Idaho Contractor Bonding Insurance: Why Bonds Matter For Projects

Running a contracting business in Idaho means understanding what protects your work and your wallet. Idaho contractor bonding insurance isn’t optional-it’s a legal requirement for licensed contractors and a practical shield against financial risk.

At Matt Anderson Insurance, we help contractors navigate bonding requirements so you can focus on building. The right bonds give your clients confidence and keep your business compliant with state regulations.

Why Bonding Protects Your Contracting Business

Idaho’s contractor registration law, enforced by the Idaho Contractors Board, makes bonding non-negotiable for most construction work. Any project valued over $2,000 in materials and labor requires you to register, and registration demands proof of general liability insurance with a minimum of $300,000 in coverage. State-level bonding applies specifically to Plumbing, HVAC, Fire Protection Sprinkler, and Farm Labor Contractors, with bond amounts ranging from $2,000 to $30,000 depending on your specialty. Plumbing, HVAC, and Fire Protection Sprinkler contractors each need $2,000 bonds, while Farm Labor Contractors face requirements between $10,000 and $30,000. Without the correct bond in place, you cannot legally operate, obtain building permits, file liens, or enforce contracts. The penalty for working unregistered is serious-you face misdemeanor charges carrying up to $1,000 in fines or six months in jail.

How Bonds Protect Your Financial Position

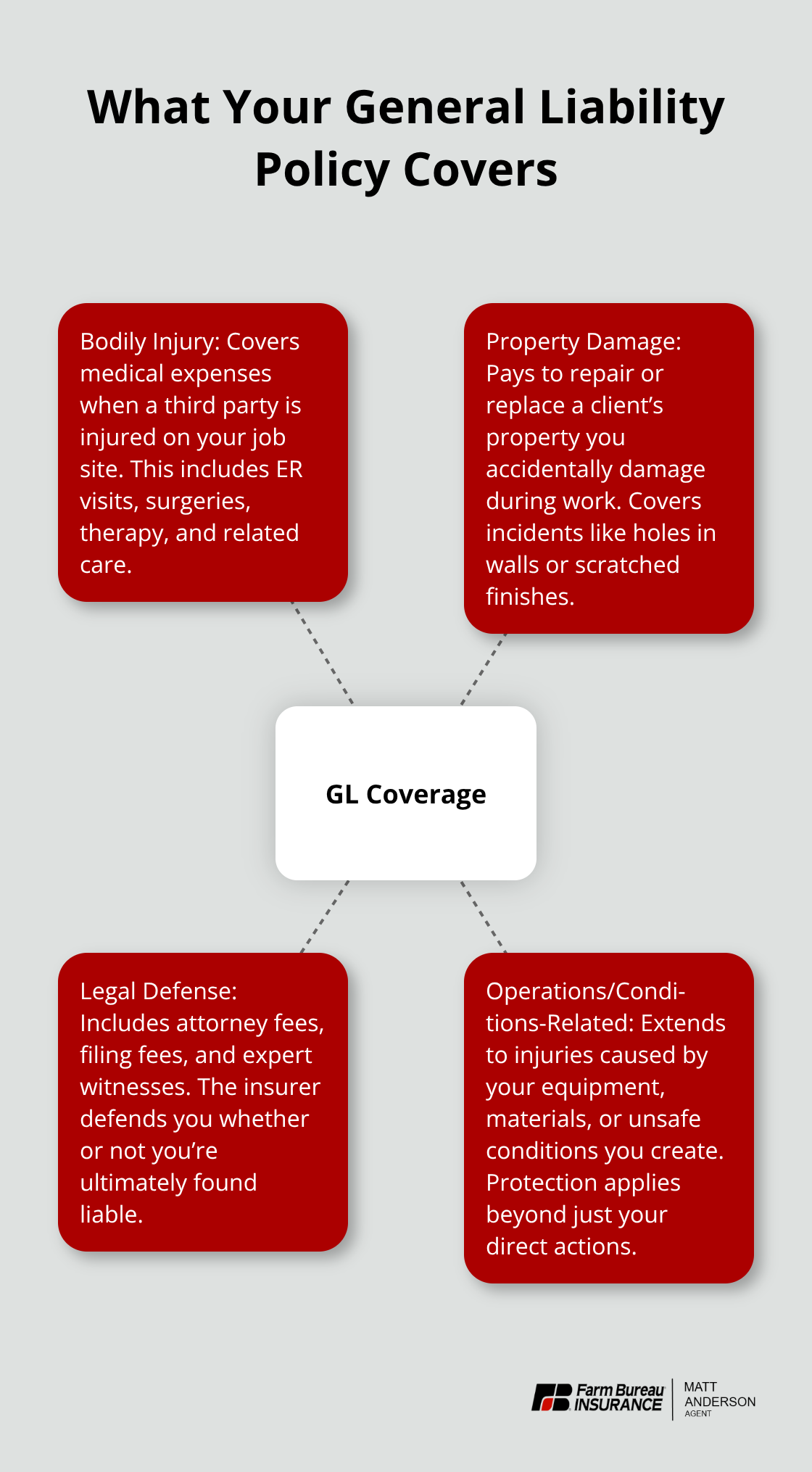

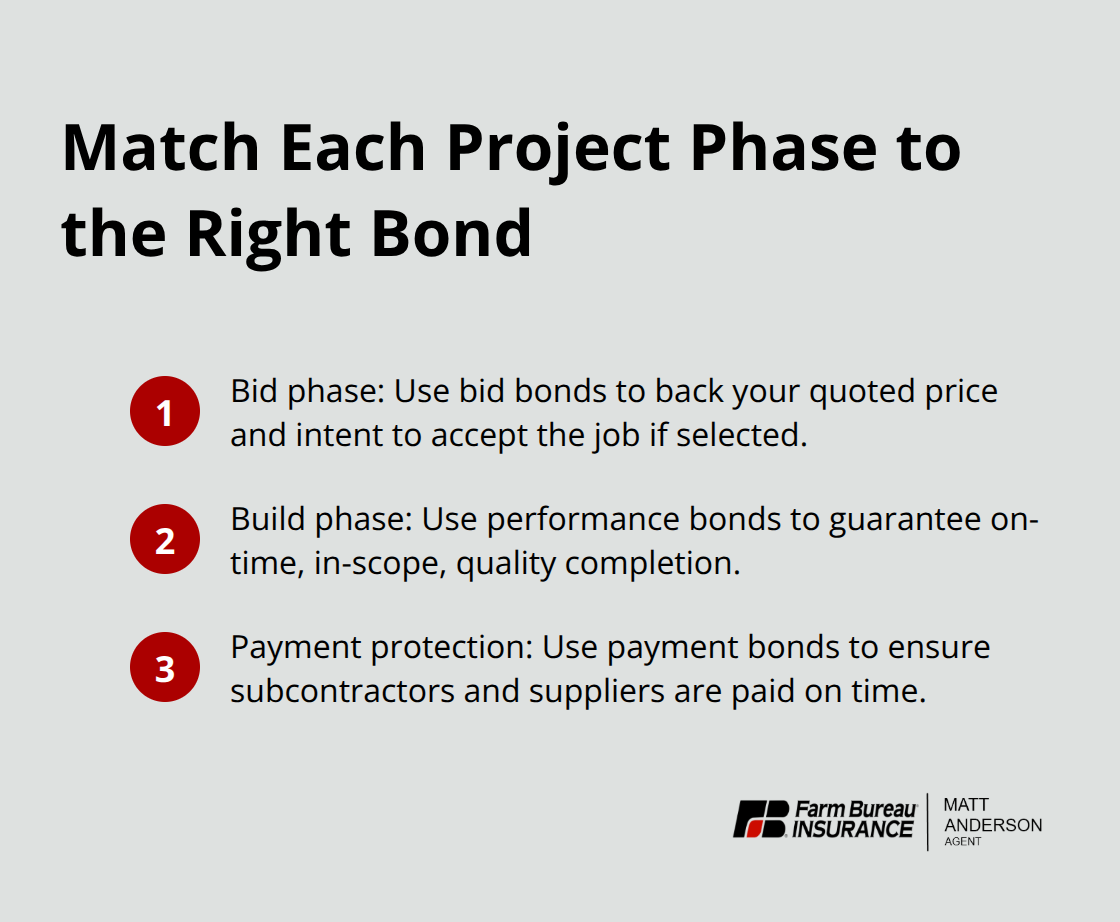

Bonds function as a financial guarantee that protects both you and your clients. When a surety backs your bond, they commit to reimburse project owners for damages or unpaid claims up to the bond amount. Construction projects carry real risk-materials get damaged, timelines slip, workers get hurt, and subcontractors sometimes go unpaid. Performance bonds specifically guarantee that you will complete work as promised on time and within scope. Payment bonds ensure that workers and suppliers receive what they are owed, protecting them from your financial failure. Bid bonds prove to project owners that you will honor your bid price and take on the job if selected. These three bond types work together to shift risk away from you personally and onto the surety company backing your work. Your personal assets remain protected because claims go against the bond, not your bank account or business assets.

What Clients See When You Carry Bonds

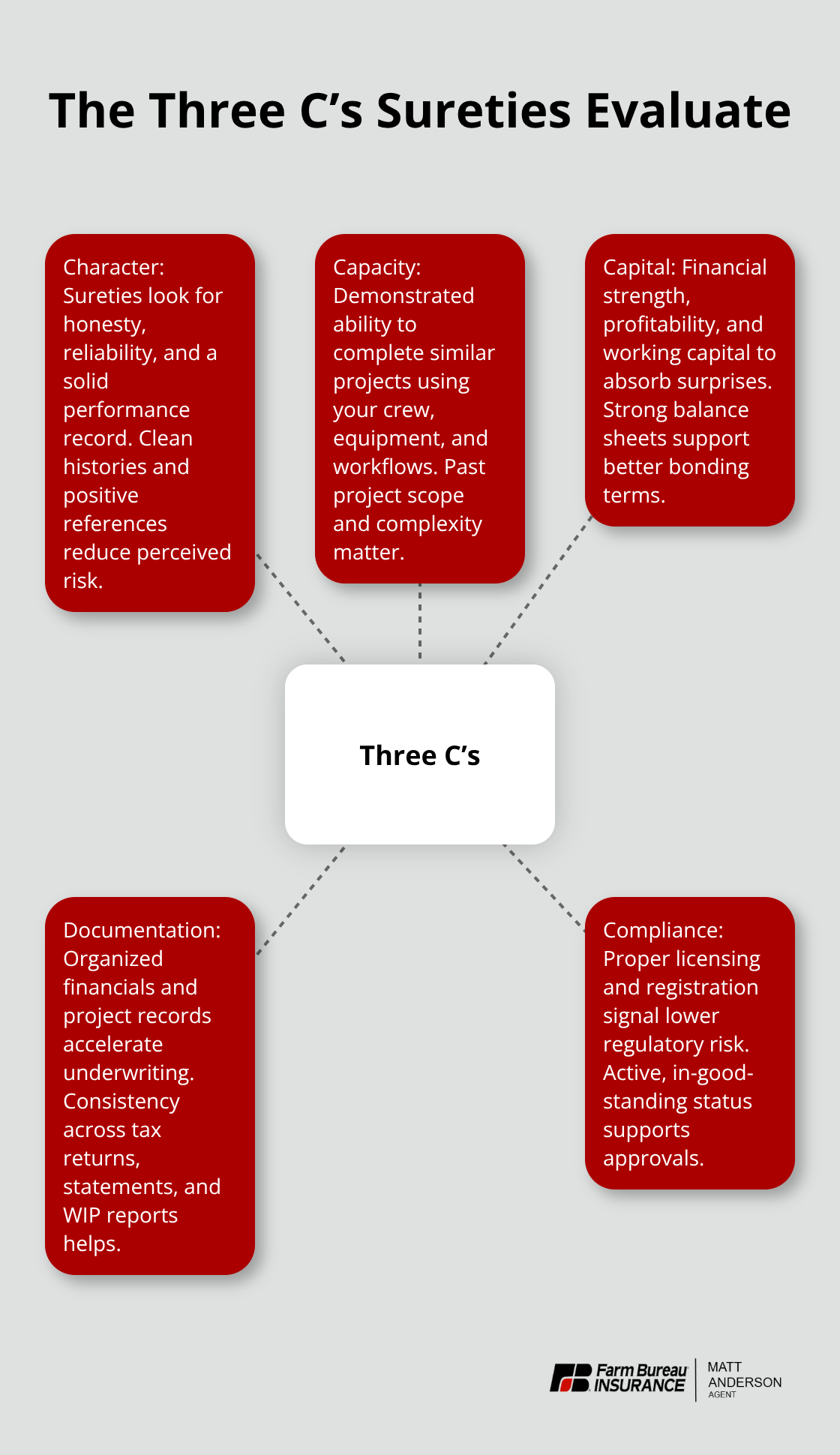

Project owners and general contractors openly favor bonded contractors when selecting subcontractors or awarding bids. A bond signals that you have passed underwriting scrutiny based on character, capacity, and capital-the three C’s that sureties evaluate. Character assessment examines your honesty and past performance record. Capacity evaluation reviews your ability to complete similar projects using your resources and workflows. Capital analysis looks at your financial strength, net worth, profitability, and working capital to determine whether you can weather project challenges. Clients see bonding as proof that an independent third party has verified your credentials and financial stability.

Without bonds, you compete on price alone, which means lower margins and higher stress. Bonded contractors win more competitive bids and attract clients willing to pay fairly for reliable work.

Moving Forward with the Right Coverage

The bond types you need depend on your trade and the projects you pursue. Bid bonds protect you when you submit proposals for competitive work. Performance and payment bonds become essential once you win a contract and start the actual construction. Understanding which bonds apply to your situation-and maintaining them throughout your business operations-keeps you compliant and competitive. The next section covers the specific bond types that protect different phases of your contracting work.

Which Bond Types Cover Your Contracting Work

Idaho contractors operate across three distinct project phases, and each phase demands a specific bond type. When you submit proposals for competitive work, bid bonds prove to project owners that you will honor your quoted price and accept the job if selected. Most bid bonds cost between 1 and 3 percent of your bid amount, making them relatively affordable protection. Once you win the contract and work begins, performance bonds take over.

These bonds guarantee that you will complete the project on time, within scope, and to the quality standards outlined in your agreement. Performance bonds typically cost 1 to 3 percent of the total contract value, though contractors with strong credit histories and solid track records often qualify for rates at the lower end of that range.

How Payment Bonds Protect Your Subcontractors

Payment bonds operate alongside performance bonds on most projects over $2,000. They protect your subcontractors and material suppliers by guaranteeing they receive payment even if you face cash flow problems. Payment bonds cover the same contract value as performance bonds and carry similar pricing. This protection matters because unpaid suppliers can file liens against your projects, which creates legal complications and damages your reputation with future clients.

State-Level Bond Requirements by Trade

The Idaho Division of Building Safety requires that Plumbing, HVAC, and Fire Protection Sprinkler contractors maintain a $2,000 state-level bond with their respective licensing boards. These state bonds cost as little as $100 per year or $10 per month, depending on your credit profile and the surety company you work with. Farm Labor Contractors face steeper requirements, ranging from $10,000 to $30,000, reflecting the higher risk associated with wage and labor compliance violations. Your specific trade determines which state bond applies to your license.

The Three C’s That Sureties Evaluate

The underwriting process for any bond centers on what sureties call the three C’s: Character, Capacity, and Capital. Character evaluation reviews your payment history, references from past clients, and any disciplinary actions against your license. Capacity assessment examines whether you have completed similar projects, maintain adequate equipment and crew, and demonstrate reliable workflows. Capital analysis looks at your net worth, business profitability, and working capital reserves-essentially whether you have financial cushion to handle unexpected costs.

Building Your Bonding Profile for Better Rates

Contractors with clean credit scores and documented project success typically secure bonds within 24 to 48 hours and receive the most favorable rates. Conversely, contractors with recent credit issues or limited project history may face higher premiums or stricter underwriting conditions. Your bond application should include tax returns from the past two years, bank statements showing current working capital, and a portfolio of completed projects matching the scope and value of work you plan to bid. Sureties want to see that you have successfully managed projects at or above the contract values you are bidding. If you are new to contracting or transitioning to larger projects, start with smaller bid amounts and build a documented track record of successful completions. This approach strengthens your position for future bonding at better rates and demonstrates to sureties that you can handle increased responsibility. The mistakes contractors make during this phase-underestimating costs, choosing inadequate coverage, and failing to maintain compliance-can derail your bonding approval and damage your business standing.

Mistakes That Drain Your Bonding Budget and License

Underestimating Bond Costs Across Multiple Projects

Most Idaho contractors underestimate how bonding costs stack up across multiple projects, and this miscalculation creates cash flow problems that undermine profitability. A bid bond on a $50,000 project costs between $500 and $1,500 depending on your credit score, while a performance bond on that same contract runs $500 to $1,500 again. If you bid five projects in a month and win three, you have paid for two bonds you will never use, plus three active performance and payment bonds on concurrent jobs. Your bond costs should appear as a line item in every project estimate, not as an afterthought.

The surety bond application process itself takes time-typically 24 to 48 hours for approval if your financial profile is clean-but delays happen when sureties request additional documentation or flag credit concerns. Many contractors fail to budget for this friction and miss bid deadlines because they did not account for processing time.

How Credit Scores Impact Your Bond Premiums

Contractors with poor credit scores pay significantly higher premiums because sureties view them as higher risk. A contractor with a credit score below 650 might pay $150 per month for a $2,000 state bond instead of the $10 per month rate available to contractors with scores above 750. Over a year, that difference equals $1,680-money that comes directly out of your profit margin.

Review your credit report annually and address any errors or outstanding issues before applying for bonds, since your credit profile directly impacts your cost structure. This step alone can save thousands across your bonding lifetime.

Selecting Coverage Limits That Leave You Exposed

Choosing inadequate coverage limits creates exposure that bonds are supposed to eliminate. Idaho law requires general liability insurance with a minimum $300,000 single limit, but this floor does not mean it covers all your risk. A single injury claim on a residential project can easily exceed $300,000 in medical costs and lost wages. If your liability insurance has a $300,000 limit and a claim reaches $400,000, you personally pay the $100,000 gap.

Performance bonds protect project completion but do not cover liability claims-that is what liability insurance handles. Many contractors bundle these two protections without understanding the distinction, then discover mid-project that their coverage leaves gaps. State-level bonding for HVAC, Plumbing, and Fire Protection Sprinkler contractors requires only $2,000 bonds, but this covers state compliance violations, not project liability.

Failing to Maintain Registration and Display Requirements

Failing to maintain compliance with Idaho regulations costs far more than the bond itself. The Idaho Contractors Board requires you to display your registration number at your business location and every jobsite, on all advertising, contracts, building permits, letterheads, purchase orders, and subcontracts. Contractors who skip this step face registration revocation and lose the ability to file liens, enforce contracts, or obtain permits.

If you hire subcontractors or suppliers, you must verify they are registered-if they are not and you work with them anyway, you risk losing lien rights on that project. Renewal notices arrive six weeks before your registration expires, but contractors who ignore them lose active status and must reapply. The penalty for operating unregistered is a misdemeanor carrying up to $1,000 in fines or six months in jail.

Final Thoughts

Idaho contractor bonding insurance protects your business in three concrete ways. Bonds keep you legally compliant with state registration requirements and licensing board mandates, preventing the misdemeanor charges and lien-loss penalties that derail contractors who operate without proper coverage. They shift financial risk away from your personal assets and onto the surety company backing your work, so claims against your projects do not drain your bank account or business reserves. Project owners and general contractors gain confidence that you have passed independent financial and character verification, which helps you win competitive bids and command fair pricing instead of competing on cost alone.

We at Matt Anderson Insurance understand that bonding requirements feel overwhelming when you focus on running your contracting operation. Our licensed agents identify exactly which bonds your trade requires, calculate realistic costs for your project pipeline, and secure coverage that fits your budget and timeline. We handle the application process, coordinate with licensing boards, and manage renewals so compliance stays on your radar without consuming your time.

Contact Matt Anderson Insurance to discuss your bonding needs and explore how bundling your contractor bonds with other business coverage can lower your overall insurance costs. We will walk you through the application process, explain which bond types apply to your projects, and help you avoid the costly mistakes that drain profitability. Your registration and bonding are too important to leave to chance.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles.