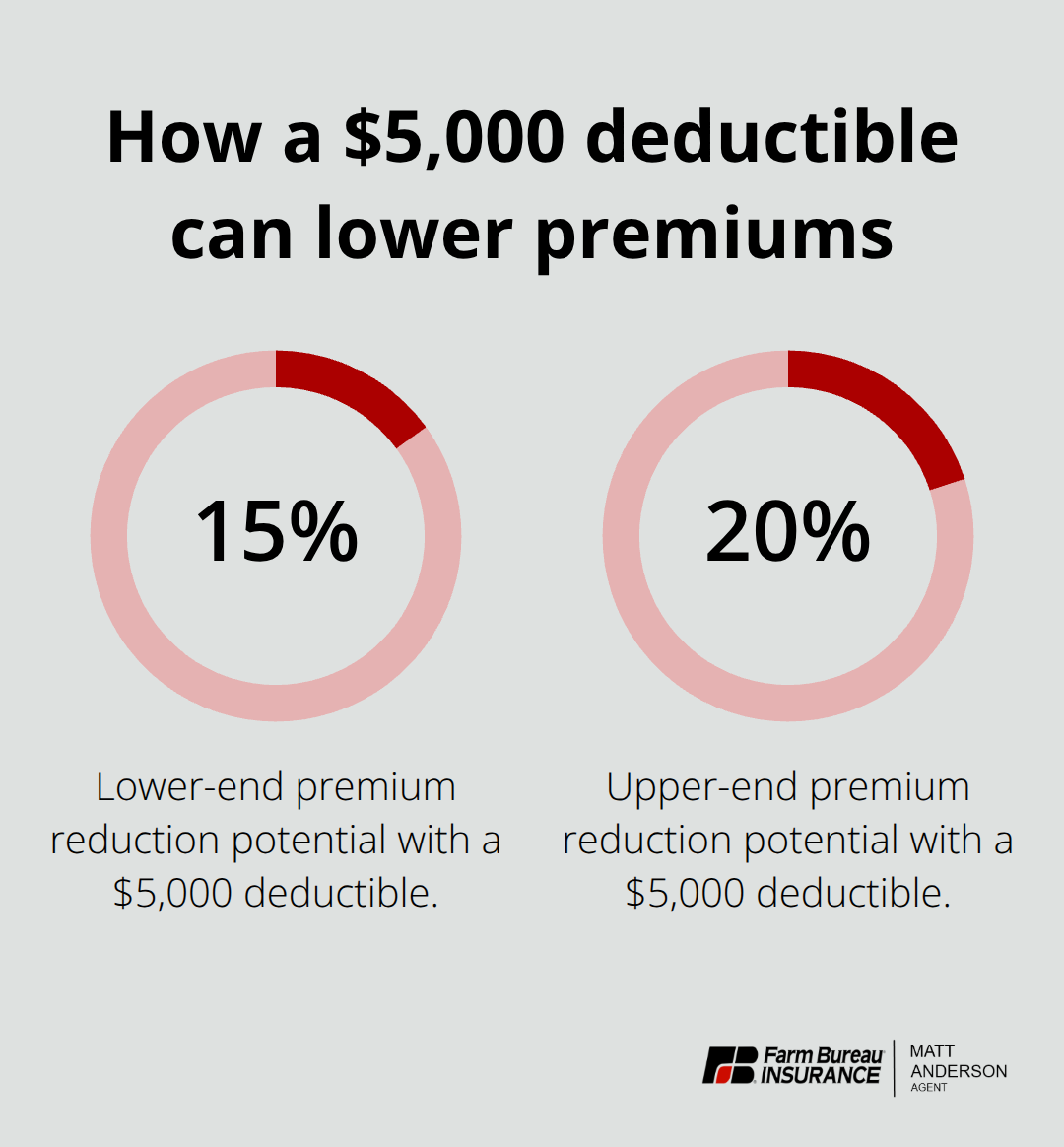

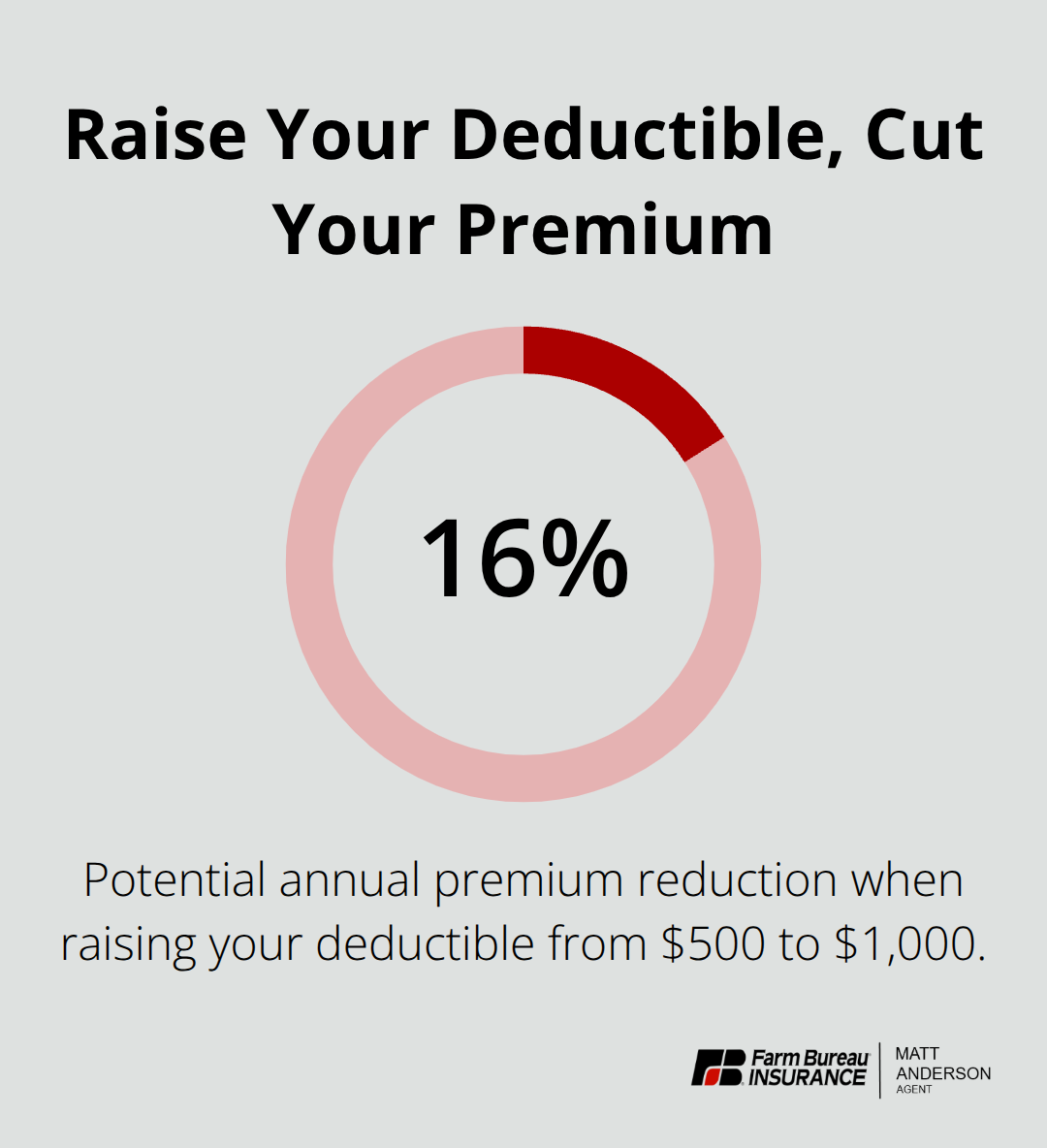

When you receive quotes, compare the deductible options carefully because raising your deductible from $500 to $1,000 often reduces your premium by 10% to 15%, which saves $100 to $200 annually on a typical Idaho policy. Your deductible choice directly affects both your monthly cost and your financial exposure during a claim. A $500 deductible means you pay $500 out of pocket before your insurer covers the rest, while a $1,000 deductible increases your out-of-pocket responsibility but substantially lowers your premium.

The math works in your favor if you have adequate emergency savings-choosing a higher deductible reduces your annual premium cost, and that savings compounds over years of claims-free coverage. However, only raise your deductible if you can genuinely afford to pay it without financial hardship when a loss occurs. Many Idaho homeowners find the $1,000 deductible the right balance because it saves meaningful premium dollars while remaining manageable if a claim happens.

Maximize Discounts and Special Features

Review whether your policy includes declining deductible features, which some carriers offer as an optional add-on; these reduce your deductible by $100 for each year you don’t file a claim, eventually dropping to zero on minor claims. Installing security systems, smoke detectors, and automatic water leak detection devices can reduce your premium further because these features lower your insurer’s risk exposure. Paying your premium in full upfront or setting up automatic payments also qualifies you for additional savings with most carriers.

Final Thoughts

Your Idaho homeowners insurance policy protects one of your largest financial assets, but only when you understand what you’re actually buying. The coverage types we’ve outlined-dwelling protection, personal property, liability, and loss of use-form the foundation of your protection, while rate factors like location, age, and claims history determine what you’ll pay. Selecting the right policy means matching your coverage limits to your actual rebuild costs, recognizing coverage gaps like flood and earthquake exclusions, and comparing quotes from multiple carriers using identical coverage amounts.

The decisions you make now determine whether you’re truly protected when loss strikes. An underinsured home leaves you personally responsible for the gap, while a policy without flood coverage becomes worthless if water damage occurs. Missing the right discounts means paying hundreds more annually than necessary, and choosing the wrong deductible can either drain your emergency savings or cost you thousands in unnecessary premiums.

We at Matt Anderson Insurance understand these decisions matter, which is why our licensed agents work with Idaho families to build policies that actually fit their situations. Contact us today to discuss your specific coverage needs and get a personalized quote that protects your home and your finances.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.